Lease-Here, Profit Here

Dealers have found increased cash flow and profitability after moving from a new-car or BHPH/RTO model to lease-here, pay-here. Leasing expert breaks down the advantages of LHPH and discusses the potential risks.

What is lease-here, pay-here? Essentially, it’s an alternative to the buy-here, pay-here and rent-to-own models. However, there are several major differences and a number of advantages — and some disadvantages — for dealers.

LHPH has often been dismissed as too complex for dealers who are accustomed to new-car sales or BHPH. Before you decide whether or not LHPH will work for you and your dealership, let’s break down the basics of such a program and discuss the potential benefits and inherent risks.

Lease-here, pay-here advantages

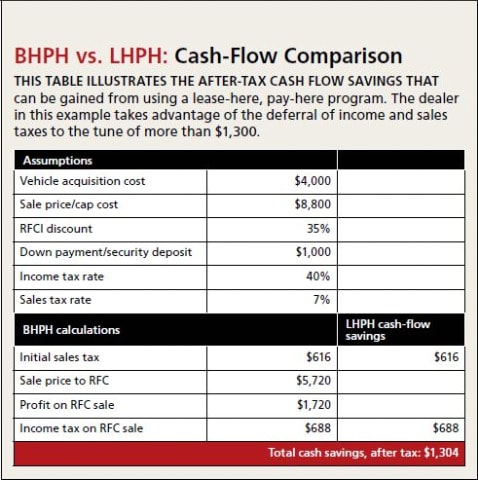

The biggest attraction to LHPH is the elimination of the upfront sales tax. While the accounting, regulatory and federal taxation differences between LHPH and BHPH programs are identical in all states, there are sales tax and licensing differences dependent upon state rules. Understanding the leasing sales tax rules in your jurisdiction is the first step.

LHPH also can increase profitability. If you’re collecting the same payment amount for the same term amortizing only to residual value, the result is a much higher rate and rental income. When added to the tax savings previously discussed and profits generated from trade-ins, you have the potential for a more profitable business that is easier to sustain through weak demand periods.

That being said, here are the four primary advantages that LHPH holds over BHPH:

1. Elimination of initial sales tax: In all but 17 states, a LHPH transaction is not subject to the initial sales tax that would be applied to a BHPH transaction. The buyer’s initial cash payment can be retained as a security deposit rather than being paid to the state. For dealers, that means increased cash flow, greater liquidity and reduced borrowing costs.

2. Deferred federal and state income tax liabilities: In a BHPH conditional sale, there is a significant “gain on sale” when the vehicle is sold for an amount that is (typically) 50 to 100 percent greater than the dealer’s tax basis in the vehicle. To reduce the federal and state tax liabilities assessed on this gain, the retail installment sales contract is typically sold to a related finance company (RFC) at a discount. However, there is still upfront net profit that’s subject to federal and state taxation. With LHPH, there is no gain on the sale, because there is no sale! That eliminates the need to move the lease to an RFC in order to book a separate “loss on the sale of the lease.” Since the leased vehicle can be depreciated on an accelerated basis, the transaction starts with a tax loss from the accelerated depreciation, in effect, creating a tax shelter for the dealership.

3. Reduced federal and state regulatory requirements: Experienced BHPH dealers know that compliance is never a sure thing. Regulation Z and the various state regulations impose a highly technical set of requirements. Attorneys are quick to jump on minor technical errors and the courts and regulatory agencies continue to evolve new interpretations of these requirements. On the other hand, LHPH transactions are guided by the much less-onerous Regulation M. Only a handful of states (most notably, California and New York) have state consumer leasing acts that impose added requirements. With no “lease rate” disclosure required (or permitted), not only is customer resistance to the lease rate avoided, there are no usury limits or calculation idiosyncrasies to worry about.

4. Collection of tax-free security deposits: Leasing traditionally includes collection of a refundable security deposit at lease inception instead of a down payment. Unlike a down payment, a security deposit is not taxable, and is retained throughout the transaction as an offset against default liability. It’s also collectible at any point in the lease.

In addition to the primary benefits listed above, other benefits to LHPH include reduced consumer disclosures, bankruptcy protection, reduced monthly payments, and, in most states, no loss of prepaid sales tax in case of default.

What Are the Risks?

As with any other tool, there are also some disadvantages to implementing a lease-here, pay-here program. Here are the five primary risks inherent to LHPH:

1. Vicarious liability exposure: In some states, lessors have been held responsible for injuries caused by negligent lessees simply because the lessor owned the leased vehicle. Federal law has now virtually eliminated this risk, but lessors should still obtain contingent and excess liability insurance coverage to defend against nuisance suits.

2. Lease accounting and data processing complexity: LHPH programs cannot be accounted for and managed properly on BHPH accounting and data processing systems. A specialized system is required. However, LHPH programs can be structured similarly to BHPH programs with payments in arrears and use of the “interest rate implicit in the lease” to calculate payments.

3. New terminology and “true lease” compliance: Leasing has its own terminology, legal requirements and customer rights and duties. The BHPH sales and finance terminology your staff is accustomed to can confuse customers and potentially violate federal and state lease advertising rules and regulations. Such language may also inadvertently create a conditional sale with the related disclosure requirements.

4. General unfamiliarity with leasing: Even with compliance training, an internal program handbook and customer outreach, it is likely that staff will make mistakes in trying to answer customers’ questions about leasing. The ongoing training and supervision of your staff must include continued development of accurate answers to frequently asked questions from both sides of the transaction.

5. Third-party sale/funding limitations: Some BHPH dealers sell their loan portfolios to third-party finance companies. Others operate on lines of credit with lenders who are familiar with the program. A change to LHPH may limit the salability of your assets or require increased due diligence from the purchaser, especially considering the risk to residual value.

Lease-here, pay-here does have complexities and potential liabilities that you won’t find in buy-here, pay-here, and there is no cookie-cutter solution to turn a BHPH program into an LHPH overnight. It will take careful planning and you will incur some initial expense. However, investing the time and effort to understand the operational and compliance differences can pay huge dividends in profitability.

More F&I

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

What Market Timing Mistakes Mean for Your Reinsurance Program

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →

Your Office Is Talking

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

Read More →

F&I Training Fundamentals

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Read More →