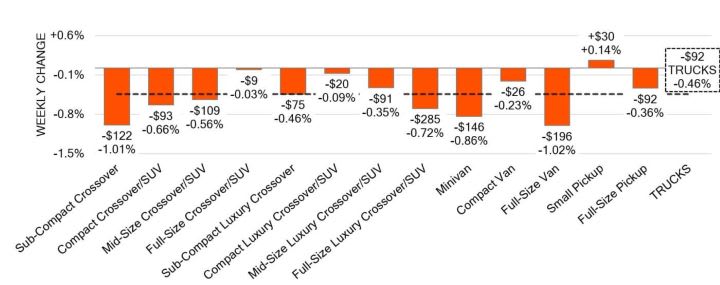

Small pickup trucks are defying a fourth-quarter seasonal trend of declining prices, as those 8 years old and newer saw an uptick last week. Black Book explains that and more in its weekly market report.

Most wholesale segments experienced a normal autumn depreciation as the year starts to wind down.

Black Book

Small pickup trucks are defying a fourth-quarter seasonal trend of declining prices, as those 8 years old and newer saw an uptick last week. Black Book explains that and more in its weekly market report.

Hybrids in particular lead not only EV market share but all power trains on the continent so far this year as gas and diesel continue their decline.

Read More →

Building on a previously announced $26 billion U.S. investment, Hyundai said it will grow its North American lineup and U.S.-based production and parts sourcing.

Read More →

Sony-Honda venture cancels two planned models, the first of which had been pegged for a mid-2026 California delivery debut. The brand’s direct sales had been challenged by the state’s auto dealers, but the venture cites Honda’s EV retreat.

Read More →

Softening prices, rising credit availability and higher tax refunds could be behind February’s sales pace rise and accompanying dip in inventory, according to Cox Automotive.

Read More →

The wholesale automotive market fared remarkably well given the U.S.-Israel war on Iran, Black Book analysts reported.

Read More →

The agency sent warning letters to dozens of auto groups about what it described as illegal practices and urged them to ensure their pricing policies enable transparency with consumers.

Read More →

New-vehicle sales fell year-over-year for the fifth month in a row in February, making retail deliveries the slowest they’ve been since 2023, according to a CarGurus report.

Read More →

The automaker says its California skunk works is already finding efficiencies to lighten traditionally heavy electric vehicles for lower cost, plus extended range.

Read More →

Both vehicle values and conversion rates sped up last week as two segments outperformed in the pre-spring burst of buying.

Read More →

GM says it sells the cheapest electric vehicle in the U.S. market. It explains how it made improvements to the entry-level EV while keeping its price down.

Read More →