BLACK BOOK: COVID-19 Market Update

Black Book recently published an update to their COVID-19 Market Updates.

Black Book recently published an update to their COVID-19 Market Updates.

Image provided by Black Book

BLACK BOOK – Black Book recently published an update to their COVID-19 Market Updates, which includes:

Current Wholesale Prices & Price Trends, including Auction Volume & Insights and Sales Rates

Used Wholesale Price Trends & Projections, including a Mid-Size Car Segment Highlight (Rental Exposure and Historical Trends of the Segment) & Forecasted Economic Scenarios

A Look at the Retail Vertical, including Retail Prices & Dealer Insights

New Vehicle Sales Outlook, including Forecasted Economic Scenarios

Used Vehicle Supply Projections, including Lease & Rental Unit Returns

With expected downsizing of the fleets, the used values in this segment will experience strong headwinds in the next several months. We project that wholesale values in this segment will be at least 10% lower than pre-COVID-19 projections for the rest of 2020.

Wholesale prices declined 1.5% in May – a substantial improvement compared to April when prices dropped by 5.9%. As a result, Black Book’s Seasonally Adjusted Retention Index had a very respectable comeback in May, only dropping by 0.7% (vs. a 6.9% drop in April). The decrease in April was driven almost exclusively by the collapse in consumer confidence, along with high levels of uncertainty about the financial markets due to the COVID-19 pandemic. During the last five weeks, we have observed the stabilization of prices, as shelter-in-place orders are being relaxed throughout the country. As a result, auction sales volume is finally returning to pre-COVID-19 levels, although most auctions are still operating in a digital only environment. Over the last four weeks, we also measured a substantial increase (compare to previous weeks and compared to last year) in volume of rental units sold, as rental fleet companies are reducing their fleets to match much weaker consumer and business traveler demand.

During the first week of June, wholesale prices continued showing strength, with volume-weighted overall car and truck segments both showing gains for a second week in a row, gaining 0.11% overall. As for specifics, the overall car segments increased 0.16%, compared to 0.21% the prior week. The overall trucks and SUV segments increased again this past week at 0.08% vs 0.04% vs. prior week.

Since the beginning of April, unemployment claims have continued to increase. Last week, the Labor Department reported that the US added 1.88 million new jobless claims, bringing total claims to over 41.5 million since the start of the pandemic. The US unemployment rate in April was 14.7%, the highest monthly rate since the Great Depression. In a surprise to many economists, May unemployment decreased to 13.3% due to the success of the Federal Paycheck Protection Program (PPP) and other stimulus measures. The Labor Bureau also noted in their report that there was a classification error in its survey, and the real unemployment numbers should be about three percentage points higher for both April and May. There is also concern that without further Federal stimulus these gains can be temporary and employment numbers may deteriorate once PPP expires. The unemployment numbers are similar to Black Book’s projections for our Most Likely Economic Scenario, and these were used for short term residual value projections in our recent publication of June residual values.

With a weakening of the economy, consumer confidence is decreasing. The University of Michigan’s Monthly Consumer Sentiment Index was 72.3 points (a slight uptick from April’s 71.8, mostly due to the arrival of stimulus checks). As a comparison, the Index was at 101 in February.

As more economic data, for the second quarter of 2020, arrives, “the GDPNow model [from the Federal Reserve] estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2020 was -53.8 percent on June 4th.”

The overall weakening of the economy is causing demand of vehicle purchases to decline. In addition, gasoline prices reversed the May trend, and started to increase, up $0.20 since the end of April to $1.97 per gallon, according to the U.S. Energy Information Administration.

At the same time, we expect a large, incremental influx of used inventory to hit the marketplace over the next six months, coming from prolonged lease return delays, downsizing of rental fleets (including the expected sell-off of a large number of Hertz’s units – the company proposed selling more than 30,000 cars a month in order to raise cash), increased repossessions, and un-sold inventory from the March-May time period.

