Black Book: Weekly Market Update

The overall market continued to decline this past week, but the rate of depreciation lessened, and some segments reported positive pricing movement.

The overall market continued to decline this past week, but the rate of depreciation lessened, and some segments reported positive pricing movement.

BLACK BOOK – Wholesale Prices, Week Ending August 21st

The overall market continued to decline this past week, but the rate of depreciation lessened, and some segments reported positive pricing movement. Despite the lower level of depreciation this past week, the rate of weekly decline remains at a level that is larger than the overall market traditionally experiences this time of year.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.12% -0.58% -0.19%

Truck & SUV segments -0.48% -0.48% -0.21%

Market -0.36% -0.52% -0.21%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.12%. For reference, the previous week decreased by –0.58%.

Sub-Compact Car (-0.74%), Prestige Luxury Car (-0.55%), and Sporty Car (-0.90%) had the largest declines this past week. Sub-Compact Car had twenty-five weeks of gains, so it is no surprise that the past three weeks have had large declines. For comparison, the prior weeks’ change was -0.91%.

Six of the nine car segments reported stability with only small increases or decreases in wholesale values.

Truck / SUV Segments

The volume-weighted, overall Truck segment declined -0.48%, which is the same as the previous week’s decline of -0.48%.

All three van segments had gains again last week, with Minivan increasing +0.72%, Full-Size Van up +0.50%, and Compact Van moving by a smaller +0.18%.

Full-Size Pickups have seen increasing rates of depreciation in recent weeks, with the 1500 series trucks driving the declines due to new vehicle incentives still being available. 2500 and 3500 trucks remain in short supply, with lower incentives.

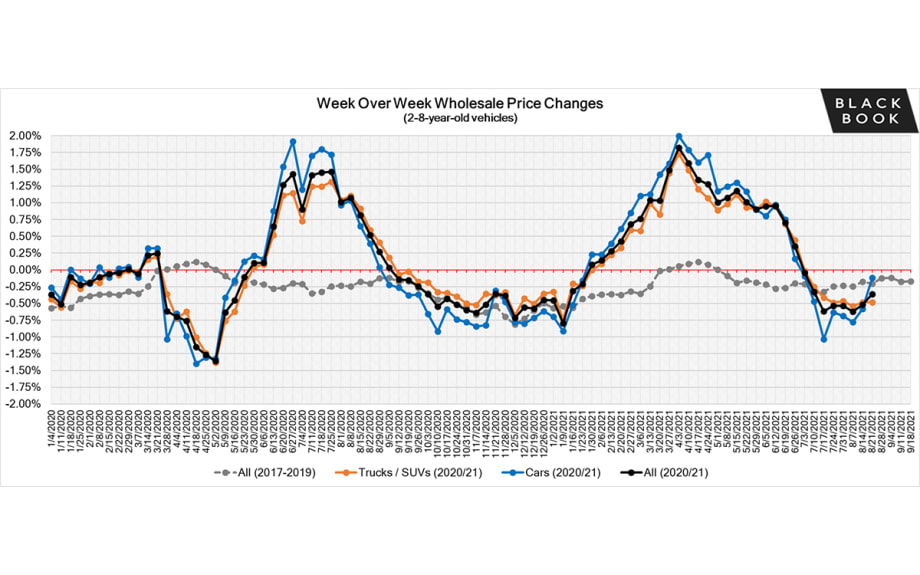

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices are now declining at rates higher than the typical seasonal decline.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

Up until now, Toyota has been unaffected by the microchip shortage, but they announced last week they will be making cuts to production because of the shortage. They are estimating this will cut their September global volume by 40%.

Ford also made headlines last week, with more planned plant closures, this time for the F-150.

General Motors has had production disruptions to most of their product line-up and the list of affected models continues to grow. The latest to fall victim to the microchip shortage are the Chevrolet Bolt EV and EUV. Additional downtime is also planned this week for some of their SUVs and sedans.

Genesis revealed their first electric crossover, the GV60. The compact crossover is set to go on sale in the US next year.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. In June, retail prices continued to rise. After strong Spring and Summer months, retail listing prices seemed to stabilize at a level more than 24% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Current used retail listing volume is about 13% below the start of the year. Used inventory is now starting to decrease again due to slow down in trade-ins and lease returns.

Days-to-turn for used retail listings have been increasing, as retail demand softened over the last few weeks. The days-to-turn now sits just below 33 days, which is still lower than what is typically expected in a normal year.

Wholesale

Sales rates have been continually improving in recent weeks as sellers have adjusted floors to reflect the softening in wholesale values.

The news of Toyota’s plans to cut 40% of their September production has dealers anticipating the demand for used vehicles will continue. New car dealers have already been reporting they are at historic lows of available new inventory.

The industry will come together in-person this week for the National Independent Automobile Dealers Association (NIADA) convention and the International Automotive Remarketing Alliance’s (IARA) Summer Roundtable in San Antonio, Texas.

More Showroom

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →

California Holds EV Lead Despite Annual Decline

At nearly 14%, California had the lowest zero-emission vehicle market share in the first quarter since the fourth quarter of 2021, according to the California New Car Dealers Association.

Read More →