Consumers Shopping for Auto Insurance at a Higher Rate Despite COVID-19 Challenges

Newly released TransUnion Insurance Shopping Annual Report uncovers impacts of COVID-19 on personal auto insurance.

Newly released TransUnion Insurance Shopping Annual Report uncovers impacts of COVID-19 on personal auto insurance.

Even with the ongoing economic impacts of the COVID-19 pandemic, overall personal auto insurance shopping rates in the first half of 2020 surpassed 2019 levels.

The state of auto insurance shopping remains uncertain, and it will be critical for insurance carriers to adapt to these changing shopping behaviors and differing consumer needs.

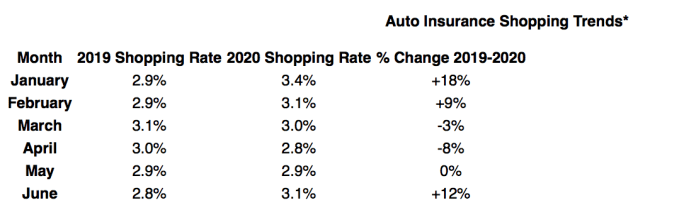

The 2020 Insurance Shopping Annual Report from TransUnion found overall shopping rates were higher year over year in the first few months of 2020 until the week of March 22 – near the onset of the pandemic – when shopping plummeted 14% below the previous year. However, shopping rates reversed in May and have continued to trend higher through June.

Many factors are impacting auto insurance shopping – particularly amidst COVID-19 – and these dynamics vary across generations, regions and financial situations. To better understand these driving forces, TransUnion conducted an online survey of more than 3,000 U.S. auto insurance policyholders, aged 18 years or older, during the week of July 27.

Nearly one-third (30%) of survey respondents said a major life event was a key force behind their decision to shop for auto insurance, followed by a need to reduce expenses due to COVID-19’s impact on household income (24%). Typical life events that drive auto insurance shopping include marriage, having a child, buying a new home, among others. As the COVID-19 pandemic lingers, new life events may be impacting the need for auto insurance shopping, including job loss, reduction in pay, etc.

“While our annual insurance shopping report shows shopping has stabilized for the time being, we will likely see shifts in these trends due to the significant, ongoing financial impacts of the COVID-19 pandemic,” said Mark McElroy, executive vice president and head of TransUnion’s insurance business unit. “The state of auto insurance shopping remains uncertain, and it will be critical for insurance carriers to adapt to these changing shopping behaviors and differing consumer needs. Our latest report helps equip carriers with timely insights to build a reliable basis of trust between insurance businesses and their customers.”

*The above shopping rates are rounded to the nearest tenth; percent change is rounded to the nearest whole number

Before COVID-19 was declared a global pandemic in early March, TransUnion observed insurance shopping rates trended higher on an annual basis for eight straight months. This upward trend was directly correlated to the insurance industry’s increased marketing spend from 2012 to 2019.1

As the pandemic set in and many individuals limited their miles driven, advertising spending fell 2 and carriers turned their attention to positioning themselves as partners in these uncertain times, including through premium rebates. In fact, U.S. auto insurance companies offered about $10.5 billion in insurance premium rebates to customers in an effort to provide COVID-19 financial relief, according to the Insurance Information Institute.

The rebates have proven to be beneficial for both policyholders and carriers. TransUnion’s survey reveals 22% of current auto policyholders considered delaying auto insurance payments due to COVID-19. And for the policyholders who recall being contacted by a carrier about a premium relief or discount (45%), six in 10 (61%) said the gesture increased their loyalty to their auto insurer.

Simultaneously, in the time since shopping bottomed out in April, TransUnion observed shopping rates rebound in May to 2.9% and continue into June at 3.1%, exceeding the June shopping rates in both 2019 and 2018.

“While the rebound in shopping rates for May and June is a positive movement, it’s too soon to determine whether this trend will continue given the variety of factors likely at play,” said David Drotos, vice president of insurance solutions at TransUnion. “As highlighted in the 2020 Insurance Shopping Annual Report, we’re seeing premium rebates, stimulus checks and expanded unemployment benefits through the CARES Act likely contributing to this increased shopping activity. These considerations will be integral for carriers and shoppers in navigating the uncertain days ahead.”

Younger consumers driving auto insurance shopping likely due to the differing financial impacts of COVID-19

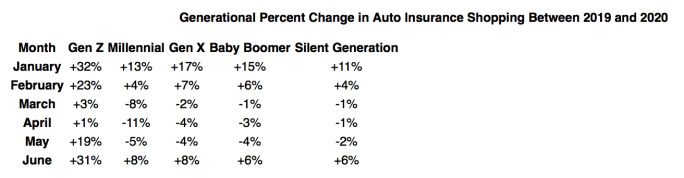

In the first half of 2020, younger generations continued to drive increased shopping rates when compared to older generations. The report found Gen Z had a sharp spike in shopping year over year for Q1 2020 compared to all other generations. This spike was subsequently followed by a dip at the beginning of Q2 across all generations, though more pronounced for Gen Z and Millennials, and rates have since rebounded.

While the industry has seen shopping driven by younger drivers in recent years, the negative economic impacts of COVID-19 are likely intensifying these trends as younger generations face more financial challenges and price sensitivities. TransUnion’s survey of auto policyholders found a higher percentage of younger consumers have had their household income negatively impacted by COVID-19 compared to older consumers (Gen Z: 61%; Millennial 60%; Gen X: 55%; Baby Boomers: 44%).

“Differences in shopping behavior have become more acute in 2020 as a result of exacerbated disparities due to the pandemic, particularly when comparing across generations and financial situations. As social and economic circumstances continue to evolve throughout 2020, carriers can use these insights to build a deeper understanding of what drives consumers to shop as well as their customers’ needs amidst the uncertainty ahead,” concluded Drotos.

TransUnion is hosting a webinar on September 17 at 1:00 p.m. CT titled, “You Can Quote Me: Trends and Insights in Insurance Shopping.” Insurance industry professionals that are interested in learning more can register for the webinar here.

The 2020 Insurance Shopping Annual Report also arms carriers with auto insurance shopping trends by region, macroeconomic impacts, state GDP, customer risk and asset ownership, among others. For the complete study, please click here.

1 TransUnion internal insurance shopping data, January 2019–June 2020

2 Mintel - Estimated direct mail volume for P&C insurers January-May 2020

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →