COVID-19 Market Updates

Black Book published new insights to their weekly COVID-19 Market Updates, including wholesale prices, retail listing prices, overall wholesale sold volume, used retail listing volume, and BEV sales outlook.

Black Book published new insights to their weekly COVID-19 Market Updates, including wholesale prices, retail listing prices, overall wholesale sold volume, used retail listing volume, and BEV sales outlook.

IMAGE: Black Book

Here is a quick recap of the headlines from the last week:

Wholesale prices have begun to reverse course, with the rate of increase drastically slowing and some segments seeing values fall this past week.

Retail listing prices increased again last week.

Overall wholesale sold volume was on par with last year, but performance of different channels varies.

Used retail listing volume has stabilized at levels significantly lower than last year due to two main drivers: overall used inventory is lower, while many units in good condition are presold before they are listed online.

Weekly initial unemployment claims remained over the one million mark again last week.

TransUnion released July’s Industry Snapshot Report that shows that the number of accounts in hardship remains extremely high, almost 1400% above last year’s levels, but there are some improvements in prime risk tiers.

The University of Michigan’s Monthly Consumer Sentiment Index for August increased slightly but remained low.

According to the American Financial Services Association, Maryland and Washington DC are the last localities that still have a moratorium on auto repossessions. Many lenders and captives resumed the process in the last several weeks.

Last Week’s Highlights from the Wholesale Market

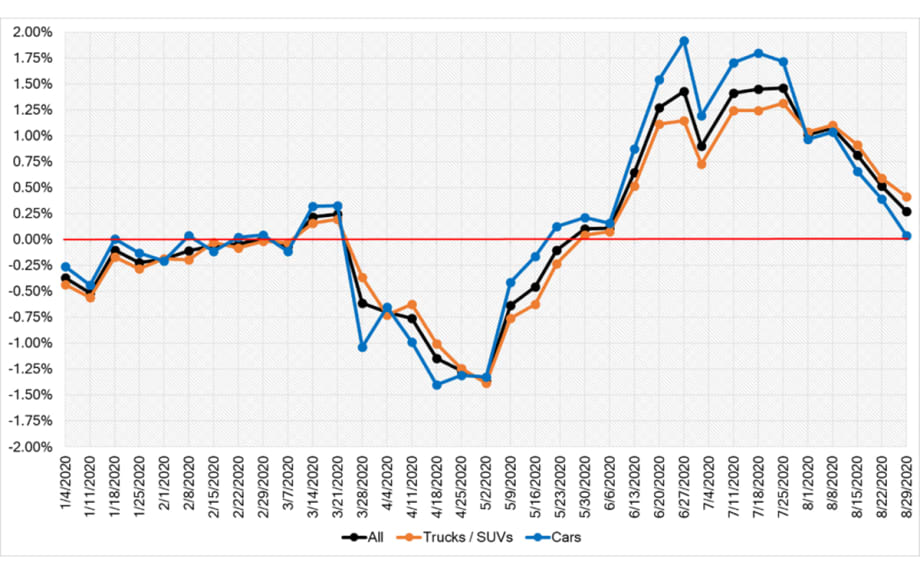

Volume-weighted, overall car and truck segments both showed gains for the14th week in a row, increasing 0.27% this week (compared to 0.52% the prior week). As for specifics, the overall Car segments increased by 0.04% (compared to 0.39% the prior week), and the overall Truck and SUV segments increased again this past week at 0.41% (compared to 0.59% the prior week).

The graph below shows week-over-week depreciation rates for the entire market, including Cars and Trucks/SUVs/Vans for the last several months. We have now experienced 14 weeks of overall market rebounding with consistent week-over-week increases in almost all vehicle segments. This past week was the first time in the last 13 weeks that the market showed signs of softening, especially in the Car segments.

News from the Retail World (Used and New)

As new deliveries are increasing, dealers are finding themselves being more selective in what they are stocking on their lots. For the last couple of months, they were finding themselves keeping trade-ins that they typically wouldn’t keep in an effort to get inventory levels up. Now, with the new inventory increasing, they are sending more vehicles to auction and returning to a more typical offering of age, brand, condition, etc.

As we are nearing a holiday weekend, dealers have been finding themselves backing off in their used purchasing until after they get a sense for the success of the Labor Day weekend sales. With schools resuming and consumers settling back into a more “normal” routine, foot traffic seems to be dropping off and dealers are exercising caution to not get caught with high priced inventory.

What Comes Next?

As more used inventory reaches the market and consumer demand weakens, we expect wholesale prices to stabilize, and possibly decrease, as early as Labor Day. The last two weeks saw moderation in both price increases and sold volumes.

We expect a large, incremental influx of used inventory to hit the marketplace starting in September and last into the beginning of 2021, coming from prolonged lease return delays and downsizing of rental fleets. In addition, lenders expect a significant increase in delinquencies and repossessions over the upcoming months as the economy continues to feel the effects of high unemployment. With much weaker retail demand, and a projected oversupply of used inventory, we forecast a significant drop in wholesale prices this fall, relative to the heights seen in recent weeks.

Longer Term View

Although the economic effects of the pandemic will continue to be felt as far out as three years from now (e.g. according to the recent CBO economic outlook report, the unemployment rate will not return to pre-COVID levels for at least a decade), we still project that wholesale vehicle values will return to the pre-COVID-19 baseline by 2023. Used supply will decline due to cuts in retail and fleet sales throughout 2020 and into 2021.

Economic Conditions

Job Market

Since the beginning of April, weekly initial unemployment claims have remained at record levels. Last week, the Labor Department reported that the US added just over 1.0 million new jobless claims. Since March, we have seen 23 consecutive weeks of record level layoffs and furloughs. The graph below compares weekly initial unemployment claims from the current recession against the Great Recession of 2007 – 2009. The severity and speed of job losses is unprecedented. The horizontal (x) axis is an offset (in months) from the beginning of the recession, week 0 being the week of March 21st.

In the early stages of the crisis, the US unemployment rate in April skyrocketed to 14.7%, the highest monthly rate since the Great Depression. The May unemployment level decreased to 13.3% due to the success of the Federal Paycheck Protection Program (PPP) and other stimulus measures enacted in part by the Federal Reserve and Government. As the country and the economy continued to reopen during the early part of June, the monthly unemployment numbers eased further to 11.1% and dropped to 10.2% in July. The Labor Bureau also noted in its reports that there was a classification error in its surveys, and the real unemployment numbers were actually higher for each month since March, as illustrated below.

There is a concern that without further federal stimulus, these gains will be temporary and employment numbers may deteriorate. According to a recently released CBO report, “the unemployment rate is projected to peak at over 14 percent in the third quarter of this year” before declining in the fourth quarter.

This recession is very different and unprecedented in the labor market – reflecting an almost instantaneous jump in unemployment with projected fast growth within a year. The graph below compares unemployment rates for the last several major recessions. The horizontal (x) axis is an offset (in months) from the beginning of the recession.

Although we have seen a reduction in unemployment claims, the initial economic shock and job losses have created a deep hole for us to dig ourselves out of. Between February and the end of July, the nation lost close to 12.9 million jobs.

Consumer Confidence

With a weakening of the economy and the increase in new COVID-19 cases across the South (which is now expanding to other hot spots across the country), consumer confidence retracted to the lows of April. The University of Michigan’s Monthly Consumer Sentiment Index for July, released at the end of July, decreased to 72.5 points, and the increase for August is 74.1. The report also predicts a further weakening in consumer confidence without substantial fiscal stimulus: “Although strong gains in consumer spending from the 2nd quarter lows can be anticipated, those gains will significantly slow by year-end without some additional fiscal spending programs to diminish the hardships faced by unemployed workers, small businesses, as well as support for state and local governments.”

Not surprisingly, consumer confidence has been on a rollercoaster the last five months. At the beginning of the year, it was strong – the University of Michigan’s Monthly Consumer Sentiment Index in February was 101 points. As the COVID-19 pandemic spread across the US, the Index dropped to 71.8 points in April and increased slightly to 72.3 points in May. During recent testimony by Federal Reserve Chair Jerome Powell, he noted that during the months of April and May, “stimulus checks and unemployment benefits are supporting household incomes and spending.” With these one-time stimulus payments and extended unemployment benefits helping the economy, the Index for June increased further to 78.1. The gains, however, were not uniform across the country. With a significant reduction in the number of COVID-19 cases, the Northeast region led the way with a record 19.1 point month-over-month jump, while the Southern region rose just 0.5 points due to the dangerous increase in numbers of new infections and fear of further shutdowns.

Gross Domestic Product (GDP)

The Bureau of Economic Analysis published an advanced estimate on GDP in the second quarter – real GDP decreased at an annual rate of 32.9%. This was the highest drop in GDP ever recorded.

Consensus states that the economy will start to grow in the third quarter compared to the previous one. Current “nowcast” from GDP Now model [from the Federal Reserve] estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2020 was 28.9% on August 28th.

Delinquencies Automotive Lending

The number of accounts in ‘hardship’ jumped substantially in April and kept increasing through June across all risk groups, according to the Monthly Industry Snapshot by TransUnion. The numbers stabilized in July and currently, about 6.3% of all accounts are in hardship – this is almost a 1,400% increase over last year. The increases are across all risk tiers. As deferrals expire in the upcoming month, coupled with a high unemployment rate, lenders expect a large portion of these ‘hardships’ to become delinquencies.

