BLACK BOOK: Weekly Market Update

It is now clear that like 2020, 2021 will also not have typical seasonality patterns as the market is going through a rapid increase in wholesale values.

It is now clear that 2021 will also not have typical seasonality patterns as the market is going through a rapid increase in wholesale values.

Wholesale Prices, Week Ending May 22nd

Wholesale values have risen for four months, with average weekly increases above 1.0% for the last eleven weeks. The rapidly rising values can be explained by basic supply & demand. Ongoing delays from part suppliers, most recently the global chip shortage, are causing significant shortages to new-vehicle supply which directly impacts the used-supply channels. Balance that against pent-up demand, stimulus, low interest rates, etc., and we have soaring wholesale values.

Car Segments

On a volume-weighted basis, the overall Car segment continued it’s 17-week trend, increasing this week by 1.17%.

Six of the nine car segments had gains exceeding +1%.

Compact Cars have had a higher growth rate than the overall car segment average for 10-consecutive weeks.

For the first time since mid-January, Prestige Luxury Car had a larger weekly increase than the car segment average.

Sporty Cars had the largest weekly gain (+1.61%), followed closely by Luxury Car (+1.49%).

Truck Segments

On a volume-weighted basis, the overall Truck segment increased 0.93% this past week. For reference, the previous weeks increase was1.12%.

All thirteen truck segments reported gains last week, with seven exceeding +1%.

Sub-compact Luxury Crossovers led the gains (+1.67%) this past week, followed closely by Sub-compact Crossovers (+1.54%) which have increased more than the car-segment average for 15-consecutive weeks.

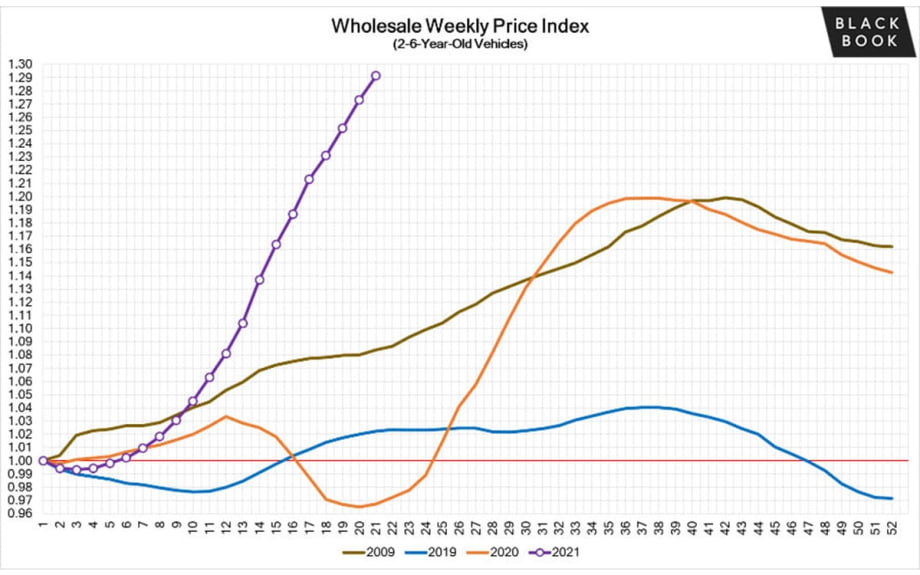

Newer Used Vehicles (0-2-year-old)

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. It is now clear that 2021 will also not have typical seasonality patterns as the market is going through a rapid increase in wholesale values. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Currently, wholesale prices are more than 29% higher compared to the beginning of the year (adjusted for the mix).

Retail (Used and New) Insights

Electrification is in the plans for a majority of OEMs with announcements coming out every few weeks about new models to come:

Ford revealed their electric Full-Size Pickup, the F-150 Lightning; the base model starts under $40,000 with 230 miles of range.

Preorders for Kia’s first all-electric EV6 open June 3rd. The EV6 has an estimated 300-mile range and can charge in 20 minutes.

Rivian is set to begin deliveries of its R1T electric pickup Launch Edition in June; the R1S SUV is expected to start in August.

The semiconductor chip shortage is expected to cost the global automotive industry $110 billion in revenue in 2021, according to consulting firm AlixPartners. The forecast is up by 81.5% from an initial forecast of $60.6 billion in late January.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. Currently, the prices are more than 15% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Volume

Used Retail

Current used retail listing volume is about 13% below the start of the year, but the inventory levels have slowly but consistently increased over the last 4 weeks, which indicates that dealers are able to procure inventory but an increase at this point in the year is not a trend seen in recent previous years, as can be seen on chart below.

Days-to-turn has been decreasing since the middle of March, which reflected an increase in retail demand across the country, but now, days-to-turn has started to stabilize.

Wholesale

Floor pricing continues to increase each week, but availability of average and clean units remains scarce which is leading to declining conversion rates in recent weeks.

Despite the limited inventory on dealer lots, many dealers are finding themselves receiving greater profit margins in the wholesale channel as opposed to their own retail lots.

Armed with the knowledge that their available inventory in the pipeline is extremely limited, remarketers are finding that they are able to continue to raise their floors and hold firm on their set values. They plan to accept a no-sale this week with the expectation it will sell the next.

More Showroom

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →

California Holds EV Lead Despite Annual Decline

At nearly 14%, California had the lowest zero-emission vehicle market share in the first quarter since the fourth quarter of 2021, according to the California New Car Dealers Association.

Read More →