As 2019 is unfolding, we are frequently finding compliance issues around what the industry knows as payment packing. We call it inconsistent payment quotes. Whatever its name, it’s a bad practice that must be attacked and eradicated.

What a NAAG

Despite improved industry education and a slew of regulatory enforcement actions, packing payments remains a popular pursuit at dealerships around the nation. Here’s how to prevent this highly illegal practice before it starts.

Establishing a process-defining policy that every sales manager acknowledges and agrees to is a critical component of any anti-payment-packing initiative.

Photo by pixhook via Getty Images

As 2019 is unfolding, we are frequently finding compliance issues around what the industry knows as payment packing. We call it inconsistent payment quotes. Whatever its name, it’s a bad practice that must be attacked and eradicated.

What a NAAG

During the late ’90s, dealers and F&I product providers in the Pacific Northwest were attacked with deceptive sales practices allegations by state attorneys general, one of whom coined the term “payment packing.” NAAG — an appropriate acronym for the National Association of Attorneys General — published a resolution declaring it a deceptive sales practice to be pursued under each state’s fraud statutes.

Finally, California and Minnesota eventually adopted a car buyer’s bill of rights, which outlawed payment packing and created additional forms designed to prevent it.

While this list is not exhaustive, here are some of the more common payment-packing scenarios:

• The number of days to first payment exceeds 45 days.

• The number of payments per year is less than 12.

• An undisclosed short term is used.

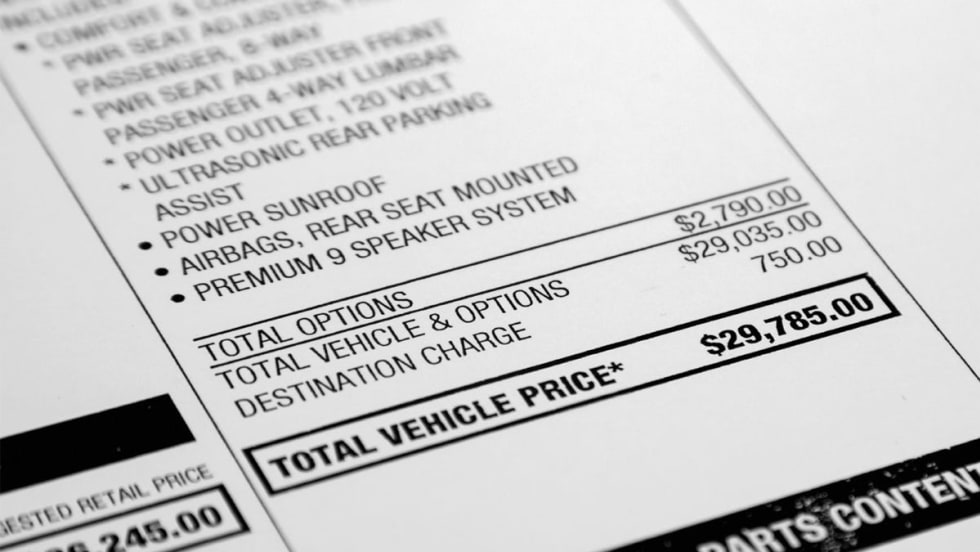

• A payment range is quoted in excess of $5 when using edesking software. (Most variables are accounted for to calculate the out-the-door number.)

• The sales tax is artificially inflated to increase the out-the-door number.

• The first pencil is quoted before the bureau is pulled, there is no approval and no exception noted, and the quote uses a rate other than the dealer’s default rate.

• Any pencil is quoted after the bureau is pulled, with no approval and no exception noted, and the quote uses a rate other than the dealer’s matrix rate.

• Any pencil is quoted after an approval is obtained and the quote uses a rate higher than the buy rate on the approval plus the maximum dealer markup allowed.

• Any pencil is quoted with a payment that includes undisclosed F&I products.

• Any pencil is quoted with a rate that exceeds state max.

Compliant Desking Processes

Establishing a compliant desking process must resolve potential desking issues. A dealer is well-served to establish a desking policy which defines the accepted process and obtains every sales manager’s acknowledgement and agreement to abide by the policy.

In Part Two of our series on “When Sales Is to Blame for Noncompliance,” we discussed the evolution of the desking process, shared a sample rate matrix, and described a compliant process for pulled bureaus. In Part Three, we continued with two additional possible outcomes — bureau not yet pulled and approval in hand — and an auditing process for all deals.

A third condition present may be that the customer has been submitted to a finance source and approved. The timestamp on the desking worksheet will be after the timestamp of the approval, which documents for the dealer’s defense that the exception to policy was due to more information than the standard transaction.

Some of the acceptable exceptions to policy include the customer who walks in with a pre-approval that the dealer intends to accept, or states that she has been approved by her credit union at 3.0%. These are the acceptable exceptions to using the rate matrix or the average rate. The defending point is the contemporaneous documentation on the worksheet: “Quoted at customer rate of 3.0%.”

Using this methodology shows that the dealer has a process and starts the defense against charges of payment packing.

And yes, good luck and good selling!

If a dealership is still buying Sharpies to complete paper Four Squares, you will probably find a higher percentage of packed payments or potentially discriminatory pricing.

Read More →

A CMS is the method by which a dealer manages the entire compliance process, including not only a compliance program, but also an audit function.

Read More →

Compliance expert examines the Fair Credit Program and its influence on dealers.

Read More →

The effective and consistent use of a checklist improves the deal, improves your CITs and will help with your compliance controls.

Read More →

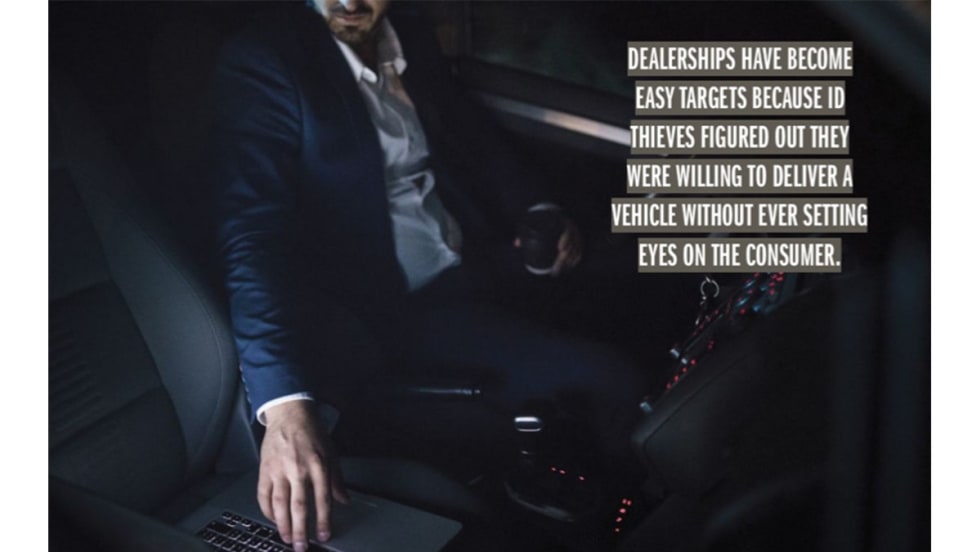

A dealership sold and financed a vehicle to an identity thief, even after seven red flags were identified. Truly managing the process means vetting and clearing any red flags before delivering the vehicle.

Read More →

You may sell a vehicle for more than the MSRP, but just be sure you do it right.

Read More →

There are five key credit determinants that lending institutions take into consideration when making the decision to extend credit.

Read More →

All four of our currently available data points suggest that a dealer cannot charge a consumer for a CPO warranty at the point of sale.

Read More →

A compliant credit application process is a pivotal part of the job. Do not let the process slip or a dealership could find themselves in some deep water.

Read More →

We all know identity theft is running rampant across the nation, making it even more important for dealers to do their due diligence when it comes to the digital delivery process.

Read More →