COVID-19 Market Insights

Black Book recently published an update to their weekly COVID-19 Market Update report.

Black Book recently published an update to their weekly COVID-19 Market Update report.

IMAGE: Black Book

BLACK BOOK – Here is a quick recap of industry related headlines over the last week:

Wholesale prices continued their decline last week, for the seventh week in a row.

Average retail listing prices of available inventory was essentially flat last week.

Wholesale sold volume decreased substantially in September compared to 2019 as the wholesale market turned in the middle of the month. It appears that the volume rebounded in October but is still lower that it was in 2019.

Used retail listing volume continued to increase last week, but it remains at levels lower than last year – about 2.6% below a prior year, and 12% below where the industry started 2020.

Weekly initial unemployment claims dipped under 800,000 in last week’s DOL after California has completed its pause in processing of initial claims, and has resumed reporting actual unemployment insurance claims data.

University of Michigan released the preliminary Index of Consumer Sentiment for October, and it stood at 81.2 – a slight increase from September, but still about 20% below pre-COVID levels.

Hertz is planning to close all of their retail sales locations.

In an interview with Automotive News, new Chase Auto CEO Peter Muriungi acknowledged that between 7 and 8 percent of all automotive accounts were in hardship over the Summer months (matching an industry average). Most of them (about 90%) have moved out of that status.

Last Week’s Highlights from the Wholesale Market

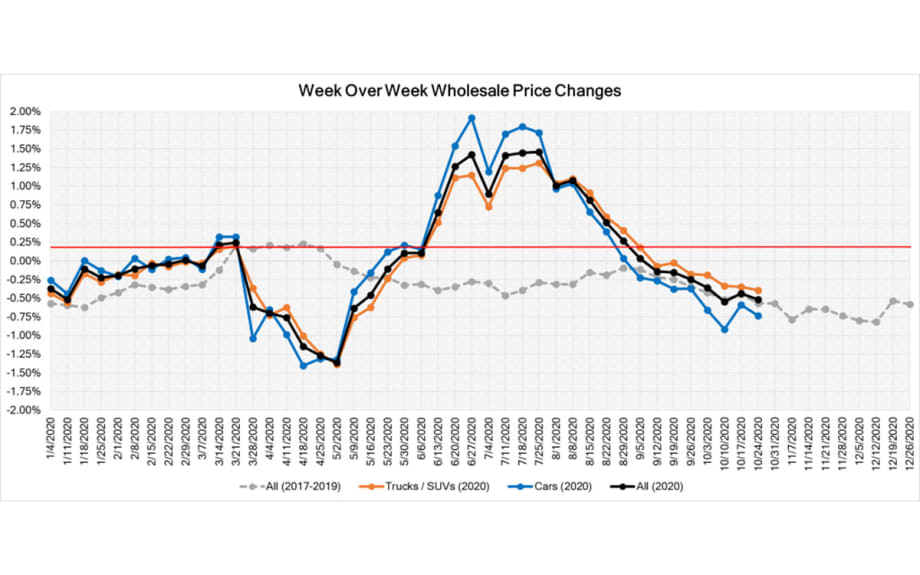

Volume-weighted, overall Car and Truck segments both experienced continued softening in values, with the overall market decreasing by –0.52% this past week (compared to –0.43% the prior week). As for specifics, the overall Car segments decreased –0.74% (compared to –0.59% the prior week), and the overall Truck and SUV segments decreased this past week at a rate of –0.39% (compared to a decrease of –0.35% the prior week).

The graph below shows week-over-week depreciation rates for the entire market, including Cars and Trucks/SUVs/Vans for the last several months. We also show an average weekly change from several previous years (grey line).

News from the Retail World (Used and New)

Retail prices fell two weeks ago but have since stabilized. However, not all segments are performing equaly. As has been the case with with the wholesale market, the overall retail market is being skewed by the strength of the Full-Size Trucks and certain SUV segments that continue to garner a higher price. Other segments, such as Compact Cars and Compact Crossovers, are seeing larger declines in retail prices due to a larger supply in the market.

The highly anticipated GMC Hummer EV debuted last week and is expected to come to market late next year. The initial release will be for the Edition 1 and will carry a price tag of $112,595. The all-electric vehicle will not only be off-road capable, but fast with a 0-to-60 time of three seconds.

The 2020 New York Auto Show was canceled, but the 2021 show now has new dates, August 20-29. Originally, it was scheduled for April 2-11, but due to ongoing virus concerns and an expansion of the convention center the dates were moved.

What Comes Next?

We are starting to see an incremental influx of used inventory coming to the marketplace. We expect this to last into the first half of 2021, It is the resultof prolonged lease return delays. Presently it appears that most of these vehicles never make it to auctions, as grounding dealers keep the inventory for retail sales. In addition, lenders have re-started the process of repossessions, as the economy continues to feel the effects of high unemployment. With much weaker retail demand without second federal stimulus, and a projected oversupply of used inventory, we forecast a significant drop (steeper than usual end of the year seasonality) in wholesale prices this fall and winter, relative to the heights seen in recent months.

Longer Term View

Although the economic effects of the pandemic will continue to be felt as far out as three years from now (for example, the recent Federal Reserve projections in September show unemployment above 4% for the foreseeable future), Black Book projects that wholesale vehicle values will return to at least the pre-COVID-19 baseline before 2023. Used vehicle supply will decline significantly due to cuts in lease and fleet (both rental and commercial) sales throughout 2020 and into 2021.

Economic Conditions

Job Market

The graph above compares weekly initial unemployment claims from the current recession against the Great Recession of 2007 – 2009. The severity and speed of job losses during this crisis is unprecedented. The horizontal (x) axis is an offset (in months) from the beginning of the recession, with week 0 being the week of March 21st.

Last week, the Labor Department reported that the US added 787,000 new jobless claims – a decrease of 55,000 from the revised prior week’s numbers.

Since March, we have seen 31 consecutive weeks of record layoffs and furloughs, indicating that businesses are still struggling to start a full recovery.

In the early stages of the crisis, the US unemployment rate in April skyrocketed to 14.7%, the highest monthly rate since the Great Depression.

The May unemployment level decreased to 13.3% due to the success of the Federal Paycheck Protection Program (PPP) and other stimulus measures enacted in part by the Federal Reserve and Government.

As the country and the economy continued to reopen during the early part of June, the monthly unemployment numbers eased further to 11.1% and dropped to 10.2% in July.

In August, we saw further improvement in the labor market as the unemployment rate fell to 8.4%.

The September unemployment number dropped to 7.9% mostly due to exit of large number of people from the employment pool. Additionally, job gains slowed down significantly.

The Labor Bureau also noted in its reports that there was a classification error in its surveys, and the real unemployment numbers were higher for each month since March, as illustrated above.

There is concern that without further federal stimulus, these gains will be temporary and employment numbers may deteriorate.

This recession is very different and unprecedented in the labor market – reflecting an almost instantaneous jump in unemployment with projected fast growth and recovery within several years. The graph above compares unemployment rates for the last several major recessions. The horizontal (x) axis is an offset (in months) from the beginning of the recession.

Although we have seen a reduction in unemployment claims, the initial economic shock and job losses have created a deep hole for us to dig ourselves out of. Between February and the end of September, the nation lost close to 10.7 million jobs.

Consumer Confidence

Not surprisingly, consumer confidence has been on a rollercoaster over the last six months.

At the beginning of the year, sentiment was strong – the University of Michigan’s Monthly Consumer Sentiment Index in February was at 101 points.

As the COVID-19 pandemic spread across the US, the Index dropped to 71.8 points in April and increased slightly to 72.3 points in May.

During testimony by Federal Reserve Chair Jerome Powell, he noted that during the months of April and May, “stimulus checks and unemployment benefits are supporting household incomes and spending.”

With these one-time stimulus payments and extended unemployment benefits helping the economy, the Index for June increased further to 78.1. The gains, however, were not uniform across the country. With a significant reduction in the number of COVID-19 cases, the Northeast region led the way with a record 19.1 points month-over-month jump, while the Southern region rose just 0.5 points due to the dangerous increase in numbers of new infections and fear of further shutdowns.