As we enter the summer months, we expect both wholesale and retail prices to deteriorate. We attribute this projected decrease to the large influx of incremental used inventory expected to hit the marketplace, the weakening of retail demand due to the deep recession, and corresponding unemployment numbers. On the other hand, due to better than expected (but still very high) unemployment numbers, it is possible that the automotive industry will avoid a more catastrophic economic scenario (severe recession) that was considered as one of the scenarios in residual value projections.

Although the economic effects of the pandemic will continue to be felt as far out as three years from now, we still project that wholesale values will return to the pre-COVID-19 baseline by 2023, as used supply will decline due to cuts in retail and fleet sales throughout 2020 and into 2021.

CURRENT WHOLESALE MARKET OVERVIEW

Auction Insights

Auctions, both physical and digital, continue to be hot with bidding activity and sales rates nearing expectations for this time of year. We’ve heard comments from dealers including, “If I wasn’t watching the news, I would think this was a typical springtime market.”

The cleaner, low mileage units are getting all the attention right now as low new car inventory levels are leaving dealers in need of an attractive alternative for consumers.

Lease extensions and lack of repossessions over the last three months are resulting in some auctions being light on inventory to consign, which is contributing to the increased demand for the quality units that are available.

Auctions that have resumed physical sales continue to report higher conversion rates than ones running on all-digital platforms.

Auction Volume

Despite most auctions continuing to operate under an all-digital platform, sales volume has rebounded to a level consistent with, and some days higher than, the same time last year. This is being driven by strong retail sales, which are then leading dealers to use auctions as a source of inventory. The number of sales bottomed out around an 80% year-over-year decline when most auctions closed their physical sales (and some closed entirely) at the end of March. The graph below illustrates the estimated year-over-year change in sales volume of the wholesale market.

Sales Rate

At the onset of the pandemic, as shelter-in-place orders went into effect, sales rates quickly tumbled into the teens, but rates have been slowly climbing each week. On average, we’ve now seen sale rates remaining at a consistent level each week. Black Book’s estimate of the Weekly Average Sales rate is presented below.

CURRENT WHOLESALE PRICE TRENDS

Market Level View

Volume-weighted, overall car segment values increased 0.16% this past week. Most vehicle segments experienced increases or stability, except for Sub-Compact Car, that has been on a continual decline since the end of March. Again, this past week, the largest increase was the Compact Car segment for a fourth week in a row at 0.59% (the same increase as the week prior). When volume-weighting is applied, the overall Truck segment (including pickups, SUVs, and vans) values increased by 0.08% last week with most of the segments reporting only small upward or downward movements. The Small Pickup segment led the increases for a third week in a row at 1.20%. The surprise this past week is the decline of the Full-Size Van segment at –0.78%, after many weeks with the slowest week-over-week depreciations. The last ten weeks have had average week-over-week depreciations of only –0.27%, compared to the overall truck segment that has averaged -0.69% in the last ten weeks.

The graph below shows week-over-week depreciation rates for the entire market, including Cars and Trucks / SUVs / Vans for the last several months. During the last four weeks we have observed that weekly depreciation rates have started to slow down, and now we are seeing a consistent pattern of increases, particularly within the mainstream vehicle segments.

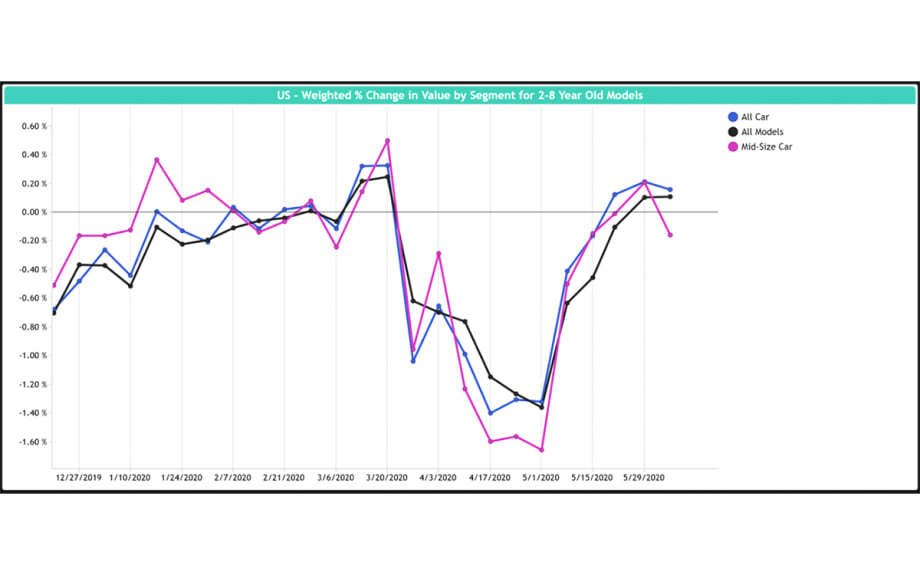

Segment Highlight – Mid-Size Cars

Segment Description

The Mid-Size Car (MSC) segment has evolved over the past decade as shifts in consumer preferences have pushed buyers to crossovers and SUVs. We’ve seen the retirement of models like the Chrysler 200, Dodge Avenger, Mitsubishi Galant, and Suzuki Kizashi over the years, but more recently we’ve seen domestic manufacturers discontinue once popular models such as the Ford Fusion and Buick LaCrosse. At its high point, MSC had a market share of 15-17% between 2008-2013, but the change in consumer tastes has driven the 2020 market share down to 8%. Popular models in this segment include Toyota Camry, Honda Accord, Nissan Altima, Hyundai Sonata, and Kia Optima.

Rental Exposure

MSC has long been a common source for rental companies, but that has also changed with the shift in consumer preferences. Up until 2018, MSC was the biggest source of rental vehicles, but that top spot is now held by the Compact Crossover/SUV segment with MSC coming in second. The highest volume rental units have historically been Chevrolet Malibu, Toyota Camry, Ford Fusion, Kia Optima, Hyundai Sonata, and Volkswagen Passat.

Historical Trends of the Segment

Black Book’s Seasonally Adjusted Retention Index for MSC fared much better than many other segments during the last recession, reaching its lowest level of 98.9 in May 2009, compared to a low of 76.1 in December 2008 for the Compact Crossover segment. As for the COVID-19 impact, the Index fell –8.4% to 107.5 in April but made a slight improvement in May to 107.9 as we saw prices rebound after stay-at-home orders began to be relaxed across the country.

MSC has moved in sync with the overall car segment average for much of the year, with slightly steeper depreciation through the hardest COVID-19-impacted month of April. The 15% rental penetration makes this a segment of concern as all eyes continue to watch the rental market’s reaction. For now, this is a segment that provides a relatively low price point vehicle for many consumers in need of a quality used vehicle.

USED WHOLESALE PRICE PROJECTIONS

Wholesale Price Impact Under the Most-Likely Economic Scenario

Wholesale prices dropped significantly in April as uncertainty over COVID-19 impact and response dampened vehicle demand, resulting in an overall wholesale price decline of 5.9% in April. We saw a substantial improvement in prices during the last two weeks of May and the monthly decrease was limited to only -1.5% in May.

Black Book’s published June Residual Values (dashed lines) reflect a new economic reality – projected values will continue to stay well below pre-COVID-19 projections over the next two years. The green line represents our most-likely economic scenario. A more severe recessionary scenario is shown in red. Projections are indexed to the pre-COVID-19 projections (black line). All values are weighted by the used vehicle sales volume (actual, where available, or projected).

Short-Term Outlook (Summer / Fall of 2020)

We project a drop in wholesale prices compared to a pre-COVID-19 baseline this summer/fall, as the US economy suffers through the effects of COVID-19. We anticipate that wholesale prices will be more than 15% lower than originally projected later this summer and fall due to glut in supply and much weaker demand. Prices will start to recover in 2021 as the economy becomes stronger. We also anticipate that older (>6-year-old), cheaper vehicles in average condition will not decline as much due to increased demand for these units.

Long-Term Projections (36-Month Residual Values, Summer / Fall of 2023)

The effects of the pandemic will continue to be felt, but we project that values will return to the pre-COVID-19 baseline as used supply will decline as a result of cuts in retail and fleet sales throughout the remainder of 2020 and into 2021.

Wholesale Price Impact Under a Severe Recession Scenario

In this scenario, we project a drop in wholesale prices of more than 25% over the summer, compared to a pre-COVID-19 baseline, with a slow recovery in 2021. The effects of the pandemic and recession will still be impactful in 36 months, and we project a 10% market level decline of wholesale prices as compared to pre-COVID-19 projections for the second half of 2023.

Segment Highlight – Mid-Size Cars

Mid-Size Cars represent the second largest segment in the rental fleet market. With expected downsizing of the fleets, the used values in this segment will experience strong headwinds in the next several months. We project that wholesale values in this segment will be at least 10% lower than pre-COVID-19 projections for the rest of 2020.

The graph below shows the expected change in retention value compared to the pre-COVID-19 outlook for base and severe recession scenarios. Projections are indexed to the pre-COVID-19 projections (black line).

RETAIL VERTICAL

Retail Prices

We continue to see decreases in retail asking prices in June as consumer confidence took a dip over last two months. Initially, retail prices were decreasing at a much lower rate compared to wholesale prices – we saw a decrease of about 5% from the peak in early April compared to end of May. We expect retail prices to decline further, and at a higher rate, as consumer demand weakens over the next several months, hence narrowing the gap between wholesale and retail prices.

Dealers Insights

At the center of the dealer conversations we’ve been having is their surprise around the uptick in retail sales. This is leading dealers to be frustrated by the difficulty in sourcing quality used units to backfill what they have sold. Dealers have reported being down by as much as 50% in available inventory. They want to re-stock their lots but are getting outbid by the larger buyers.

Availability of good condition, low mileage, well equipped units continues to be tight and when there is such a unit on the lanes, the amount of bidding activity and the final sale price are reflective of the rarity.

The increase in demand that we’ve seen over the past couple of months due to hard-to-beat new car incentives looks to be fading away as availability of new inventory continues to be a problem. Manufacturers are still struggling to get production back up to speed. There are still some enticing offers out there, but they aren’t quite as sweet as they once were. For example, Chevrolet has now changed its offer from 0% for 84 months to 0% for 72 months.

Dealers are anxiously awaiting new vehicle deliveries. Currently, deliveries are few and far between as the supply chain and assembly lines face challenges in resuming production and deliveries are only arriving from inventory produced prior to the shutdowns. In some cases, it is only a matter of days before dealers are out of some of the high demand models, such as Full-Size Pickups.

Another trend that has arisen out of conversations with dealers is the uptick over the last ten days in service department business.

NEW VEHICLES SALES OUTLOOK

Our New Sales Outlook remains unchanged from last week. We anticipate a significant reduction in US new vehicle sales in 2020 (both retail and fleet sales) due to continued reduced consumer demand. This is a result of several ongoing factors, including less miles driven due to remote work and shelter-in-place initiatives, high unemployment, and an overall feeling of uncertainty by consumers. Overall, new sales were down 23% during the first five months of the year, compared to last year (with a 30% YOY decline in May as most states started to lift shelter-in-place orders). Even as OEMs are restarting assembly lines, there are significant challenges to get back to a normalized production schedule as we reported in previous updates.

In our base economic scenario, we project a 25% drop (compared to pre-COVID-19 projections) in new sales in 2020 to 12.7mm units. In a deep economic recession scenario, we project a 40% drop in new sales in 2020 to 10.2mm units.

In the longer-term, we expect new sales volume to return to pre-COVID-19 levels within five years.

USED VEHICLE SUPPLY PROJECTIONS

Black Book projects a higher than expected used vehicle supply in the wholesale marketplace for the rest of 2020 due to several factors:

Delayed lease returns resulting from lease extensions offered by OEMs – more than 560,000 additional three-year-old units

Extensive de-fleeting by rental car companies, due to lack of consumer and business traveler demand and financial pressure to raise cash – at least 250,000 one- to two-year-old vehicles

Dramatic reduction in auction activities due to COVID-19 in March, April, and May

Increased repossessions due to deteriorating economic conditions in addition to delayed repossessions in April / May

Short Term Lease Return Projections

When we started the year, lease returns were projected to hit a record volume of above 4.1 million units. Once the pandemic was underway and most manufacturing stopped, OEMs started to encourage lease extensions in order to push returns further into 2020 and to be able to provide replacement vehicles. As a result, we project at least 560,000 additional units in the second part of 2020 (compared to the pre-COVID-19 estimates) due to a slowdown in sales in April / May, along with expected turn-ins of the lease extensions.

Rental Unit Returns

Business and leisure travel collapsed at the end of March. We expect a significant reduction in both categories for the remainder of 2020. In addition, there is no expectation that travel will return to pre-COVID-19 levels in the next several years. According to IATA (The International Air Transport Association), air travel will not return to pre-COVID-19 levels until after 2023. This puts tremendous financial pressure on rental companies, that rely on air travel, to reduce both their current fleet and future acquisitions. At the end of May, Hertz filed for bankruptcy in North America as a result of the pandemic.

In addition to Hertz, we expect other rental companies to reduce their fleet during the summer and fall months to match lower demand for rentals. This practice will lead to over 250,000 additional rental units hitting the wholesale market over the next six months. Note that this is a base case scenario in which rental companies (excluding Hertz) can gradually reduce their fleet instead of a rapid-fire sale.

The graph below shows Black Book’s projections for rental returns. The purple line shows the difference between current (darker rectangles) and pre-COVID-19 projections (lighter rectangles).

In the longer term (later 2021 – 2023), the drop in rental return volume will benefit the price of newer used units, as supply will be limited.

Longer Term Used Returns Projections

With the reduction in retail and fleet sales over the next several years, we project approximately 75k used units per month less in the market in three years, compared to previously projected returns. This lower level of used inventory will be beneficial to used car prices as supply will be limited, helping to bolster valuations.

Read: NADA Chairman Rhett Ricart: Our Manufacturers Need Us More Than Ever

More Showroom

Used Market Stabilizes

The Carfax Used Car Index noted a major drop in used-vehicle price increases in July after several months of hikes.

Read More →

California Hybrids Reach State Record

The Golden State still leads the country in electric-vehicle registrations, but much like the rest of the U.S. its hybrid market share is up while full electrics stabilize after a dramatic first-quarter dip.

Read More →

My Mercedes in the U.S.

The German brand debuted its studio dealership concept for the first time in the states in Los Angeles, tapping Americans’ penchant for creative distinctions.

Read More →

Used Sales Hit Summer Drag

The vacation season, combined with high prices, has dented deliveries and added to inventories, though supply is still slim enough to keep listings elevated.

Read More →

California Launches EV Rebate Program

Participating automakers are matching the state's $13.5 million investment in new electric-vehicle rebates scheduled to take effect later this summer.

Read More →

OEM Poll Sees Industry Evolution

Kerrigan Advisors’ survey of automakers finds that tariffs, technology, network tightening and other factors are poised to reshape auto retail.

Read More →

The Trade-In Paradox

Retailing older cars with confidence in today’s market is a matter of establishing and following a clear process that can turn greater profit for auto dealers as they aim to meet used-unit hunger.

Read More →

Focus on Vehicle Cabins

The market for interior materials will grow in coming years as automakers look to meet consumer demand while staying competitive with changeups to sourcing and included features.

Read More →

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →