Manheim Used Vehicle Value Index Jumps Mid-Month

The latest measure shows values have never been higher, an indication there is rapidly growing demand for used-vehicle inventory.

The latest measure shows values have never been higher, an indication there is rapidly growing demand for used-vehicle inventory.

Image provided by Manheim

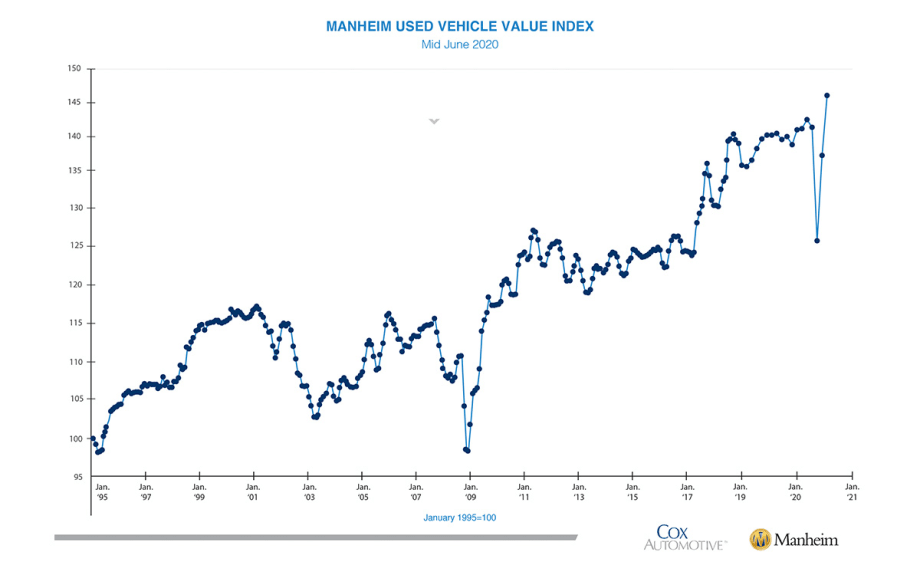

MANHEIM – A mid-June measure of the Manheim Used-Vehicle Value Index is good news for those hoping to see an increase in wholesale used-vehicle values. In fact, the latest measure shows values have never been higher, an indication there is rapidly growing demand for used-vehicle inventory. The team notes wholesale values of used-vehicles at auction are now higher than they were in January.

We continue to see positive recovery trends in the auto market in June.

Wholesale Prices Continue Strong Performance First Half of June

Wholesale used vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) increased 6.6% in the first 15 days of June compared to the month of May. This brought the mid-month Manheim Used Vehicle Value Index to 146.1, a 4.0% increase from June 2019. If the mid-month value of the Manheim Index holds for the full month, the Index will hit an all-time high.

Manheim Market Report (MMR) prices improved again over the last two weeks, resulting in a 3.7% cumulative increase in the first two weeks of June on the Three-Year-Old Index. Over the first 15 days of June, MMR Retention, which is the average difference in price relative to current MMR, was above 100% every day and averaged 102.8%. The MMR Retention trend reflected that vehicles were selling above current MMR values. The weekly price performance in May and June has been more reminiscent of a typical March and April.

On a year-over-year basis, most major market segments saw seasonally adjusted price increases in the first 15 days of June. Luxury cars outperformed the overall market, while most other major segments underperformed the overall market.

Recovering retail sales are reducing vehicle supply. As used retail sales continue to recover, both retail and wholesale supply are coming down. Using a rolling seven-day estimate of used retail days’ supply based on vAuto data, we see that used retail supply peaked at 115 days on April 8. Normal used retail supply is about 44 days’ supply. The most recent seven-day estimate of used retail supply is at 31 days. We estimate that wholesale supply peaked at 149 days on April 9, when normal supply is 23. It was down to 30 days for the most recent seven-day period.

Rental risk pricing improves. The average price for rental risk units sold at auction in the first 15 days of June was up 0.5% year-over-year. Rental risk prices were up 6% compared to May. Average mileage for rental risk units in the first half of June (at 40,500 miles) was down 13% compared to a year ago and down 12% month-over-month.

Coronavirus uncertainty amid economic contraction. Auto loan delinquency rates fell in May, but much of the improvement may be a result of loan accommodations, which were reported by Equifax to be 7.3% of auto loans by the end of May. In May, 1.45% of auto loans were severely delinquent, while 5.19% of subprime loans were severely delinquent. Both rates were higher than last May’s rates. The subprime delinquency rate in May was the highest for the month of May going back to 2006. The initial May reading on Consumer Sentiment from the University of Michigan increased to 78.9 from 72.3 in May. The increase in sentiment was driven by improving views of future expectations as well as current conditions. Consumers also saw improving buying conditions for vehicles and homes. The peak in daily new COVID-19 cases in the U.S. was seven weeks ago, but the new case trend has at best flattened out recently as several areas of the country are seeing an uptick in new cases. Some cities and states are contemplating reimposing lockdown orders. Despite these concerns, we continue to see positive recovery trends in the auto market in June.

Read: EFG’s New Flagship VSC Increases Penetration up to 15 Percent through 25 Million Term Options

Originally posted on Auto Dealer Today

More Showroom

Used Market Stabilizes

The Carfax Used Car Index noted a major drop in used-vehicle price increases in July after several months of hikes.

Read More →

California Hybrids Reach State Record

The Golden State still leads the country in electric-vehicle registrations, but much like the rest of the U.S. its hybrid market share is up while full electrics stabilize after a dramatic first-quarter dip.

Read More →

My Mercedes in the U.S.

The German brand debuted its studio dealership concept for the first time in the states in Los Angeles, tapping Americans’ penchant for creative distinctions.

Read More →

Used Sales Hit Summer Drag

The vacation season, combined with high prices, has dented deliveries and added to inventories, though supply is still slim enough to keep listings elevated.

Read More →

California Launches EV Rebate Program

Participating automakers are matching the state's $13.5 million investment in new electric-vehicle rebates scheduled to take effect later this summer.

Read More →

OEM Poll Sees Industry Evolution

Kerrigan Advisors’ survey of automakers finds that tariffs, technology, network tightening and other factors are poised to reshape auto retail.

Read More →

The Trade-In Paradox

Retailing older cars with confidence in today’s market is a matter of establishing and following a clear process that can turn greater profit for auto dealers as they aim to meet used-unit hunger.

Read More →

Focus on Vehicle Cabins

The market for interior materials will grow in coming years as automakers look to meet consumer demand while staying competitive with changeups to sourcing and included features.

Read More →

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →