Specialty Market Update

The biggest takeaway from this month’s value changes is that all the warm weather segments are down, most by substantial amounts. The only vehicles to see any upwards pricing pressure are the snowmobiles, which should be headed in that direction for the next several months, reports Black Book

The biggest takeaway from this month’s value changes is that all the warm weather segments are down, most by substantial amounts. The only vehicles to see any upwards pricing pressure are the snowmobiles, which should be headed in that direction for the next several months, reports Black Book

Motorcycle & Powersports Market Update

“Powersports values continue to show volatility from month to month as we seem to be heading back towards more normal seasonal adjustments in pricing. After last month’s surprising rise in values, we are currently seeing broad based declines for most segments that are more typical for the time of year. Once again, this comes with the caveat that demand and prices are significantly elevated from historical levels, and we are still quite a distance away from a “normal” market.” – Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

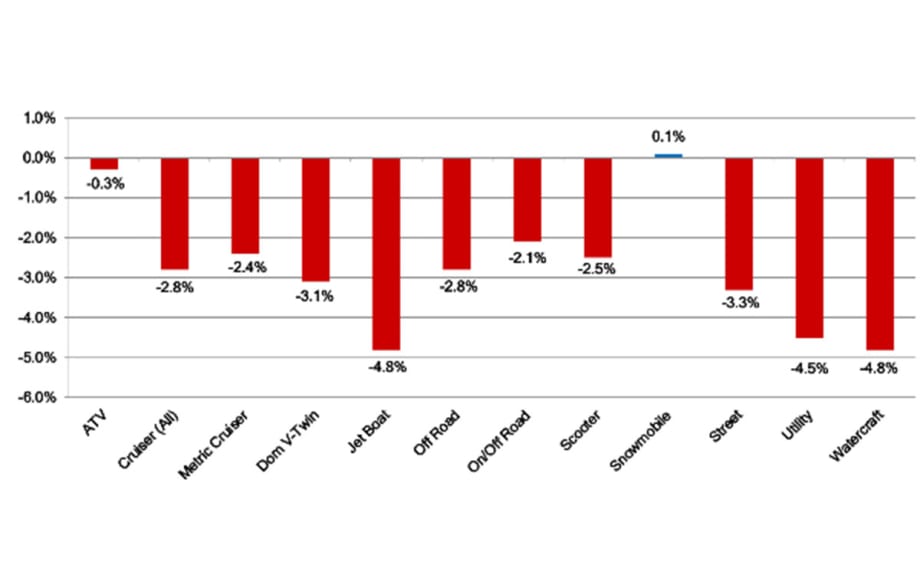

September to October Average Segment Change in Value

The biggest takeaway from this month’s value changes is that all the warm weather segments are down, most by substantial amounts. The only vehicles to see any upwards pricing pressure are the snowmobiles, which should be headed in that direction for the next several months. Last month’s rise in values for most segments appears to have been another mark of the volatility in the market as society continues to come to grips with all of the disruptions and changes brought about by thepandemic over the past 18 months. While the overall trends at the moment are for downwards adjustments in pricing nearly across the board, continuing high consumer demand and ongoing production issues due to both COVID and the computer chip shortage will act as a brake on this process. We expect overall pricing levels to remain high throughout the rest of this year and well into 2022 before coming back down to more “normal” levels.

Segment Spotlights & Industry News

Street Bike Performance

Street bikes have behaved much more typically this year than last. As you can see from the chart below, prices have been on a downwards trajectory since their peak earlier in the year. That being said, overall price levels are still substantially higher than historical averages.

ATV & Utility Vehicle Performance

The ATVs and Utility Vehicles, much like their on-road counterparts, are on a path back towards more normal value adjustment patterns. The ATVs, which have lagged the Utility Vehicles in overall appreciation this past year are faring slightly better at the moment.

In recent conversations with dealers they continue to report lessening but still healthy demand and ongoing issues with acquiring inventory. In particular, the chip shortage is now hampering deliveries of new units from many manufacturers. As a result, dealers have become more adept at selling new units before they arrive. One dealer reported they were currently taking four times as many deposits as they did pre-COVID. Additionally, many dealers are currently sitting on about 30 days inventory, versus a more typical 90 to 120 days supply prior to the pandemic.

The Powersports Finance Summit 2021 is being held Oct 26, at the Wynn in Las Vegas. Our Senior Analyst for Motorcycle & Powersports, Scott Yarbrough, will be a participant on the Vehicle Values panel. Please stop by and say hello if you are attending in person, or catch up on the event afterword at Auto Finance News. (autofincancenews.net)

Collectible Cars Market Update

“The end of summer is always a busy time as many enthusiasts try to squeeze in one more fun event before the weather starts to get colder and their attention turns to thinking about what’s going to happen in Scottsdale in January. This year was no exception, with a host of auctions being held all around the country. Results were strong across the board, and the collectible car world appears to be in excellent health heading into fall.” – Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

RM Sotheby’s St.Moritz auction, held at the famous Kempinski Hotel, was their first ever to be held in Switzerland, and was very successful, with sales totals reaching just under $18,000,000. As it was a high-end boutique sale, there were only twenty-four vehicles offered. Of those, only six failed to sell, resulting in a 75% sell through rate. Eight individual lots sold for in excess of $1,000,000.

RM Sotheby’s Auburn, Indiana auction, continuing a long standing tradition of being held on Labor Day weekend, marks the traditional end of summer and the beginning of fall in the collectible car world. It is always a fun and well attended event, with vehicles spread across price ranges that include the budgets of most collectors. This year, total sales came in at $15,800,000, and the sell through percentage was an astounding 97%. One of the crowd’s favorites was the 1936 White Model 706 Yellowstone National Park Tour Bus, which realized $550,000.

Mecum’s Dallas auction was a four day event that saw a broad selection of 1,101 collector vehicles cross the block. 946 of them were declared sold, for a healthy sell through rate of 86%. Total sales came in at $36,800,000.

Barrett-Jackson’s first ever sale in Texas was held in Houston at the NRG Center. As a “no reserve” auction the sell through was 100%, with total sales coming in at $37,500,000 on the sale of roughly 500 vehicles. This was their most successful auction not held at their Scottsdale, Arizona headquarters, and 34 new world records were set.

Notable Recent Auction Sales Include:

1958 BMW 507 Roadster $2,300,000 (RM Sotheby’s)

1988 Porsche 959 Komfort Coupe $2,121,000 (RM Sotheby’s)

2012 Aston Martin One-77 Coupe $1,850,000 (RM Sotheby’s)

1955 Mercedes-Benz 300SL Gullwing $1,486,000 (RM Sotheby’s)

2019 Lamborghini Aventador SVJ Coupe $660,000 (Mecum)

1970 Ford Mustang Boss 429 Fastback $357,500 (Mecum)

1957 Cadillac Eldorado Biarritz Conv $220,000 (Mecum)

1979 Porsche 928 Coupe “Risky Business” $1,980,000 (Barrett-Jackson)

2019 Ford GT Coupe Lightweight $1,199,000 (Barrett-Jackson)

1966 Shelby GT350 “Stirling Moss Race Driven” $495,000 (Barrett-Jackson)

1958 BMW 507 Roadster Courtesy of RM Sotheby’s

Market Trends

The Vintage Exotic segment focuses on high dollar European exotic sports cars produced from the late 1950s up through the mid-1970s. This is without a doubt the top of the market. This segment includes Ferrari 250s, 275s, and 365s, Lamborghini Miuras, Maserati Ghiblis, Mercedes-Benz Gullwings, Porsche Speedsters, and coach-built Bentleys and Rolls-Royces. Although most owners of these vehicles are wealthy individuals, the market is very volatile and fluctuates quite a bit as it falls in and out of favor, sometimes being seen as a safe haven in which to park money and other times as an unreasonable extravagance. Values have been fairly stable for several years, with some individual models generating more interest than others.

Slightly more than half of the vehicle segments we track increased in value last year, including Muscle Cars, Pony Cars, Vintage Exotic Cars, and Classic Trucks/SUVs, while a couple, American Classics and Vintage European Sports Cars, declined. As we are coming out of COVID and things have been getting back to normal (hopefully) there has been a lot of pent-up consumer demand, especially for the “fun vehicle” categories, including Boats, Motorcycles/Powersports, RVs, and of course collectible cars and light trucks. We are starting to see signs of life with the two segments which went down last year, although American Classics are still burdened with an aging collector base, and Sports Cars had skyrocketed a few years ago, so they may still be finding their equilibrium.

Recreational Vehicles Market Update

“For the first time in several months, one of the RV market segments has declined in value: motorhomes dropped seven percent, falling for the first time since February, and while towables once again increased, it was by under one percent, their smallest gain since last November. Is increased new production helping supply finally catch up with demand, or is this just normal market fluctuation?” – Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Cooling Off As Fall Approaches

For Motorhomes (including Class A, B, and C)

Average selling price was $69,953, down $5,536 (7.3%) from the previous month.

One year ago, the average selling price was $56,259.

Auction volume was down 19.1% from the previous month.

The average model year was 2009.

For Towables (including Travel Trailers and Fifth Wheels)

Average selling price was $24,280, up $140 (1.0%) from the previous month.

One year ago, the average selling price was $18,280.

Auction volume was up 5.3% from the previous month.

The average model year was 2016.

Industry Highlights

According to the RVIA, the total number of RVs shipped in August reached 52,819, the highest amount ever for the month, and an increase of 33.8% over August 2020. Towables totaled 47,889 units and motorhomes accounted for 4,930. Truck Campers came in at 464, Folding Camping Trailers reached 575, and Park Models were 309. August was the second highest month ever for RV shipments, trailing only March 2021. Class B motorhomes extended their gains to 16 consecutive months, with 1,442 shipped.

The Hershey RV Show, presented by the Pennsylvania Recreation Vehicle and Camping Assn, was very successful, with announced attendance of 61,320, their second best year ever. Several manufacturers reported strong sales, with many setting records.

Camping World presented a plan to financial analysts to grow their annual revenue to $1 billion on an EBITDA basis.

The annual “Elkhart Open House”, where RV dealers gather to view new RV models and place their orders for next year, was canceled for the second year in a row. Some dealers still came in person to view the offerings and meet with manufacturers in smaller venues.

Thor Industries announced they just had their most profitable year ever, with net sales of $12 billion.

Statistical Surveys, Inc. reported that there were 53,985 retail RV registrations in July, down 25% year over year.

Medium and Heavy-Duty Truck & Commercial Trailer Market Update

“We are seeing an increase in demand for new and used Medium and Heavy-Duty units, as well as Commercial Trailers following the leveling off that occurred in August. Sticker shock and price fatigue helped ease retail demand for a few weeks, while pent up demand and low inventory allowed the market to remain stable. Over the past month, we’ve seen demand increase with transaction prices and conversion rates improving. Further complications within the supply chain have forced many to extend their previous expectations for when production will meet demand. With over 19 months of below normal new model production for classes 3 – 8 and commercial trailers, we do not expect supply to catch up with demand until after the first quarter of 2024. Used prices will continue to increase through Q2 of next year before reaching a soft ceiling that is expected to last the remainder of the year. We expect to see softening in used pricing beginning as early as the second quarter of 2023 for commercial trucks and trailers." – Josh Giles, Principal Automotive Analyst, Valuations & Residuals

Heavy-Duty Trucks and Tractors

The chart above shows the monthly adjustment trends for each segment within the Heavy-Duty market.

Heavy-Duty Over-the-Road (OTR) values increased 4.4% from September to October, compared to the 0.3% increase seen the prior month.

Heavy-Duty Regional Tractor (HR) values increased 4.5% from September to October, compared to the 0.4% increase seen the prior month.

Heavy-Duty Construction (HC) vales increased 9.0% from September to October, compared to the 0.5% increase seen the prior month.

Medium-Duty Trucks

The chart above illustrates the monthly adjustment trend for Medium Duty trucks.

Production delays mixed with increasing demand on last mile deliveries continue to help improve values for units in this segment.

From September to October, Medium Duty Trucks have increased an overall weighted average of 2.8% compared to the 1.5% increase seen from August to September.

So far this year Medium Duty values have increased 24.1%. This is amazing considering MD units depreciated 11.6% during the same period in 2020.

According to the Federal Reserve Economic Data (FRED), new retail sales grew only 1% from July to August. New retail sales figures of August were reported at 36,308 units. This number is close to the figure reported this time last year at 36,327 units; however, we are down 22% from the figures reported in August of 2019.

ATA Truck Tonnage continues a downward trend, reporting a drop of -0.8% from June to July. It’s important to point out though, that these numbers are extremely positive considering the pandemic, supply chain issues, and driver/operator shortages.

Reports are indicating that driver interest is down due to the reduced number of driver applicants and graduates coming out of school. There is also a lack of drivers returning to work due to strong unemployment benefits. Interest will likely increase as time goes on and unemployment benefits are reduced.

With backed-up freight and the Holiday Season just around the corner, we expect to see a continued slow recovery as far as production and transportation go, with continued strengthening of used vehicle prices.

Commercial Trailer Market Update

Commercial Trailer values continue to increase as new production issues are causing scarcity in both new and used inventory.

Wholesale and retail transactions on all trailer segments continue a positive trend as demand continues to rise.

In addition to transportation, some trailers are used as storage. With freight being backed up due to equipment availability or driver shortages, Dry Vans, Refrigerated Vans, and Lowbed trailer demand has surpassed the rest of the pack.

Dry Van values have increased 17.8% for October, compared to the 18.1% increase from Q3.

Dump Trailers were flat this past quarter, showing only a 0.6% increase for Q3.

Refrigerator Vans have gained 14% for October, compared to the 2.8% increase seen during Q3.

Following a slight drop in Q3, we increased Lowbed Trailers 6.6% heading into Q4.

We expect values for all trailer segments to continue increasing as new and used equipment becomes more scarce.

More Showroom

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →

California Holds EV Lead Despite Annual Decline

At nearly 14%, California had the lowest zero-emission vehicle market share in the first quarter since the fourth quarter of 2021, according to the California New Car Dealers Association.

Read More →