With a weakening of the economy and the increase in new COVID-19 cases across the South, consumer confidence retracted to the lows of April in July. The University of Michigan’s Monthly Consumer Sentiment Index for July decreased to 72.5 points and increased slightly in August to 74.1.

September Index increased further to 80.4, but still remains heavily depressed compared to pre-COVID and last September’s numbers.

Preliminary numbers for October stood at 81.2 points – a slight improvement since September and the highest point since April’s drop.

Gross Domestic Product (GDP)

The Bureau of Economic Analysis published the third estimate of GDP in the second quarter (as of September 30th) – real GDP decreased at an annual rate of 31.4%. This was the highest drop in GDP ever recorded.

Consensus states that the economy will start to grow in the third quarter, as compared to the previous one. The current “nowcast” from the GDP Now model [from the Federal Reserve] estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2020 was 35.3% on October 20th.

Delinquencies in Automotive Lending

The number of accounts in ‘hardship’ jumped substantially in April, and kept increasing through June across all risk groups, according to the Monthly Industry Snapshot by TransUnion. The numbers stabilized in July and improved in August – currently, about 4.3% of all accounts are in hardship – this is roughly an 800% increase over last year. The increases are across all risk tiers. As deferrals expire in the upcoming month, coupled with a high unemployment rate, lenders expect a large portion of these ‘hardships’ to become delinquencies.

The numbers are substantially higher for sub-prime tiers – as of August, about 12% of all subprime automotive accounts were in hardship.

According to the “Senior Loan Officer Opinion Survey on Bank Lending Practices” from the Federal Reserve, lenders started to tighten standards on auto loans during the first half of 2020. Board of Governors of the Federal Reserve System released results from the third quarter that showed a substantial increase in the number of banks that have tightened their standards.

Gas Prices

Gasoline prices reversed their May trend and started to increase. Since their lowest point at the end of April, prices are up $0.38, to $2.15 per gallon last week, two cents decrease from the prior week, according to the U.S. Energy Information Administration.

Current Wholesale Market Overview

Auction Insights

Volume is starting to show signs of growing for some remarketers, but not necessarily in the hottest segments. This is leading them to lower their floors to sell inventory.

Dealers are reporting that they are starting to send more unwanted units to auctions. This is great news as auctions have been low on available volume after the strong sales that were experienced over the summer months.

Full-Size Trucks continue to perform well at auctions, especially the 2500 and 3500 level domestic trucks that are short on new inventory supply.

The big buyers were very active over the summer and would pay any cost to secure inventory, but over the last several weeks we’ve seen their buying decline. They continue to be very active in their bidding, but they aren’t the final, successful bidder as often.

Auction Volume

Over the last several weeks we have seen the wholesale sold volume decrease as dealers started to pull back on purchasing.

The drops in volume were not uniform across all auctions and platforms.

We saw a significant drop in sold volume (both, month-over month and year-over-year) in wholesale channels in September. There are several factors that contributed to this drop:

The no sale rate increased in September as many remarketers were not willing to adjust price floors.

We also saw a decrease (YOY) in available units:

Rental companies held back some units to cover Hurricane related rentals.

Repossessions are slow to hit the market as the process slowed down significantly compared to pre-COVID days.

The graph below illustrates the estimated year-over-year change in the monthly sold volume in the wholesale market. The summary includes all major wholesale channels including open auctions (digital and physical), dealer-to dealer platforms, direct to dealer sales, etc.

Sales Rate

At the onset of the pandemic, as shelter-in-place orders took effect, sales rates quickly tumbled into the teens.

Subsequently, rates began climbing each week before finally stabilizing in June and July.

After months of consistently strong sales, much of seller’s best inventory was sold and retail demand began to soften in certain segments. As a result, sales rates started to decline.

Sales rates have stabilized in recent weeks as sellers have adjusted floors to reflect the weakening wholesale values.

Black Book’s estimate of the overall Weekly Average Sales rate is presented below.

Current Wholesale Price Trends

Current Market Level View

Volume-weighted, overall Car segment values decreased -0.74% over the last week, an increase in depreciation from the –0.59% decrease experienced the week prior.

Compact Cars have been extremely volatile throughout the pandemic, with a sharp fall initially, then followed by a steady rebound. However, the values have been consistently falling since the last week of August. This past week, the Compact Car segment experienced the largest Car segment decline at –1.62%.

After 20 weeks of increases and/or stability, the Premium Sporty Car segment showed the first signs of declines with a small –0.09% depreciation this past week.

When volume-weighting is applied, the overall Truck segment (including pickups, SUVs, and vans) values declined -0.39% last week, slightly larger depreciation compared to the previous week decrease of –0.35%.

Sub-Compact Crossovers are a newer segment in the market, but consumer preference is still for the larger crossover/SUV options. This is leading to large declines week after week for this segment. The past 4 weeks have had an average rate of decline exceeding 1%.

Full-Size Trucks remain in short supply on dealer lots and this is holding their weekly depreciations low. However, Small Pickups have increased their rate of decline, with a -1.11% change this past week.

Black Book’s Seasonally Adjusted Retention Index

The graph above compares Black Book’s Seasonally Adjusted Retention Index for the 2019 and 2020 calendar years. The Black Book Used Vehicle Retention Index is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically equipped MSRP. It is weighted based on registration volume and adjusted for seasonality, vehicle age, mileage, and condition. The Index offers an accurate, representative, and unbiased view of the strength of used vehicle market values. It measures an ‘apples-to-apples’ year-over-year retention comparison.

2020 started slightly below 2019 levels, but the market showed early strength in February and March.

As the US economy shut down due to the COVID-19 pandemic, we measured the highest single month drop in April of 6.9 points since launching the Index.

As we entered July, wholesale prices continued the rebound that began during the second half of May and continued through the month of June, with June’s Retention Index climbing back to pre-COVID-19 levels with a record jump of 9.1 points.

Black Book’s July Index value jumped above 2019 to 126.0 points as wholesale prices continued their climb.

August Retention Index jumped further to 129 points – the highest retention level ever recorded since the inception of the Index in 2005.

Our September index came at 130.8 – 1.4% increase from August and 12.8% higher than in 2019. Market strength was driven mostly by the Full-Size Pickup segment.

Our “nowcast” for October shows a decline in Index to about 128 points.

During the last recession (2007-2009), the Index declined by about 15 points in a span of 12 months before recovery started. We project that the Index will decline over the next five months after experiencing the summer’s strength. The graph below shows the historical trends in Black Book Retention Index that covers the last 15 years including the Great Recession.

Used Wholesale Price Projections

Wholesale Price Impact Under the Most-Likely Economic Scenario

2020 In Review

The wholesale market started the year strong from January through March, as prices increased during the first quarter.

Wholesale prices dropped significantly in April, as uncertainty over COVID-19’s impact and response dampened vehicle demand. This resulted in an overall wholesale price decline of 5.9%.

We saw a substantial improvement in prices during the last two weeks of May as many states re-opened their economies, and the monthly decrease was limited to only -1.5%.

During the summer months, demand in the automotive market was fueled by federal government stimulus and delayed tax season. Additionally, used and new inventory shortages drove wholesale prices up.

In June, wholesale prices continued to increase, and the overall market appreciated by 5.7%. As a comparison, last year’s prices declined by 0.9% over the same period.

Wholesale prices increased by a record 7.0% in July.

Wholesale prices continued their ascent in August and increased by an additional 2.7%.

Prices started to decline in the first week of September and by the end of the month declined by 1.0%. Performance varied by segment with the strength coming from Full-Size Pickup (which increased by 1.2%).

As retail demand weakens and used supply starts to come to the market, wholesale prices are declining at an accelerated rate (compared to prior years, excluding Full-Size Pickup Segment) – we observed a 2.0% drop in prices in the first three weeks of October.

Short-Term Outlook

The graph above shows a market level weighted average projected (dashed lines) and historical (solid line) wholesale values for all 2017 model year models. The green line represents our most-likely economic scenario, which does not include a possible second wave of COVID-19, as well as a still undefined second stimulus package. A more severe and prolonged recessionary scenario is shown in red.

We project a drop in wholesale prices this Fall, as the US economy suffers through the effects of COVID-19, and due to an expected glut in supply. Prices will start to recover in 2021 as the economy becomes stronger.

We also anticipate that older (>6-year-old), cheaper vehicles in average condition will not decline as much due to increased demand for these units.

Long-Term Projections (36-Month Residual Values, Fall of 2023)

The effects of the pandemic will continue to be felt out to 36 months from now. We project that values will return to the pre-COVID-19 baseline as used supply will decline due to cuts in retail and fleet sales throughout the remainder of 2020 and into 2021.

Used Retail Vertical

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space.

From the peak in early April, until the end of June, retail listing prices decreased by about 4%.

Since the second week of June, we have seen an increase in used retail prices fueled by higher consumer demand due to stimulus payments, the federal Paycheck Protection Program (PPP), and limited used and new inventory.

Since early August, used retail prices rebounded to above pre-COVID-19 levels.

We expect used retail prices to decline later in the fall as demand will decline in the absence of stimulus payments during a weak economy.

Used Retail Inventory

Many dealers continue to report a shortage of used inventory in the wholesale marketplace. As a result, from the peak in February, we have seen a decline in the number of used retail listings by between 20% and 25%. Current inventory level is about 20% below where we started the year.

The true shortage of vehicles is probably not as severe as this decline would lead you to believe, as many dealers sell some of their best inventory in the first several days before listing them online. Nevertheless, the shortage of used inventory helps keep retail prices elevated even in the weak economic conditions.

The graph above shows the weekly average of the number of retail listings collected by Black Book, indexed to the first week of the year. We see a continuous decline in the numbers starting at the beginning of May as the economy started to open in the states outside of the Northeast.

The graph below shows year-over-year change in average monthly retail listings.

We started 2020 with active retail listings above previous year’s levels.

By July, the listing volume dropped to about 7% below 2019 numbers.

August saw another drop in listed inventory to about 9% below 2019.

In September, inventory listings continued to grow and were about 6% below 2019.

Currently, the number of listings is about 2.6% lower compared to last year.

Used Retail vs. Wholesale Prices Trends

Each week, members of the Black Book automotive analyst team, data science team and executive leadership team speak with no less than 30 dealers, along with buyer and seller representatives, wholesalers and others, who represent hundreds of franchise and independent dealers nationwide. These industry experts, along with experts we speak with from leading fleet management and rental car companies, auction leadership, and other industry experts, help to clarify and connect the dots between the wholesale and retail markets, adding to the insights that our data reveals.

Since the start of the pandemic, we have been observing different trends in both wholesale and retail prices (see graph below).

In April and May, wholesale prices declined at a higher rate compared to retail prices. As margins grew, dealers reported healthy profits on a per vehicle basis. Retail prices displayed stickiness on the way down.

Similarly, as wholesale prices came roaring back to pre-COVID-19 levels in July and August, retail prices were slow to recover, exhibiting the same stickiness on the way up.

As the wholesale market started to decline in September, we began to experience the early stages of our expectations that both wholesale and retail prices will decline significantly over the remaining months of 2020.

The graph below captures this retail / wholesale dynamic since the start of the year. Prices are indexed to the first week. The black line is Black Book’s Retention Index (not adjusted for seasonality). It is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically equipped MSRP. It is weighted based on registration volume and adjusted for vehicle age, mileage, and condition. The blue line is a retail index – average listing price of available retail inventory adjusted for mileage.

New Vehicles Sales Outlook

We still anticipate a significant reduction in US new vehicle sales in 2020 (both retail and fleet sales) due to a continued reduction in consumer demand. This is the result of several ongoing factors, including less miles driven due to remote work and shelter-in-place initiatives, high unemployment, and an overall feeling of uncertainty by consumers.

Overall, new vehicle sales were down 18.8% during the eight months of the year compared to last year (with a 6% YOY increase in September). The graph below shows our current projections for new vehicle sales for the remainder of 2020.

Our New Vehicle Sales Outlook was updated based on stronger than expected August sales numbers. Due to continuous production disruptions and much weaker demand due to the economic slow-down, we project a 20% drop (compared to pre-COVID-19 projections) in new sales in 2020 to13.6mm units in our base economic scenario.

In the longer-term, we expect new sales volume to return to pre-COVID-19 levels within five years.

Used Vehicle Supply Projections

Black Book projects a higher than expected used vehicle supply in the wholesale marketplace for the rest of 2020 due to several factors:

Delayed lease returns resulting from lease extensions offered by OEMs – more than 560,000 additional three-year-old units in the second half of 2020.

Extensive de-fleeting by rental car companies due to lack of consumer and business traveler demand, and financial pressure to raise cash – at least 250,000 one- to two-year-old vehicles will be added to the market in the second part of 2020.

Increased repossessions due to deteriorating economic conditions in addition to delayed repossessions during spring and summer months – we expect the volume of repossessed vehicles to at least double in the next six months compared to last year. This additional volume could exceed 1.0 million additional units in the next 6 months.

Short Term Lease Return Projections

When we started the year, lease returns were projected to hit a record volume of above 4.1 million units. Once the pandemic was underway, and most manufacturing stopped, OEMs started to encourage lease extensions in order to push returns further into 2020, when they would be able to provide replacement vehicles. As a result, we project at least 560,000 additional units in the second part of 2020 (compared to the pre-COVID-19 estimates) due to a slowdown in sales in April / May, along with expected turn-ins of the lease extensions. So far, a large portion of these units are being kept by grounding dealers and not being sent to the auctions.

Repossessions

About 1.9 million vehicles were repossessed by lenders and sold (mostly) through wholesale channels in 2019. During the beginning of the pandemic, most states put a moratorium on auto repossessions and most lenders had deferral programs to help owners through the first several months of the recession. Most of the lenders have ended their deferral programs. Our survey of lenders and automotive recovery companies suggest that the volume of repossessed vehicles will at least double in the next six months. We expect that there will be substantial challenges at every step of the process as recovery, transportation, and disposal are not fully recovered.

Rental Unit Returns

Business and leisure travel collapsed at the end of March – air travel is still down by more than 70% according to the TSA. We expect a significant reduction in both categories for the remainder of 2020. In addition, there is no expectation that travel will return to pre-COVID-19 levels over the next several years. According to the IATA (International Air Transport Association), air travel will not return to pre-COVID-19 levels until after 2023. This puts tremendous financial pressure on rental companies that rely on air travel to reduce both their current fleet and scrutinize future vehicle acquisitions.

At the end of May, Hertz filed for bankruptcy in North America as a result of the pandemic. Hertz was able to secure a deal with its lenders that allows a gradual reduction of fleet – over 182,000 units between June and December. In addition to Hertz, we expect other rental companies will continue to reduce their fleet during the fall months to match lower demand for rentals. This practice will lead to over 250,000 additional rental units hitting the wholesale market in the second half of 2020.

In the longer term (later 2021 – 2023), the drop in rental return volume will benefit the price of newer used units, as supply will be limited.

The graph below shows Black Book’s projections for rental returns. The purple line shows the difference between current (darker rectangles) and pre-COVID-19 projections (lighter rectangles).

Longer Term Used Returns Projections

With the reduction in retail and fleet sales over the next several years, we project a substantial decrease of available used inventory in the years to come. The graph below illustrates the numbers of returned vehicles up to 8-years-old. This lower level of used inventory will be beneficial to used car prices as supply will be limited, helping to bolster valuations.

More Showroom

Mitsubishi Sets Growth Strategy, Structural Transformation

The Japanese automaker aims to 'strengthen products and technologies that embody its brand identity,' focus on its strongest markets and expand value-chain businesses 'that leverage its unique strengths.'

Read More →

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →