Cox: September Sales to Decline 7.2% From Year-Ago Levels

Despite the expected volume decline, the firm put September’s seasonally adjusted annual sales rate at a healthy 17.1 million, down from last September’s 18.1 million SAAR. The company said higher interest rates and talks of tariffs may be having some pull-ahead impact in the market.

ATLANTA — September’s new-vehicle sales pace is expected to rise to 17.1 million units, according to Cox Automotive. If realized, the firm’s forecast would be an improvement over August’s 16.6 million sales rate. The gain, however, might be misleading, Cox’s Senior Economist Charlie Chesbrough said.

The firm noted that September’s total sales volume should decline nearly 60,000 units from last month nearly 100,000 units compared to September 2017, which benefit from a sales lift from replacement demand and delayed purchases following Hurricane Harvey in August 2017.

“Year-over-year comparisons are challenging in September, as the industry realized record sales levels last year,” said Chesbrough. “With one less selling day this September and due to seasonal adjustment factors, the sales pace will actually show an increase, despite significant volume declines.”

Vehicle sales reached an all-time high in September 2017 and bested the previous two Septembers by nearly 80,000 units. A large decline from last September’s unnaturally high level is expected, and recent storms and flooding in the Southeast will only contribute to weak volumes.

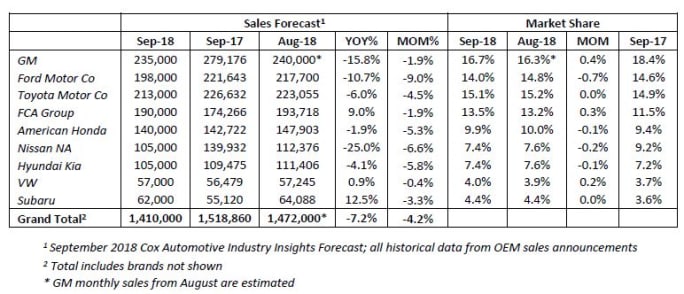

Including fleet sales, Cox Automotive’s September forecast puts new-vehicle sales at 1.41 million units, which would be down 100,000 units, or 7.2%, from September 2017. Compared to August, sales would be down 4.3%.

And despite the decline in sales volume, one less selling day this September vs. last September should cause the sales pace to rise, the company noted. It’s why the firm put September’s SAAR at 17.1 million, which would be down from last September’s record 18.1 million pace.

“A record SAAR in September is very unlikely,” the firm noted. “Sales will need to post 90,000 units above forecast to beat last year’s record,” the firm noted. “Without massive incentives and promotions, a record is not expected.”

The company added that talk of tariffs as well as rising interest rates may be having some pull-ahead impact in the market. “Auto buyers, concerned about the likelihood of higher vehicle prices over the course of the year may be buying sooner than they had originally planned, supporting the higher sales pace.

“Although the market and buying conditions are strong, risks are also rising. Additional interest rate hikes are expected, which will cause a buyer’s monthly payment to increase,” the firm noted. “And previous years of aggressive leasing is now creating a major headwind. Millions of gently-used, high-content vehicles have been returning to dealer lots. Off-lease vehicle volume is expected to peak in 2019, and many potential new-vehicle buyers will be drawn to this value alternative.”

Most manufacturers are expected to post sales declines. Jeep is expected to perform well, as demand for rugged crossovers fits well with their portfolio. Ford and GM are likely to see some larger declines as aging product in some segments, poor car sales, and tighter incentives hold them back.

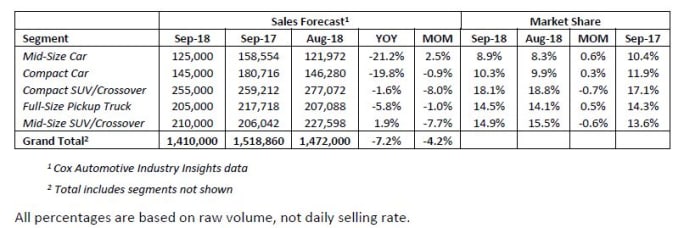

Most vehicle segments should see declining sales vs. last year. Car share may make a modest improvement as higher prices in the used market coupled with newer high-volume products from Honda and Toyota could support new sales.

Looking further ahead, Cox Automotive forecasts a slowing sales pace over the remaining months of the year as buying conditions deteriorate due to higher interest rates and elevated gasoline prices. Steel and aluminum tariffs may also be negatively contributing to sales activity, forcing automakers to hold incentive activity at more modest levels.

“Product costs are rising as a result of higher metal prices, and margins are being negatively impacted,” the firm added. “With less profit margin available, tighter and targeted incentive activity is required. Days supply is also in a relatively stable position, allowing for more pricing discipline.”

The growing volume of gently-used vehicles, which are selling at a 30% to 50% discount to their new versions, also pose a real threat to stronger new-vehicle sales volumes. Despite these headwinds, Cox noted that economic conditions for vehicle buyers remain favorable with strong consumer confidence level and decades-low unemployment rates.

The overall demand for transportation also remains high. Higher interest rates and new trade tariffs are also not chasing away buyers, the firm noted.

Cox’s forecast for full-year auto sale is 16.8 million units, which would be down from 2017’s 17.1 million-unit total.

More F&I

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →

Your Office Is Talking

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

Read More →

F&I Training Fundamentals

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Read More →

Not Just Any Tire Will Do

More consumers and businesses are opting for all-season options for various reasons as safety, sustainability and convenience push practical change.

Read More →