Bridging the Digital GAP

Once the king of the car-buying process, dealers are under attack in today’s Digital Age. Industry insiders believe auto finance sources hold the key to restoring order.

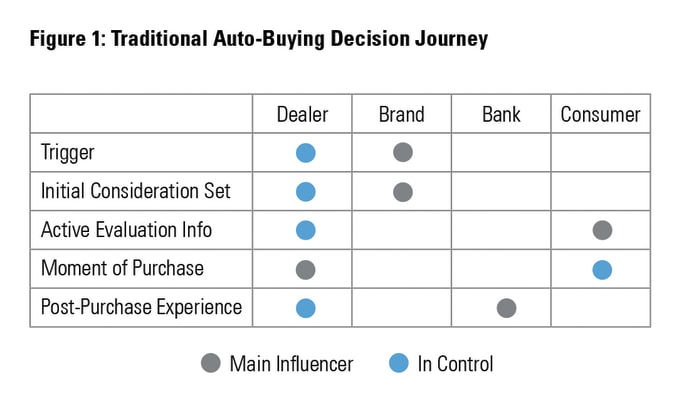

Once upon a time, dealers were the kings of the car-buying process. In those days, auto finance sources served the consumer indirectly through the dealer, and the arrangement seemed to work for everyone. Dealers liked the end-to-end control over the purchasing process, finance sources could bypass the crowded consumer marketing space, and consumers saved time.Today, the story has changed.

Empowered by better information, consumers live in a world of digital demand. They have greater choice, louder voices and higher expectations. They can easily learn what others paid for a car, see a specific vehicle’s quality score and a specific dealer’s inventory limitations — all from behind their computer screen, smartphone or tablet device. Rather than suffer through traditional negotiations, consumers today demand the same level of digital transparency and anonymity that online shopping gives them elsewhere.

Despite all these changes, the dealer is still the most powerful variable in the car-buying equation. The king, however, is under attack, especially when it comes to customer acquisition. Finance sources should consider the following three-step approach to bridge the digital demand gap.

Step 1: Rethink Supply and Demand

Research from IHS found that 44% of customers are dissatisfied with the amount of time they spend buying a car — a process that takes almost 15 hours on average. This dissatisfaction manifests itself in fewer trips to the dealership. In 2005, J.D. Power reported that the average consumer made 4.5 dealer trips per purchase. Today, consumers make just 1.4 trips, with a full 46% of buyers visiting just one dealership. New buyers spend 55% of their purchase time researching online vs. 41% of their time in the dealership.

This data offers a cautionary tale to complacent incumbents, but also to enthusiasts who think that dealers are poised for total disruption: 44% dissatisfaction is concerning, but surmountable, and fewer trips to the dealer mean less control, but control nonetheless. Indeed, our research suggests that 98% of cars are still purchased at the dealership, with only 5% of cars destined for online sales in 2020.

The reality is that dealerships and traditional auto finance sources will continue to play major roles in the consumer journey, especially at the point of purchase and beyond. Rather than reimagine their businesses, dealers and finance sources need to work together to ensure seamless integration between online acquisition channels and in-person closing.

Step 2: Build a Multichannel Strategy

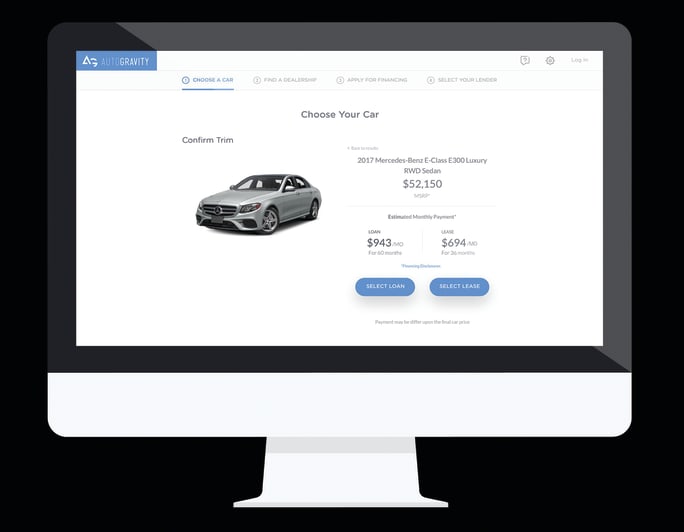

AutoGravity is one of a slew of fintech firms looking to alter how car buyers interact with both dealers and finance sources. With the financial backing of Daimler AG, the Irvine, Calif.-based company was founded in October 2015 by two former employees of Daimler Financial Services.

Innovative lenders should continue to devote attention to the dealer, because dealerships still perform vital functions. Until cars can drive themselves, it makes sense to keep inventories and service facilities close to people, where the dealer can also cross-sell F&I products such as GAP and service contracts, complete necessary paperwork (title applications), and facilitate the trade-in process. Dealerships do all these functions at an efficiency threshold that would be difficult to disrupt.

Still, captives, banks, credit unions, and finance companies can leverage new technological trends to acquire customers both inside and outside the dealership. First, lenders can partner with aggregators to turn online inquiries into applications. Aggregators, or comparison sites, use decision engines to filter lending products specifically to a customer’s need. The buyer benefits from comparison-induced price compression, but suppliers can capitalize on lower customer acquisition costs.

AutoGravity launched the first dealer-branded version of its app through a partnership with California-based Fletcher Jones Auto Group and its Mercedes-Benz dealerships. The firm then launched its smartphone-based auto finance platform this past January.

The most successful aggregator strategies target specific customer segments a finance source can attract and retain at a high lifetime value. Aggregators typically employ call center staff to close inquiries initiated online, and lenders looking to increase the payoff of the aggregator channel should consider ways to incentivize these contact centers the same way they incentivize the dealership. Others may prefer to use their own inside sales force and simply purchase customer information from the aggregator.

Second, as new entrants take functions formerly controlled by the dealer, lenders should look for ways to assume direct customer ownership, too. Direct lending happens today. Finance sources that leverage their own data can capitalize on the shift toward convenience and transparency. For instance, a bank could scrape deposit accounts to generate push notifications about lower car payments.

Finally, because direct lenders and aggregators have no choice but to send their customers to the dealership in the end, lenders should continue partnering with dealerships through traditional, incentive-based relationships. Dealers who maintain several lender relationships can often match or beat rates offered online. An internet-savvy customer who negotiated a low sales price and arranged a direct loan before entering the dealership could still “flip” toward a dealer-suggested payment or rate.

In cooperating with the dealer, finance sources should remember that dealership satisfaction influences a consumer’s willingness to repay. The more seamless the experience, the more satisfied the consumer will be. While auto-decision rates at the dealership have improved from less than 20% on average in 2010 to more than 50% over the last decade, significant room for improvement remains. Alternative deals can help lenders close the gap to 100% by allowing them to instantly pair a rejection letter with a list of pre-approved terms.

To generate these deals, decision engines scan a matrix of terms, rates, and down payments in search of a new financial combination that will convince the customer to stay. Technological intervention like automatic decisions and alternative deal engines can dramatically improve decision-making, speed up time to purchase, and create the hassle-free experience consumers expect.

Step 3: Adopt Technology to Drive Change

San Francisco-based Roadster launched its Express Storefront digital retailing and financing platform in June 2016. A month later, San Rafael, Calif.-based Toyota Marin became the first dealership to embrace the company’s ecommerce solution.

Finance sources need a blend of online and in-person experiences to ensure a seamless transition between digital acquisition and physical closing environments. At a minimum, lenders need to accept credit applications online and electronically return a response to both the customer and the dealer partner.

Additional capabilities, such as alternative deals, virtual F&I, online trade-in appraisals, and esignatures, can differentiate a finance source. In instances where software cannot generate an automatic credit decision, customers need someone who can help. Tools and material — for instance, webchat — can explain the financing process and help the consumer choose.

Finance sources that attempt to take the transaction completely online need to offer vehicle protection. GAP and service contracts form an increasingly large part of the dealer’s gross revenue, so work with the dealer to establish options and pricing for these aftermarket products. Lenders looking to sell these products can do so by building a solution in the online portal or by working with third parties, such as dealer portals or menu solutions.

Online trade-in quotes can also differentiate the customer experience, since those who can negotiate trade-ins online are more likely to leave the dealership feeling satisfied. As decisionmaking moves online, the technology providers present at the point of decision will increasingly capture brand-building business.

Electronic signatures and econtracts are also gaining wider adoption. After solving for aftermarket finance and trade-ins, finance sources need to close transactions online. When customers can sign digitally at the dealership, they experience a seamless transition from the digital to the physical world. In this situation, consumers also end their journey at the most natural time — right before they take the keys.

While some finance sources have launched dedicated portals, not all need to build the technology and integrations on their own. Finance sources of all sizes and budgets looking to enter online originations could consider a white-label consumer portal solution from a provider that supports their online strategy. While not a true “custom” solution, white label gives a degree of configurability that allows lenders to broadcast their brand while providing a modern consumer experience.

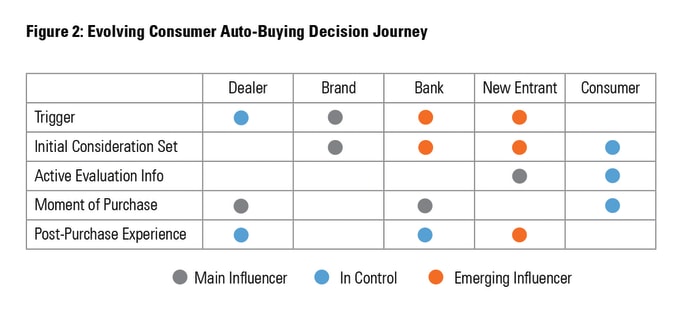

The road ahead looks clearer. Traditional dealerships will continue to dominate the end of the decision journey for the foreseeable future, but the beginning of that journey is changing. Consumers empowered by better information and higher expectations require dealers and finance sources to smooth the integration between online entry points and in-person closing.

In the new customer journey, auto finance source need to address aggregation channels, indirect dealer channels and direct lender channels. They need a strategy to pursue customers across these entry points as well as a robust technological offering that integrates seamlessly with the dealership. Dealers and lenders should work closely together, because not only does aftermarket financing form a growing percent of a dealer’s margin, dealer satisfaction also influences a customer’s willingness to repay.

Scott Hendriks and Vincent Weir are the director of product management and a senior business analyst, respectively, in the lending solutions division of Fiserv. Email them at scott.hendriks@bobit.com and vincent.weir@bobit.com.

More Auto Finance

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →