Specialty Market Insights

Black Book recently released an update to their Specialty Markets Update report.

Black Book recently released an update to their Specialty Markets Update report.

BLACK BOOK – Black Book recently released an update to their Specialty Markets Updates report.

Powersports values continue to show COVID-19 fueled strength as we enter 2021, though the rate of increase has slowed from last year. Nearly all segments are up for January, despite this being the historical low point for values in a typical year.” – Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

Segment Performance

Snowmobiles are our biggest gainers this month, up a little over 2.0%. This segment had the least growth in values last year, but most dealers are expecting the same market conditions that drove motorcycle and other powersports values to record heights in 2020, will do the same for the sleds now that winter is here.

Dealers are still having a tough time getting enough inventory, both new and used, to keep showrooms fully stocked. Until both the manufacturers and the remarketing industry can supply more units, prices are likely to remain elevated.

2020 will go down as a historic year for many reasons, among them that from January to December, powersports values across the board increased by an average of 21.1%. This ranges from a low of 4.4% for Snowmobiles, to an eye-popping 40.7% for the Off-Road bikes.

Segment Spotlights & Industry News

Cruiser Performance

Once again as we start 2021, the Cruiser segment is still showing COVID-19 fueled strength. This is likely to continue for the immediate future, as we are now entering the traditional period of increasing values for these bikes.

Off-Road Performance

2021 starts off with the first decline in values for the Off-Road segment we have seen since last winter. The drop was exceedingly small, but marks the end of a remarkable run for these bikes. Despite this, we still see this segment as being a strong performer going forward.

Industry News & Notes

The Federal Government is starting to implement the second round of PPP loans administered through the Small Business Administration. Powersports dealers should see if they are eligible for the forgivable loans. Even if they can’t benefit directly from the revived PPP program, they should see some spillover benefits from the general stimulus of more money flowing into the broader economy.

Powersports Business News recently reported that major unit sales at Powersports dealers rose an average of 26.3% for the first eleven months of 2020 compared to the prior year according to data from CDK Lightspeed DMS.

This year’s AIME expo, which was cancelled late last year, is being held virtually as the AIMExpo Connect digital powersports event January 21-22. With vaccines now rolling out, hopefully in-person trade shows and events will start to be rescheduled for later in the year.

Recreational Vehicles

“The values of used RVs sold at wholesale auctions have once again reached all-time highs. This is the fourth consecutive month of record setting values for towables, and the third out of four for motorized units. This continued popularity of used units mirrors what we’re seeing on the new side, where although manufacturers are reporting record shipments, dealers say they still don’t have enough inventory.” – Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Hit Another All Time High

For Motor Homes (including Class A, B, and C)

Average selling price was $60,067, up $6,466 (12.1%) from the previous month.

One year ago, the average selling price was $45,384.

Auction volume was down 3.8% from the previous month. The average model year was 2013.

For Towables (including Travel Trailers and Fifth Wheels)

Average selling price was $19,346, up $150 (0.7%) from the previous month.

One year ago, the average selling price was $14,121.

Auction volume was up 7.9% from the previous month. The average model year was 2014.

Industry Highlights

According to the RVIA, the total number of RVs shipped in November rose to 42,513, a record for the month, and an increase of 43.4% over November 2019. Towables totaled 38,485 units and motorhomes accounted for 4,028. Year end totals are projected to reach 423,628, which would be the fourth best year ever.

Due to public health and safety concerns, the Boston RV and Camping Expo and the Louisville Boat, RV, and Sports Show have been canceled.

The Florida RV Supershow, the largest in the country, is scheduled to be held as usual, but is requiring attendees to wear masks when inside and have their temperature checked prior to entry.

RV Retailer completed their purchase of Northgate RV and Family RV Group, adding 14 dealerships and bringing their overall total to 52 stores in 15 states.

Lazydays opened their new 42,000 square foot location in Nashville, which brings their total number of dealerships to 11.

Thor Industries purchased Tiffin Motorhomes, a maker of high-end Class A RVs, for $300 million.

The Baird Recreation Sector Index improved to 70 in December from 64 in November, with the three to five year outlook rising to 67 from 65.

Winnebago reported revenue of $793 million for their first fiscal quarter of 2021, an increase of 35%. They also reported a market share of roughly 11%.

Statistical Surveys, Inc. reported there were 29,355 RVs registered in North America during November, an increase of 27.5% over 2019, with year to date registrations are up 9.5

Collectible Cars

Health and public safety concerns have forced most of the Scottsdale auctions to reschedule, move to alternate locations, or change to a primarily digital format. Mecum was able to hold their usual large scale January auction in Kissimmee, Florida with minimal changes, and initial reports stated that sales were in line with their typical results.” – Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

Barrett-Jackson has announced they have rescheduled their flagship Scottsdale auction to March 20-27. This is their 50th Anniversary sale, so they wanted to wait until it could be held with as few restrictions as possible to allow maximum attendance and enjoyment.

RM Sotheby’s will be holding their Scottdale auction January 22nd at the OTTO Car Club, and is promoting it as a livestream auction with very limited in-person attendance. They will offer approximately 80 vehicles, primarily European exotics and other high-end collectibles.

Worldwide Auctioneers relocated their auction to their headquarters in Auburn, Indiana on January 23rd. They will offer about 65 vehicles, including the Steelewood Woodie Wagon Collection.

Bonhams will be holding their Scottsdale auction January 21st at the Westin Kierland Resort and will be offering roughly 40 vehicles.

Mecum held their Kissimmee, Florida auction January 7 – 16 at the Osceola Heritage Park. They describe it as the world’s largest collectible car auction, and typically sell between 2,000 – 2,500 vehicles and record sales totals of over $100 million. In 2020, 2,140 vehicles were declared sold for a total of $105 million, and this year’s preliminary numbers show a slight decline in the number of vehicles sold, but a slight increase in overall dollar amount. Last year’s headliner, the 1968 Ford Mustang Fastback that Steve McQueen drove in Bullitt, brought $3.7 million, and this year’s was Carroll Shelby’s personal Cobra 427, which sold for nearly $6 million. A very similar vehicle sold for $1.375 million a day later, indicating a roughly $4.5 million bump for the Shelby provenance. Other top sellers include the first L88 Corvette ever built (a 1967 Tuxedo Black convertible), a pair of Mercedes-Benz 300SLs, and two third generation Ford GTs.

Bring A Trailer, the popular online auction site, continues to thrive during this time of reduced travel opportunities and increased social distancing. They often make headlines for selling relatively normal used cars with especially low mileage for surprisingly large amounts, but also sell their fair share of traditional collectibles. A few recent results include a 1957 Porsche 356A Speedster for $400,000; 2007 Mercedes SLR McLaren for $605,000; 1982 Lamborghini Countach 400S for $425,000; 1968 Ferrari Dino 206 GT for $596,000; and a 1994 Jaguar XJ220 Coupe for $420,000.

Notable Recent Auction Sales Include:

1965 Shelby 427 Cobra Roadster $5,940,000 (Mecum)

1967 Chevrolet Corvette Convertible L88 $2,500,000 (Mecum)

1956 Mercedes 300SL Gullwing $1,567,500 (Mecum)

1967 Shelby 427 Cobra Roadster $1,375,000 (Mecum)

1957 Mercedes 300SL Roadster $1,210,000 (Mecum)

1965 Iso Grifo A3/C Coupe $1,182,500 (Mecum)

2018 Ford GT Heritage Edition Coupe $990,000 (Mecum)

1971 Plymouth Cuda 440 6-Bbl Conv $962,500 (Mecum)

2018 Ford GT Coupe $880,000 (Mecum)

1969 Chevrolet Camaro ZL1 Coupe $825,000 (Mecum)

Market Trends

The Vintage American Post War Classics segment represents “big American iron” produced from the mid-1940s up through the mid-1970s. This encompasses a wide range of vehicles, and the prices can correspondingly range from the mid-teens up to the low six figures. A few representative examples would include 1953-54 Buick Skylark, late 1950s Cadillac Eldorado (Seville and Biarritz), 1955-57 Chevrolet Bel Air, Ford Crown Victoria, Lincoln Mark III, Chrysler 300 Letter Series, and Pontiac Bonneville. These vehicles have been squarely at the heart of the hobby for decades, but shifting tastes have led to a gradual decline in their values as older collectors age out of the hobby and are replaced with younger ones who grew up being interested in different cars.

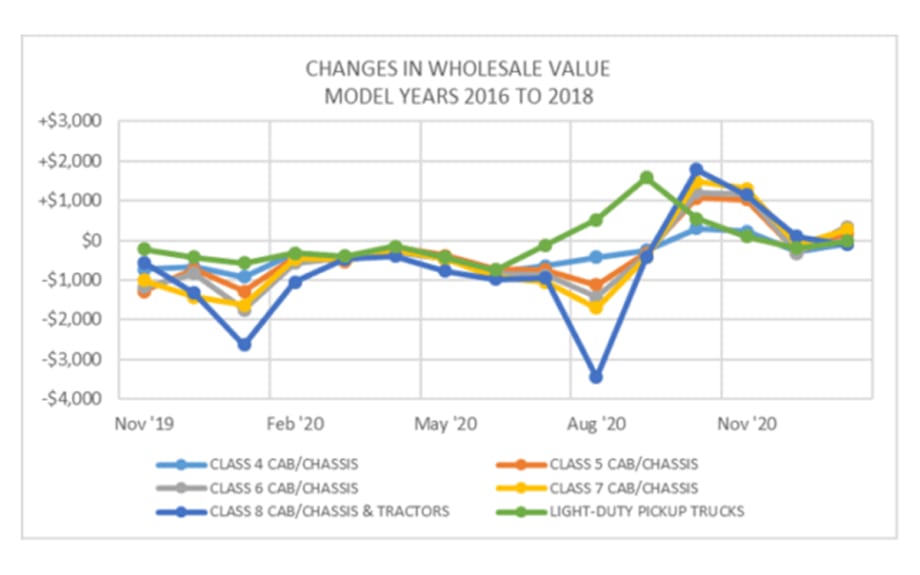

Medium and Heavy-Duty Trucks

Prices

Medium and Heavy-Duty truck wholesale values remain on a stabilization trend as we open the books to 2021. Production and supply chain issues mixed with increasing demand continue to be the driving forces behind the strength in the market. Now, we have a microchip shortage that is impacting new production to add to the growing storm. Overall, we are seeing fewer units showing up at auction, as the majority of trade-ins end up on retail lots. From November to December of 2020 we saw a 34% reduction in the number of 2019 – 2011 units being remarketed.

Remarketing efforts normally slow down a bit from December through mid-January; however, we are used to seeing about a 17% drop in remarketing during this period.

Taylor and Martin, Ritchie Brothers, Manheim, JM Wood, and ADESA all have multiple sales scheduled for Q1 of 2021, beginning the last week of January. Ritchie Brothers will hold its massive 6-day Orlando Sale, nicknamed the Super Bowl, as an online only event. This event normally pulls buyers from around the world. Last year’s Super Bowl totaled $237 million in sales, with over 18,000 online bidders registered from 85 countries. This year, it will be interesting to see if COVID-19 impacts demand and prices, as the pandemic has disrupted imports and exports around the world.

Heavy-Duty Trucks

Heavy-Duty Trucks continue to rebound following years of increased depreciation due to a saturation of production in the used market.

Average used truck mileage dropped 1,927 miles from Nov – Dec on 2015-2019 MY tractors. This speaks to the overall condition of units being remarketed.

We expect used equipment mileage to increase over the next several years as fleets for forced to keep trucks in service longer

Medium-Duty Trucks

Similar to Heavy-Duty Trucks, Medium-Duty Units continue to increase in demand and price as overall supply continues to help drive used truck pricing.

Box trucks larger than 16ft, flat-beds, and dump trucks remain in high demand due to their versatility.

Dump and straight trucks are in high demand due to construction and the housing market

Retail Sales

An overall lack of new and used supply continues to be a concern for this industry. Used retail sales remain strong with many models increasing in value as a result of the tight used supply. From November to December of this past year, used retail transactions were down considerably, which helped improve values. Retail prices increased as much as $1,675 on certain models. We expect to see continued strength in pricing as manufacturers needing trucks to deliver products to businesses and consumers across the country.

Below, new retail sales figures published by Wards Auto show a steady increase in retail sales from April to October. The pandemic continues to have a negative impact on new production which caused a dip in retail sales from October to November. Although vaccines are being shipped across the country, supply chain issues, and now microchip shortages, will continue to cause challenges as OEMs struggle to procure necessary parts. These issues could delay earlier projections that indicated production will meet demand in Q3 of this year.

Originally posted on Auto Dealer Today

More Showroom

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →

California Holds EV Lead Despite Annual Decline

At nearly 14%, California had the lowest zero-emission vehicle market share in the first quarter since the fourth quarter of 2021, according to the California New Car Dealers Association.

Read More →