NY Fed: Household Debt Surpasses 2008 Peak in Q1

The feat comes almost nine years after the Great Recession, when household debt reached $12.68 trillion. But the debt and its borrowers look quite different today, the New York Fed noted, and auto finance sources showed signs of tightening in response to some deterioration in auto loan performance.

NEW YORK – Total household debt in the first quarter finally surpassed its $12.68 trillion peak reached during the 2008 Great Recession, the Federal Reserve Bank of New York reported this week. And it happened during a period that saw a notable uptick in credit card debt transitioning into delinquencies, and a continued upward trend of auto loans transitioning into serious delinquencies.

Student loan transitions into serous delinquencies remained high, the New York Fed noted.

As of March 31, household debt reached $12.73 trillion, a $149 billion increase from the fourth quarter of 2016 and the 11 consecutive quarterly increase. And according to the New York Fed’s quarterly report, overall household debt is now 14.1% above the second quarter 2013’s trough.

“Almost nine years later, household debt has finally exceeded its 2008 peak, but the debt and its borrowers look quite different today,” said Donghoon Lee, research officer for the New York Fed. “The record debt level is neither a reason to celebrate nor a cause for alarm. But it does provide an opportune moment to consider debt performance.”

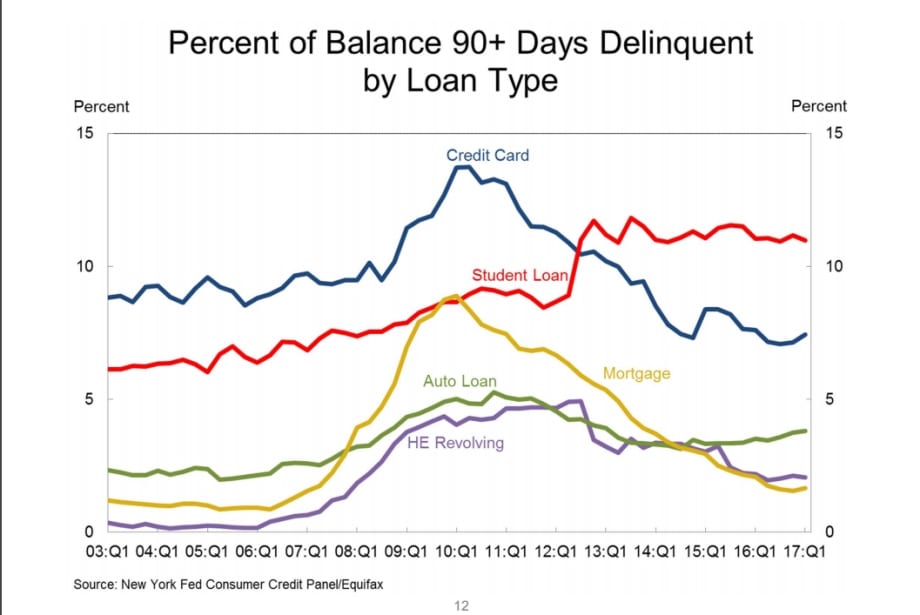

Aggregate delinquency rates were roughly flat in the first quarter, with some variations across product types. And as of March 31, 4.8% of outstanding debt was in some stage of delinquency. Of the $615 billion of debt that was delinquent, $426 billion was labeled seriously delinquent (at least 90 days late).

Auto loan balances increased by $10 billion during the quarter. Auto loan delinquencies were flat, with 3.8% of auto loan balances 90 or more days delinquent on March 31. But auto finance sources responded to the slight deterioration in auto loan performance.

Auto loan originations totaled $132 billion during the period, a decline from the prior quarter but a but an uptick from the same period last year. However, the period saw a tightening in underwriting guidelines, with the median score for originating auto loan borrowers ticking up to 706.

Looking at credit scores for both auto loan and mortgage originations, the New York Fed noted that origination volumes to borrowers with credit scores under 660 shrank since the same quarter last year, while origination volumes with credit score above 720 have increased considerably.

“While most delinquency flows have improved markedly since the Great Recession and remain low overall, there are divergent trends among debt types,” Lee noted. “Auto loan and credit card delinquency flows are now trending upwards, and those for student loans remain stubbornly high, hovering around 10% at an annual rate over the past five years.”

In an accompanying blog co-written by Lee, the New York Fed noted household debt picture is vastly different than in 2008. Mortgages now have a much smaller share than in 2008, while auto and student loans have increased in their share.

“Balances are increasingly shifting toward more creditworthy and older borrowers,” the blog reads, in part. “These shifts in borrowing patters and characteristics of borrowers, paired with the long economic recovery and a strong labor market, have resulted in very low delinquency rates for most types of debts except for student loans.

“More recently, performance on mortgages have continued to improve, while auto loan delinquency flows have been trending upward since 2012,” the blog continues. “Credti card transitions have also ticked up. The standout, however, has been student loans — with new serious delinquency flows that deteriorated steadily between 2004 and 2014 and have remained stubbornly high since.”

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →