J.D. Power/LCM: June SAAR Expected to Fall to Five-Year Low

Despite record incentive spending, the auto industry is on pace to record its weakest first-half sales performance since 2014, according to the two firms. Days to turn remained at 70 through June 18, the highest level since July 2009.

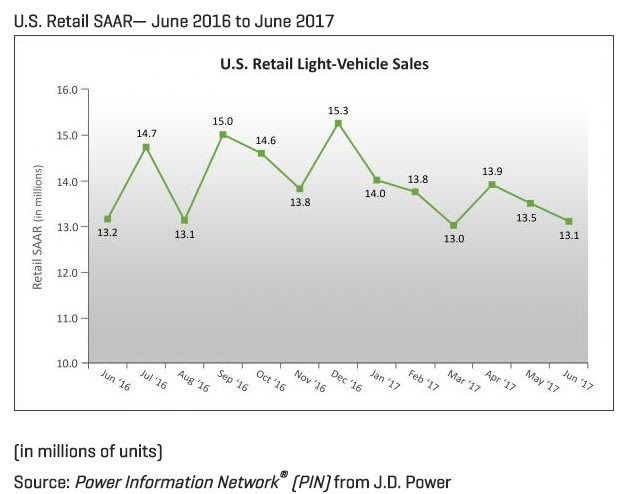

DETROIT — With new-vehicle sales in June expected fall to their lowest level since 2012, the auto industry is on pace to record its weakest first half since 2014, according to forecast partners J.D. Power and LMC Automotive.

The two firms expect new-vehicle sales to total 1.17 million units in June, a 1.3% decrease from the year-ago period. They also put the seasonally adjusted annualized rate (SAAR) for retail sales 13.1 million units, a decrease of 51,000 units from a year ago.

For the first half, retail sales are projected to be down 1% from last year.

“While the retail selling rate has declined in four of the first six months, the broader concern remains the negative health indicators behind the sales results,” said Deirdre Borrego, senior vice president of automotive data and analytics at J.D. Power.

Borrego pointed to total incentive spending as one of those indicators, which rose 11.7%, or $2.5 billion, from a year ago, to a record $25.2 billion through June. On a per-unit basis, spending for the average new vehicle through June has increased $416 from a year ago to $3,770. On trucks and SUVs, incentive spending has risen by $484 from a year ago to $3,645, while spending on cars has jumped $345 to $3,983.

Average incentive spending per unit to date through June is expected to come in at a record $3,661, surpassing the previous high for the month of $3,370 in June 2016. Spending on trucks and SUVs is expected to be $3,494, up $350 from a year ago. Spending on cars is expected to rise by $249 to $3,955.

Incentives as a percentage of MSRP are at 10% so far in June and are on pace to exceed the 10% level for the 11th time in the past 12 months.

And despite the record spending on incentives, the average new-vehicle retail transaction price to date has risen to a record $31,720, surpassing the previous high, set in June 2016, of $31,073. At that level, consumers are on pace to spend $37.1 billion on new vehicles in June, about $263 million more than last year and a record for the month.

As for sales, Trucks account for 63.7% of new-vehicle retail sales through June 18 — the highest level ever for the month of June and the 12th consecutive month above 60%. Days to turn, the average number of days a new vehicle sits on a dealer’s lot before being sold to a retail customer, remained at 70 through June 18, the highest level since July 2009 (80 days).

Fleet sales are expected to total 309,900 units in June, down 5.7% from June 2016 on a selling-day adjusted basis. Fleet volume is expected to account for 21% of total light-vehicle sales, a decrease from 21.7% in June 2016.

“As the U.S. auto market enters the fourth month in a row of a sub-17 million-unit selling rate, nerves are being tested. The primary driver of the decline in the total sales pace is a pullback in fleet volume, which is projected to be down 8% for the first half of 2017, while retail sales, assisted by elevated incentives, are projected to contract by 0.6% for the same period,” said Jeff Schuster, senior vice president of forecasting at LMC Automotive. “It will be challenging in the second half of the year to keep pace with 2016, so some additional weakness and further risk are expected in both fleet and retail volume, but a year still expected above 17 million units should not be considered a poor performance.”

The prolonged pullback in fleet volume combined with the leveling off of the retail market has led to another trimming of LMC’s outlook for 2017. The firm cut its 2017 total light-vehicle sales forecast to 17.1 million units, down from 17.2 million last month and a decline of 2.6% from 2016. The retail light-vehicle outlook has also been reduced by 50,000 units but continues to round to 13.9 million units, a decline of 1.8% from 2016. Fleet volume is now expected to be down 6.1% from 2016.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →