The Perfect Blend

The ‘Father of the F&I Menu’ offers his thoughts on how many and what type of products should be on your store’s menu.

F&I managers are supposed to sell products, right? I mean, outside of all of the other duties they’re responsible for, F&I producers are expected to sell products and make additional profit for the dealership. That’s certainly the criteria by which their performance is judged, and it’s most assuredly what controls their paycheck.

One of the questions I get from F&I managers, general managers and dealers is: “Which products should we be selling?” They also want my advice on how many products they should offer.

My answer, which is based on 19 years of studying the top F&I departments in the country, is what you sell is less important than how many products you present. And when you examine the products that drive performance, you’ll find that there is no secret formula.

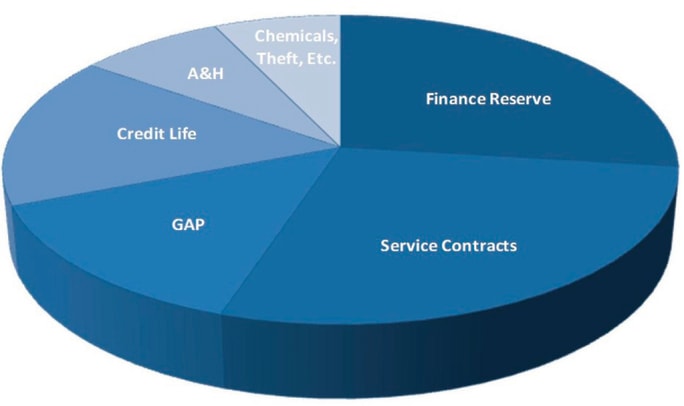

What you do find, however, is that top F&I performers drive high acceptance rates on four or five different products. And that’s what the pie chart accompanying this article illustrates.

A Tale of Two Dealers

The graph is based on a representative sampling from Dealer 20 Groups in 2012. Because of contractual reasons, I can’t offer any numbers or percentages, but the graph should give you an idea of how top-performing F&I departments distribute income across multiple products.

One additional note, the graph includes dealers that sell credit insurance. But I can tell you that the percentage breakdown would be identical for 20 Groups in states like California and New York, where credit insurance isn’t offered. Dealers in those states simply substitute credit insurance with other products to achieve this balance. And as you’ll see, these top-performing dealers sell a balanced variety of product, with finance reserve generally accounting for 30 percent of total income.

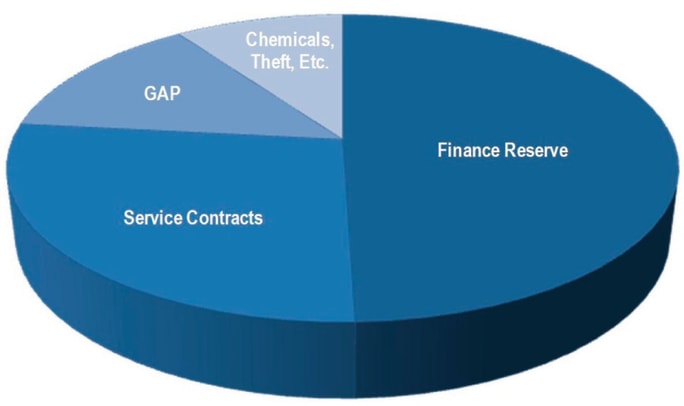

I’ve also included a second graph with this article to illustrate how below-average performers tend to rely on reserve, service contracts and a little GAP as their primary sources of income. But don’t be fooled by the larger pie pieces for this group. Penetration rates for top-performing F&I departments aren’t any less for those products. In fact, their rates match those lower performing stores; they just spread out their success over more products.

This graph illustrates how below-average F&I departments tend too rely on reserve, service contracts and GAP as their primary sources of income.

So, naturally, top performers make more money. And the disparity in performance has looked that way for the last two decades, at least according to our measurements. As a matter of fact, these charts are what drove my firm to focus on developing those early F&I menus, simply because it seemed to be the common denominator between the two groups.

Spread the Wealth

Achieving top-performer penetration rates comes down to a few basic principles: First, you need at least four or five products to sell. That may sound simple, but the fact is that many F&I managers don’t have enough products to sell. And if they do, they don’t present them in any meaningful way.

That’s why I say you have to view all products equally. Each product represents key income potential.

The truth is there are many F&I managers out there who only focus on finance reserve, service contracts and GAP. They simply don’t care about selling anything else. Many times this is the result of pay plans that overemphasize service contracts at the expense of other products.

The third principle is having a process that automatically and effectively presents all of the products for which the customer qualifies. And that’s why constant training, analysis and process evaluation are important, because overreliance on one or two products and finance reserve can happen with any process if those three items aren’t checked off your list.

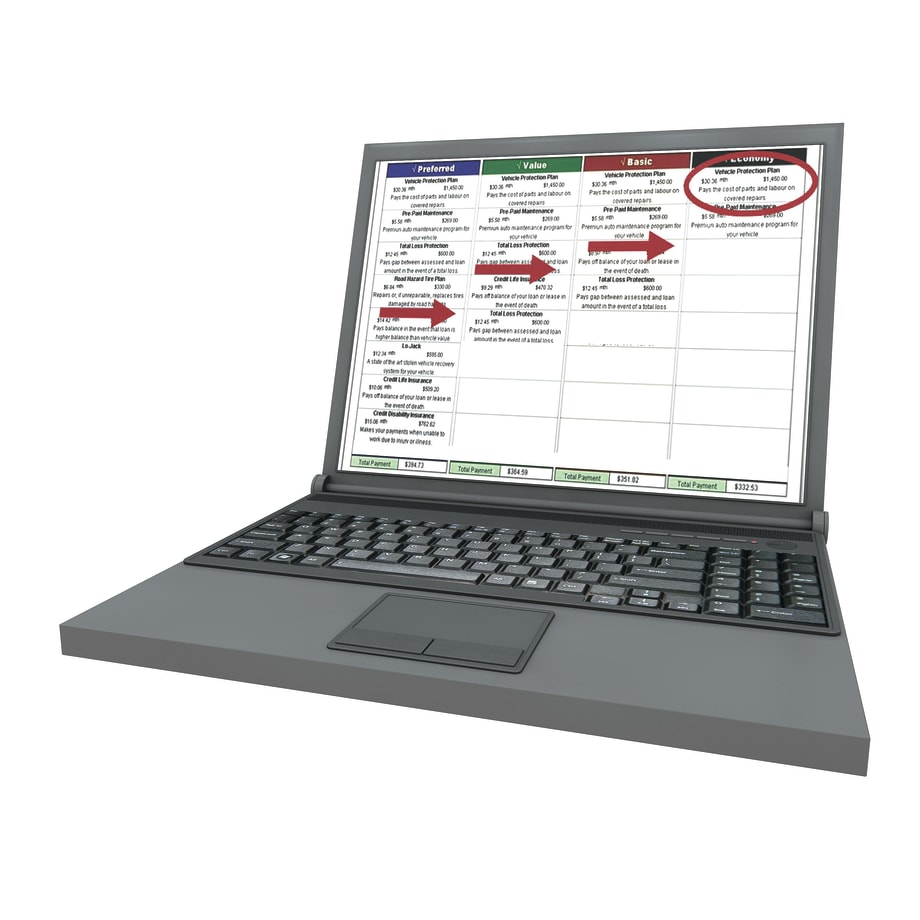

For example, when my firm rolled out the menu concept to the industry in the early ’90s, we developed and tested a lot of different styles and approaches. One of them was the four-column menu found in many F&I offices today. While it was a vast improvement over what most F&I offices were doing back then, we observed customers’ eyes instinctively and almost immediately drifting to the furthest box to the right. And that column typically contained a service contract and maybe one other product.

If you’re still using a four-column menu today, you know what typically happens next. The customer drifts toward that last column, and the F&I manager follows the customer’s lead. The F&I manager is then forced to skim over the first three columns before landing on the fourth to make sure he or she has enough time to present the service contract.

This pie chart represents how top-performing F&I offices sell a balanced variety of product, with finance reserve generally accounting for 30 percent of total income.

The effect of the scenario I described is that these F&I managers using these four-column menus were only offering service contracts and maybe one other product. Theoretically, all products were presented, but not effectively. And as we all know, customers won’t buy a product if it’s not presented, which probably explains why low-performing F&I offices rely so heavily on finance reserve to meet their income-per-unit averages.

Time Trials

Time is another issue in the scenario I previously described. Those of us who were working the box from the ’70s through the ’90s were taught to give a comprehensive list of features and benefits about our products. Problem was, our presentations became too time-consuming, and consumers became more sales-resistant and impatient with our long-winded sales pitches. We responded by limiting the number of products presented, which triggered another issue.

See, F&I managers began trying to qualify which products the customer was most likely to buy, then offer only those products. Unfortunately, all that did was further limit what products were presented. And that’s why my firm moved away from the traditional upsell philosophy to the approach we teach today, which is to present every product equally.

I’ll admit that our approach required extensive field research to perfect. And what we came up with were simple explanations for each product, coupled with easy-to-understand packages. We also made sure not to isolate any product and let customers direct the process by selecting their own coverage length, finance terms or limited insurance as payment-reducing options.

So, the key to achieving top income-per-unit averages and product penetrations is to present all the products, then allow the customer’s responses and preferences to “peel off” products to find the maximum payment to which the customer will agree.

The result of this approach is a customer-friendly process that leads to higher customer satisfaction scores, lower chargebacks, reduced time spent in F&I, and, of course, top F&I income. As for what products you should present, my advice is to present every product they qualify for every time.

George Angus is the training director for Team One Research and Training, a company specializing in scientific, research-based program development and training. E-mail him at george.angus@bobit.com.

More F&I

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →