Calculated Risk

Like previous quarters, the third quarter saw finance sources continuing to delve deeper into the credit spectrum. But is this good for the industry?

Automotive loan portfolios continued their strong performance in the third quarter 2012. Overall loan balances grew, delinquencies remained below prerecession levels and finance sources responded by making it easier for consumers to obtain a vehicle loan.

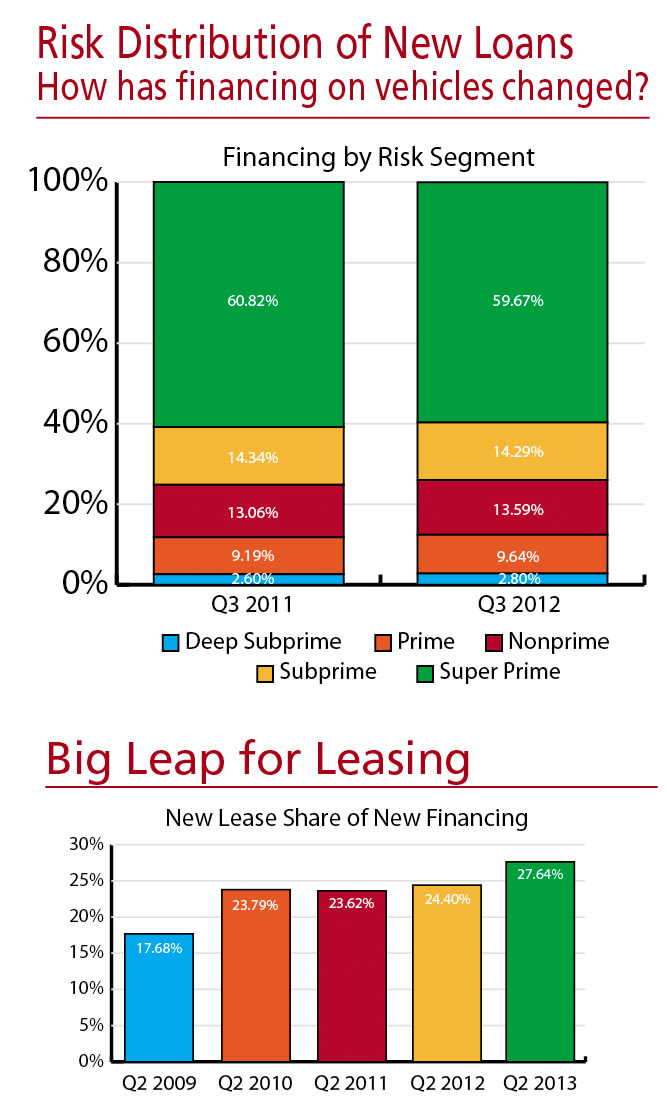

Experian Automotive’s third-quarter data showed more positive signs: Credit scores fell to prerecession levels, and finance sources increased their average amount financed. They also continued to welcome car buyers with below-prime credit. But the biggest indicator of the auto finance market’s health was the 7.53 percent year-over-year uptick in new-vehicle leasing

These trends are positive signs for dealers as the New Year progresses, putting consumers who are returning to the market in a better position to make a vehicle purchase. But as stated in previous reports, lenders continue to proceed with some caution. That measured approach is key to the auto finance market sustaining its drive toward recovery.

Delinquencies Fuel Lender Appetite

For the second consecutive year, third-quarter 30- and 60-day delinquencies remained below the rates recorded in the third quarter 2007. For 30-day delinquencies, the rate fell from 2.78 percent in the year-ago period to 2.67 percent. The rate logged during the same quarter in 2007 was 2.81 percent.

The 60-day delinquency rate also fell, from 0.71 percent in the third quarter 2011 to 0.69 percent in the third quarter 2012. During the same period in 2007, the rate stood at 0.74 percent.

Car buyers in Alaska and North Dakota are leading the nation in making their payments on time. In Alaska, the 60-day delinquency rate stood at 0.35 percent in the third quarter, while North Dakota recorded a 30-day delinquency rate of 1.39 percent.

On the opposite end of the spectrum, consumers in Mississippi had the highest percentage of delinquent 30- and 60-day loans, which stood at 4.38 and 1.33 percent, respectively, in the third quarter.

Percentage of Dollars at Risk Drops

Another indicator of the auto loan market’s health is the overall percentage of total dollars at risk. In the third quarter, the proportion of dollars at risk in lenders’ portfolios dropped, giving them more flexibility in terms of their lending strategy.

Third-quarter data revealed that 30-day delinquencies totaled $14 billion, or 2.16 percent of the total loan portfolio. For the same period in 2011, 30-day delinquencies represented 2.29 percent of the total loan portfolio.

Sixty-day delinquencies totaled $3.3 billion, or 0.5 percent of the total loan portfolio. For the same period in 2011, 60-day delinquencies represented 0.53 percent of the total loan portfolio.

The report also showed that total loan balances grew by $37 billion, rising from $642 billion in the year-ago period to $679 billion in the third quarter 2012.

Lenders Buy Deeper

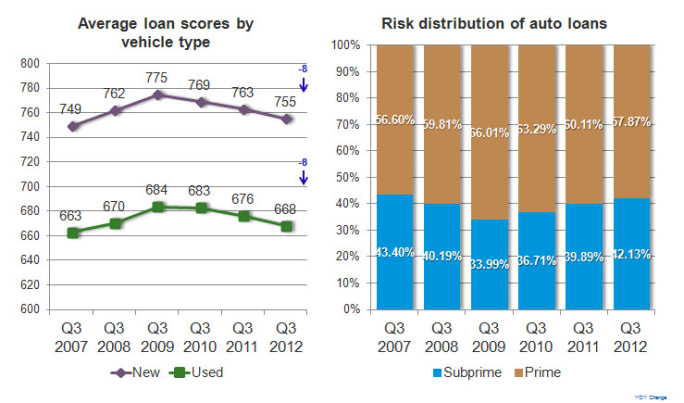

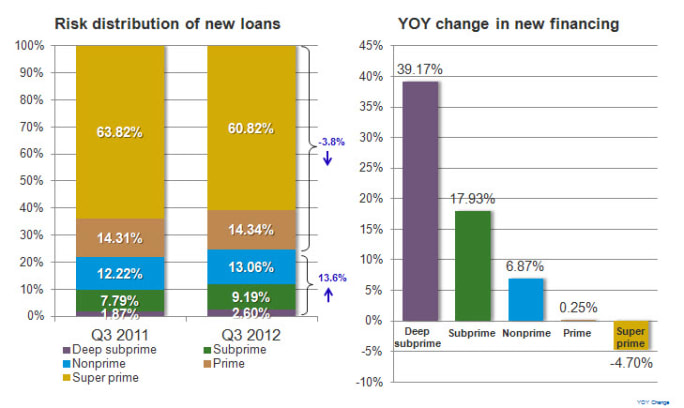

With more consumers continuing to make their loan payments on time, finance sources continued to ease their way into the more risky credit tiers. According to third-quarter data, 24.84 percent of all new-vehicle loans went to customers with nonprime, subprime or deep-subprime credit.

Nonprime grew from a 12.22 percent market share in the third quarter 2011 to 13.06 percent in the third quarter 2012. Subprime share grew from 7.79 percent to 9.19 percent, while deep subprime’s market share grew from 1.87 percent to 2.6 percent.

Average Credit Scores Fall

With below-prime loan originations growing, the average credit score for new- and used-vehicle loans dropped. For the third quarter, average consumer credit scores for new-vehicle loans fell by eight points from 763 in the third quarter 2011 to 755. Average consumer credit scores for used-vehicle loans also fell, from 676 in the year-ago period to 668.

Despite the drop in scores, lenders remained more risk-averse than they were before the collapse of the credit markets. In the third quarter 2007, the average credit score for a new-vehicle loan was 749.

Taking Measured Risks

As industry metrics continue to fall or rise to prerecession levels, we must ask the obvious question: Is that a good thing? After all, the last time subprime financing boomed and average credit scores dropped, the nation experienced one of the worst financial collapses in its history.

Based on 2012 data, however, lenders seem to be proceeding with caution rather than the irrational exuberance that led to the credit crisis. Delinquencies remain low and dollars at risk have dropped, and the risks lenders are taking seem to be well-calculated. And as long as they maintain that approach, they’ll be able to continue delving deeper into the credit spectrum. Of course, that means consumers have to do their part by making timely payments.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →