Is Amazon Really a Threat to the Car Business?

The big box revolution has irrevocably altered the retail landscape. Carvana’s success has dealers wondering whether auto retail could be next.

The concept has not been successfully applied to every industry, but grocers and office suppliers can verify the danger a “big box” competitor can present.

Photos courtesy Amazon.com Inc.

In the 1980s, we saw the arrival of the superstore. These were giant organizations that seized on an opportunity to be superefficient and dominate smaller competitors.

In the grocery business, the little mom-and-pop stores were purchased or put out of business by bigger organizations. Kroger, Publix, and Safeway quickly achieved dominance because of their ability to operate with more efficiency and leverage their costs across a broader base of rooftops.

Because of these competitive advantages, there are far fewer privately owned grocers left in our country today. It’s sad, but Mom and Pop simply couldn’t complete.

The world of office supplies offers another example. Locally owned suppliers bit the dust in large part because of Staples and Office Depot. Thomas G. Stemberg, the founder of Staples, was no dummy. After graduating from Harvard Business School, then managing several grocery stores, he recognized that the same philosophies used by those superstores could be applied to the business of office supplies. He was right. And he effectively changed the market.

Heck, Staples even created the “Easy” button! And it was easy — until Amazon arrived. Today, unless you need it right now, it’s just too convenient (and often cheaper) to buy from Amazon.

Will auto retail “superstores” put you out of business? There is no easy answer, but we can make informed predictions with the information we have on hand.

Amazon’s still-growing Seattle headquarters includes everything from offices and workspaces to botanical gardens and retail shops.

Why the Experts Are Concerned

At this year’s NADA convention, I listened to Brian Benstock, general manager of Paragon Honda and Acura in Queens, N.Y., discuss his thoughts on Amazon and the threat they pose. Brian is a top-notch GM in a store that sells over 1,000 units a month, making them the highest-volume dealer to take home the Precision Team Award for Acura and the President’s Award Elite for Honda. He knows a lot about the car business and how to succeed.

At NADA, he was speaking on the threat that Amazon poses to the automotive industry. He said, “Amazon wants it all, from A to Z” and “Bezos is coming!”

Amazon is a very powerful, well-organized company. Benstock is right to be concerned, and he’s not alone. But I’d like to share something that might help us all breathe a little easier.

Let’s go back to the Staples example. Some years after Staples achieved the top position in the office supply space, they thought that they could replicate their methodology in a different market and have the same success.

So they decided to tackle dry cleaning using those same principles. But they failed miserably. Why?

Upon diagnosis of what occurred and what prevented them from having success, we see a critical difference between office supplies and dry cleaning. In the office supply business, one simply buys a product; it is not personalized in any specific way. Any idea of “uniqueness” is a non-point.

An example would be buying a calculator: You’re going to check for the features, size, and price, but it’s still a calculator. Your clothing, however, is unique to you. You may want to discuss the care, cleaning methods and the intricacies of starching, stain removal, folding and hanging, allergies to chemicals, the use of eco-friendly products, button repair, hours, delivery, speed, and a myriad of other personal choices.

Staples executives thought they had an advantage. But operating a centralized location to do all the dry cleaning didn’t have the same utility as having a centralized warehouse for office supplies. The model breaks down because one company sells products and the other provides a service.

This is the fundamental reason why I’m not concerned about Amazon, yet.

Amazon fulfills orders quickly and efficiently. But unlike a car dealership, its sales don’t depend on personal interaction.

Do You Sell a Product or Service?

Carvana surprised a lot of people recently when they entered the list of top pre-owned units sold, but I wasn’t surprised. People doubted them when their prices were higher than most dealers and their F&I products could be bought online. This would be a death sentence if they were selling a product — but they’re not.

Carvana sells a service. The car is a byproduct. Customers can get a car anywhere, but Carvana offers an experience some people just prefer.

For most people, buying the car is a very personalized experience. They need to touch, feel, smell, drive and experience their vehicle beforehand. Others need a relationship and the security of knowing they can come back to the dealership if there’s a problem. These are amenities that Amazon doesn’t offer, yet.

Your concerns should be less about Amazon and more about the current big-box retailers in the automotive business. To compete effectively — and not join the mom-and-pop grocery and office supply stores — you will need to adapt.

This means making the process incredibly simple for your customers, giving information easily, and providing the ability to complete most of the transaction from home. This might seem intimidating, but I remember speaking with dealers 20 years ago who didn’t want to put their inventory online. No one would consider keeping that hidden now.

Back to Benstock. One key takeaway from what speech was the fact that “Our product has wheels. ... It’s easy to get it in front of the customer.”

This is a paramount advantage over Amazon. Amazon cannot compete when it comes to personal service. Benstock understands this. That’s why his salespeople often go to the customer for test drives. Any fear that a dealer has about driving the car to the customer and letting them experience it makes the sale harder, not easier.

If you don’t want your salespeople driving off to demo customers, ask yourself: “Is it the sales model that worries me, or am I actually more concerned about my people’s behavior?” If it’s the latter, you may have a people problem, and those same people are creating your sales problem.

Of course, maybe your concern isn’t showing vehicles or controlling employee behavior. You may worry you won’t have ample opportunity to discuss F&I products with the customer. This is where the model needs to change to be more efficient.

Today, we are seeing the emergence of companies with the purpose of bridging the information gap. One example is intice Inc., led by founder and CEO David Farmer. Farmer is a visionary. I recall when he began working to help dealers solve the problem of effective communication with customers, back in the late ’90s. His newest product allows the customer to do almost everything from home. They can literally desk their own deal, appraise their trade, and menu themselves on F&I products.

When they are done, their information is pushed into your CRM and your Dealertrack or RouteOne portal. All you need to do is “click” to submit the deal. When the customer does come in, they are already closed on price, payments, and F&I products. They still visit with F&I to finalize the deal and also discuss unselected or declined coverages (if necessary).

Surprisingly, when given time to consider coverage and payments in a less stressful environment, they tend to buy more products than you’d think.

The process is more similar to Apple than it is to Amazon. Yes, both sell products online, but you get personalized service with Apple.

When Transparency Leads to Profit

Having similarities to Apple is likely a benefit. How hard is it to find out the price for the AppleCare protection beforehand? It’s not hard at all. You can click, chat, phone, or walk in and ask. It is a take-it-or-leave-it proposition. Yet the majority take it.

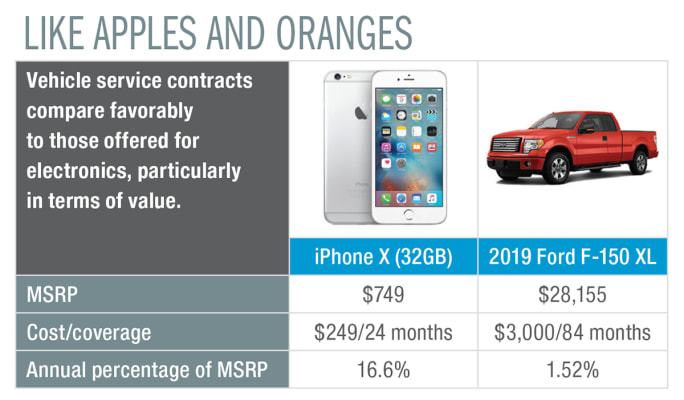

Consider this: 59% of Apple customers choose Apple Care protection on purchases made directly from Apple. How does that compare with automotive service contract averages? According to NADA, it’s 12% higher than the record 46% that F&I departments are currently generating.

This doesn’t come from a slick menu presentation or overcoming objections — quite the opposite. It comes from complete transparency. And probably most impressive of all, as a percentage of MSRP, AppleCare is around 16% per year. For most vehicles, it’s only about 1% to 2%.

By percentage, AppleCare protection is 11 times more expensive to purchase compared with adding a vehicle service contract to a Ford F-150. Yet the new truck is 38 times more expensive, has many more systems and components, all fed by more than 100 million lines of code. Smartphones top out at around 15 million.

“So what?” you say. “Amazon can sell protection products online too.” You’re right, but you cannot walk into Amazon and have your phone or computer repaired — just like you cannot have them work on your car. Again, the smartphone, computer, or vehicle is more personal. It’s like your dry cleaning. In so many ways, our customers still require human interaction with the sale.

For more than two decades, dealers have feared the idea of Walmart getting into the car business. This would be a realistic concern if it wasn’t for franchise laws and dealer associations diligently working to protect dealers.

Walmart has the available property and infrastructure to maintain a small supply of inventory, as well as the ability to provide personal service. Still, after 20 years of discussion, they recently decided to partner with a few dealers because direct-to-customer transactions are not a viable option for them.

Amazon does not currently have the infrastructure. They cannot provide a service to your customer like you do. They only sell products.

And even if they come in with a lower price, as we’ve seen from the Carvana model, many customers will still opt for the personal experience, security, and relationship that dealers provide over price. I’m not taking anything away from Jeff Bezos. I probably have an Amazon package on my doorstep right now. But his current model doesn’t work here.

For us, what we do next matters more than Amazon. We must trade in our fears for a focus on our customer’s future experience.

Lloyd Trushel is a 28-year veteran of the automotive business and co-founder of the Consator Group, an F&I development company specializing in customized training solutions. Contact him at lloyd.trushel@bobit.com.

More Showroom

Used Market Stabilizes

The Carfax Used Car Index noted a major drop in used-vehicle price increases in July after several months of hikes.

Read More →

California Hybrids Reach State Record

The Golden State still leads the country in electric-vehicle registrations, but much like the rest of the U.S. its hybrid market share is up while full electrics stabilize after a dramatic first-quarter dip.

Read More →

My Mercedes in the U.S.

The German brand debuted its studio dealership concept for the first time in the states in Los Angeles, tapping Americans’ penchant for creative distinctions.

Read More →

Used Sales Hit Summer Drag

The vacation season, combined with high prices, has dented deliveries and added to inventories, though supply is still slim enough to keep listings elevated.

Read More →

California Launches EV Rebate Program

Participating automakers are matching the state's $13.5 million investment in new electric-vehicle rebates scheduled to take effect later this summer.

Read More →

OEM Poll Sees Industry Evolution

Kerrigan Advisors’ survey of automakers finds that tariffs, technology, network tightening and other factors are poised to reshape auto retail.

Read More →

The Trade-In Paradox

Retailing older cars with confidence in today’s market is a matter of establishing and following a clear process that can turn greater profit for auto dealers as they aim to meet used-unit hunger.

Read More →

Focus on Vehicle Cabins

The market for interior materials will grow in coming years as automakers look to meet consumer demand while staying competitive with changeups to sourcing and included features.

Read More →

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →