F&I trainer makes the case for digital F&I. He offers a five-step process for adding information about products, pricing, and your finance team to your dealership’s website.

Virtually every shopping experience now begins on the internet, whether we’re looking for a TV on Amazon, or a Mexican restaurant within walking distance. It’s one of the reasons consumers are now pushing for that same quick, easy and transparent experience when purchasing a vehicle. This paradigm shift means that, just like your new- and used-vehicle inventory, F&I needs to step online to engage and educate consumers about the process and the producers who drive it.

Your dealership needs a strategy that encourages F&I to collaborate with customers as they educate themselves about the vehicles they’re interested in, the financing they’ll need, and the F&I products that will protect their investment. And all of that needs to happen before they come to the dealership. In other words, we need to make the F&I department available where customers are most comfortable making buying decisions — on their laptops, iPads, or smartphones. The following are five items you need to include in your F&I department’s new online strategy:

Ad Loading...

1. List Your Finance Sources

Most franchised dealers have numerous finance sources to choose from, including subprime finance companies, banks, and captive finance sources. Most customers, on the other hand, probably only work with one financial institution. Many dealers also work with a network of credit unions, such as CU Direct Lending, meaning they have scores of credit unions available. As LendingTree likes to say, when lenders compete, customers win.

Tech vendors aren’t the only ones pushing dealers to establish an online presence for their F&I departments. Regulators like the Federal Trade Commission are also making a strong case for connecting F&I to buyers early in the shopping process. On July 8, the FTC published four 60-minute videos designed to help buyers ‘shop with confidence.’

What we need to do is explain to customer the reasons for having multiple lenders. They need to know why finance sources have different tiers, rates, and terms, as well as different advances. Some focus on debt-to-income ratios while others focus on payment-to-income. Some sources include taxes and fees in their max advance, while others don’t.

Allowing customers to see your stable of finance sources online, as well as interest rates listed for each, is not only impressive, it demonstrates transparency. It also encourages them to let us compete for their business through finance sources that would otherwise be unavailable to them. The possibility of being able to secure a lower rate also increases the likelihood they will submit an online credit application.

Including a brief video highlighting a few advantages of financing or leasing through your store also helps to educate your customers before they come into the dealership. Hey, every customer wants to feel like they’re an informed consumer. Videos that educate and inform (not sell) create goodwill, customer loyalty, and interest in learning more.

Ad Loading...

2. Offer Pre-Approval before They Buy

In the real world, only a small percentage of people actually pay cash for a car. The rest of us have to finance them. Allowing customers to obtain pre-approval without committing to buy eliminates the fear of commitment and the risk of personal humiliation if they can’t qualify for financing. Basically, it allows the customer to take another step on the road to the sale with no obligation and zero risk.

The Federal Trade Commission’s ‘Finance a Car’ video advises consumers to check with their banks, credit unions and finance companies first, then take their best finance offer with them to the dealership.

Offering online pre-approvals is also a great qualifying tool, and can serve as a backup option in the event the customer doesn’t qualify for zero percent or extended-term financing. For most customers, allowing them to get pre-approved for vehicle financing is the closest they’ll ever get to paying cash. In fact, credit unions and direct lenders have been using pre-approval as a marketing tactic for years. Even the Federal Trade Commission encourages consumers to get pre-approved for financing before shopping for a car.

Knowing you’re pre-approved is empowering. It puts any advertised or promotional rate in context and allows you to feel like you have the flexibility to take your business elsewhere. It also demonstrates transparency, while shortening the time the customer spends in the dealership. And as we all know, educated customers are more likely to buy from and finance through the dealership that empowered them.

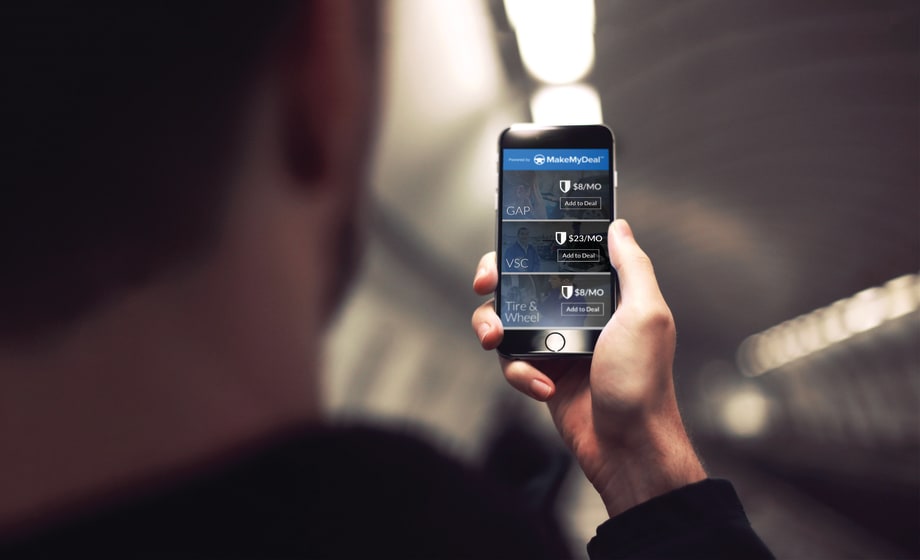

3. List Your F&I Products

Ad Loading...

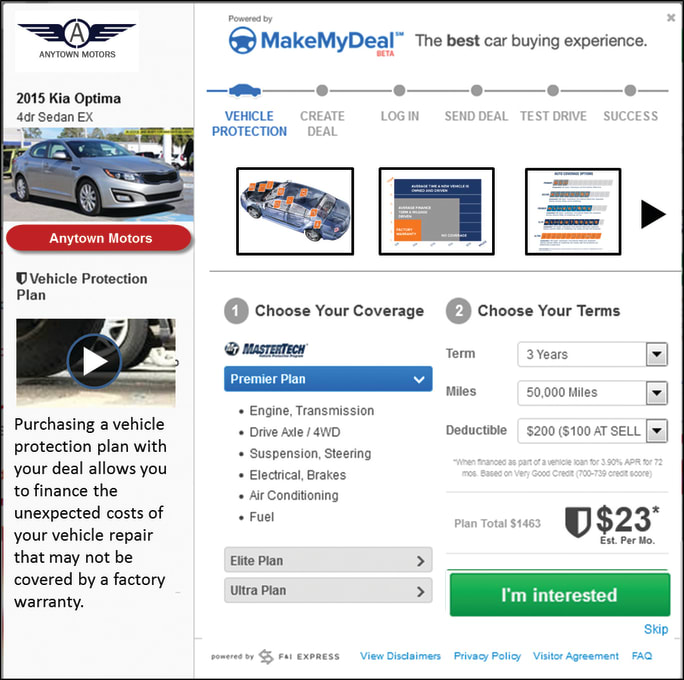

Your website should list all the F&I products you offer, along with a simple explanation and a few benefits listed for each. And whenever possible, include prices for those products. An example would be: “Tire-and-Wheel Road Hazard Protection from $442 depending on term and coverage selected.” Just make sure to use odd prices — $842, not $795 — to add credibility and legitimacy to your pricing.

Also list your product vendors and include links to their websites. Brief video explanations of every F&I product are also a must. Make sure they’re short, engaging, and designed to educate, inform, and create interest in knowing more. You may even want to include an “I’m interested” or “I need more information” button for each product so your F&I managers can engage the customer.

The real advantage of video is customers can hear and see the benefits of the product you offer. Hey, selling is a participatory sport, and there is a huge difference between passive and active engagement. And as we all know, people buy more when they’re actively engaged. Best of all, video persuades customers to spend more time on your website. Just make sure to include video testimonials from customers and experts, including your service manager or insurance agent, to help demonstrate the need and value of the products you offer.

Cox Automotive’s MakeMyDeal became commercially available in June 2014. The online deal-making platform allows dealers and buyers to negotiate deals from the dealership’s website. Customers can then calculate their monthly payment based on the negotiated price, their credit tier, desired term length, down payment, negative equity, and taxes and fees. Last November, MakeMyDeal added F&I Connect to its online deal-making process.

4. Educate and Inform Customers

When designing your F&I webpage, think about the information you’d want if you were shopping for a vehicle. A payment calculator is a definite must, but what about adding an affordability calculator? It could help shoppers understand how much vehicle they can afford, based on the payment and benefits they desire. Links to myFICO.com, the National Automobile Dealers Association’s “Understanding Vehicle Financing” page, and annualcreditreport.com would also be helpful. You may even want to consider links to consumer sites like autoconsumerinfo.com, which offers explanatory videos on all types of F&I products. It also offers a tool designed to help consumers see the extent of any manufacturer’s warranty.

Ad Loading...

The goal here is to create interest in talking to a finance manager. So your website could ask, “Would you like to know your credit score?” or “Would you like to chat online with a finance manager?” You can also offer helpful information, i.e., “5 Steps to Better Credit” or “How to Improve Your Credit Score.” Soliciting and posting positive F&I product reviews, YouTube videos, testimonials, and Facebook “likes” also needs to be an integral part of your F&I page.

5. Follow-Up Online Contacts

According to research from Harvard/MIT, contact rates decrease 100 times if you wait 30 minutes, as opposed to five minutes, to call back a lead. That’s why there needs to be a process in place and a concerted effort by everyone to follow up on internet contacts immediately. This requires a commitment to selling cars and F&I products the way customers want to buy, not the way we want them to buy.

Rapid response is also important, because when someone gets back to a customer immediately, we know where they are. Second, their interest and the question they have are still on their mind. This top-of-mind awareness reduces the chance they’ve already moved on to something else. And just think of the “Wow” factor. Hey, we need to impress internet customers by the speed of our response and our commitment to delivering the information they want when, where and how they want it.

So whenever a customer makes initial contact, whether by phone, email, text or via an online inquiry, the quicker we respond, the more likely we are to sell them. And with F&I income critical to every dealership’s bottom line, we really need to start that F&I relationship online.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.