Edmunds: Term Lengths Stretch to All-Time High in June

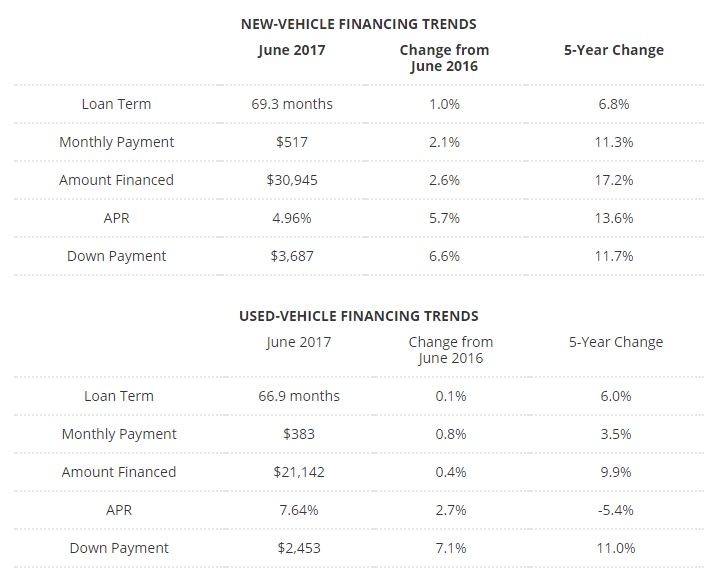

At a record 69.3 months, average new-vehicle finance terms have stretched 6.8% from five years ago. The average amount financed and average monthly payment also registered new highs.

SANTA MONICA, Calif. ─ Car buyers are pulling all levers to keep their monthly payments manageable as vehicle prices continue to rise. In June, one of those levers, average new-vehicle finance terms, stretched to an all-time high of 69.3 months, according to Edmunds.

The average, which is up 6.8% from five years ago, was recorded during the same month the average amount financed registered its biggest uptick in 2017. It rose by $631 from May to $30,945. Also setting a new mark for the year was the average monthly payment, which rose from $510 in May to $517.

"Stretching out loan terms to secure a monthly payment they're comfortable with is becoming buyers' go-to way to get the cars they want, equipped the way they want them," said Edmunds Executive Director of Industry Analysis Jessica Caldwell. "It's financially risky, leaving borrowers exposed to being upside down on their vehicles for a large chunk of their loans, but it's also a sign that consumers are still confident enough in the economy to spend more on their vehicles and commit to paying for them longer."

Edmunds also reported that the average APR dipped just below 5% for the first time since February, averaging 4.96% in June. The APR has increased 5.7% from a year ago and 13.6% from five years ago.

On Monday, Kelley Blue Book reported that June’s average transaction price grew by $511 from a year ago to $34,442, which was slower than normal for the month of June. The average, however, remained relatively flat with May.

“Transaction prices grew more slowly than normal in June, increasing less than 2 percent,” said Kelley Blue Book analyst Tim Fleming. “As the industry enters a ‘post-peak’ environment for new-car sales, more pressure will be placed on transaction prices.”

More F&I

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →

Your Office Is Talking

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

Read More →

F&I Training Fundamentals

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Read More →

Not Just Any Tire Will Do

More consumers and businesses are opting for all-season options for various reasons as safety, sustainability and convenience push practical change.

Read More →