TransUnion: Auto Loan Growth Slowing

Originations continued to fall at a faster rate than previous years, as finance sources continued to tighten underwriting standards during 2017’s end-of-year quarter. TransUnion officials, however, say the sector is performing well as the economy remains relatively strong.

CHICAGO — Declines in the unemployment rate and delinquencies opened up the credit markets in 2017, with TransUnion reporting this month that consumer opened 20.3 million more accounts in 2017 spanning auto, credit card, mortgage, and unsecured personal loans.

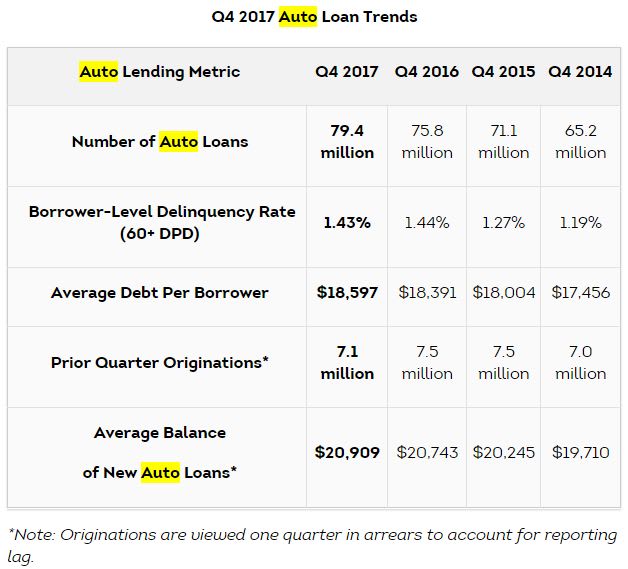

The number of auto loan accounts rose 4.8% in the fourth quarter of 2017 compared to a year ago, while the 60-day delinquency rate fell one basis point to 1.43% over the same period. Factors that could stunt the fluid consumer credit economy, according to TransUnion, are material upticks in delinquency, interest rate increases beyond what is expected, and other unanticipated economic shocks.

“Consumers continue to gain access to more credit, and balances are generally rising at a healthy clip,” said Matt Komos, vice president of research and consulting at TransUnion. “For the most part, consumers are paying their debts in a timely fashion, which has been especially evident for mortgages and personal loans. This is likely a result of the strong economy, which has helped consumers manage their personal balance sheets and build confidence.”

The firm noted that despite auto loan balances growing 5.5% to $1.179 trillion between the fourth quarters of 2016 and 2017, the growth rate was the lowest since the 5.3% increase recorded between the second quarters of 2011 and 2012. Despite the slowdown in balance growth, however, the number of auto loans grew from 75.8 million in the prior-year quarter to 79.4 million.

Originations declined for the fifth consecutive quarter, falling 4.8% in the third quarter compared to the prior-year period to 7.1 million, according to the firm, which views originations one quarter in arrears to account for reporting lag. The drop, according to TransUnion, was driven by an 8.2% year-over-year decline for the subprime, nearprime and prime credit risk categories.

“Auto lending is stabilizing after years of rapid growth. Originations continue to fall at a faster rate than previous years, balance growth is slowing and delinquencies are steady,” said Brian Landau, senior vice president and automotive business leader at TransUnion. “These metrics reflect the continuing tightening of underwriting, particularly for prime and below risk tiers.

“General speaking, the auto lending sector is performing well as the economy remains relatively strong,” Landau added. “We do not observe anything in our data that would point to significant anticipated changes in delinquencies.”

More F&I

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →

Your Office Is Talking

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

Read More →

F&I Training Fundamentals

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Read More →

Not Just Any Tire Will Do

More consumers and businesses are opting for all-season options for various reasons as safety, sustainability and convenience push practical change.

Read More →