According to the “Senior Loan Officer Opinion Survey on Bank Lending Practices” from the Federal Reserve, lenders started to tighten standards on auto loans in the first half of 2020. Recently released results from the second quarter showed a substantial increase in the number of banks that tightened their standards.

Gas Prices

Gasoline prices reversed the May trend and then started to increase. Since their lowest point at the end of April, prices are up $0.39, to $2.17 per gallon last week and holding steady for the last several weeks, according to the U.S. Energy Information Administration.

Current Wholesale Market Overview

Auction Insights

For the past two weeks, auctioneers have been finding themselves having to work harder to get the bids up. This past week, more bids were resulting in ifs and no-sales as buyers showed hesitancy in stepping up an additional $300-$400 to meet the sellers’ floors.

With transportation continuing to present a challenge for buyers and sellers, due to the time and cost required to move vehicles, some sellers are making use of the virtual sales by listing their vehicles for sale, but vehicle pickup is at their dealership or another holding location. This is beneficial to sellers because it is allowing them to get their units offered for sale sooner.

The majority of states are now resuming repossessions. This is not the case for all states, as a few still have rules in place preventing repossessions. This has the potential to drastically increase volume at the auctions in the weeks and months ahead.

As new inventory deliveries have begun to increase, dealers are finding themselves being more selective about the trade-ins they are keeping for their lots and are starting to send more unwanted trade-ins to auction. This is a change from the trend we’ve seen over the last couple of months when any inventory was viewed as necessary, even when it did not meet the criteria of a dealer’s typical stock.

With complaints around condition reporting accuracy continuing to be a commonality, a seller’s reputation is more important than ever. Sellers with a solid reputation for offering quality used units have an advantage with buyers now willing to step up in price on units from a trusted seller. This is becoming even more important in recent weeks as we’ve seen the overall condition of units being offered for sale has deteriorated. This is due to a couple of reasons:

Remarketers are using this strong market to clean out their unwanted inventory and

the highest quality units are being scooped up by buyers upstream.

Auction operations update

Manheim added another six locations to its in-lane bidding pilot program last week. This now brings its total participating auctions up to 43.

By comparison, ADESA, who was the first of the large national chain auctions to launch the return to in lane bidding via the Digital Block, currently has 33 of its locations open for in lane bidding.

Auction Volume

In the last several weeks, we have seen the wholesale sales volume and sold volume decrease. The drops were not uniform across all auctions and platforms. The number of sales bottomed out around an 80% year-over-year decline when most auctions closed their physical sales (and some closed entirely) at the end of March. The graph below illustrates the estimated year-over-year change in sales volume of the wholesale market. The red line is the base line, and any dots above the line indicate higher amounts of sales vs. the prior year.

Sales Rate

At the onset of the pandemic, as shelter-in-place orders went into effect, sales rates quickly tumbled into the teens, but rates began climbing each week before stabilizing. After weeks of consistently strong sales, much of seller’s best inventory has been sold. As a result, sales rates have started to marginally decline as conditions of units being offered for sale has deteriorated. New inventory deliveries have begun to increase in frequency which is leading buyers to be more selective in their used purchasing. Black Book’s estimate of the overall Weekly Average Sales rate is presented below.

Current Wholesale Price Trends

Current Market Level View

Volume-weighted, overall car segment values increased 0.04% this past week. This is the lowest rate of week-over-week increase in values since the third week of May. Sub-Compact, Compact, and Sporty Cars all had values falling as demand for these segments has wavered. Luxury segments continue to show some stability with small week-over-week increases, with the exception of Premium Sporty Cars that have continued to gain momentum. When volume-weighting is applied, the overall Truck segment (including pickups, SUVs, and vans) values increased by 0.41% last week. Full-Size Trucks continued their ascent for the fourteenth week in a row. New inventory deliveries are starting to increase, after months of struggles to get production back going, so it is expected that this rate of increase will begin to slow. As seen with the Car segments, the volume leading, mainstream segments are experiencing smaller week-over-week changes. Compact Crossovers, the largest segment, was stable at a change of 0% (0.0004% when decimals are expanded).

Black Book’s Seasonally Adjusted Retention Index

The graph above compares Black Book’s Seasonally Adjusted Retention Index for the 2019 and 2020 calendar years. The Black Book Used Vehicle Retention Index is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically-equipped MSRP. It is weighted based on registration volume and adjusted for seasonality, vehicle age, mileage, and condition. The Index offers an accurate, representative, and unbiased view of the strength of used vehicle market values. It measures an ‘apples-to-apples’ year-over-year retention comparison.

2020 started slightly below 2019 levels, but the market showed early strength in February and March. As the US economy shut down due to the COVID-19 pandemic, we measured the highest single month drop in April of 6.9 points since launching the Index. As we entered July, wholesale prices continued the rebound that began during the second half of May and continued through the month of June, with June’s Retention Index climbing back to pre-COVID-19 levels with a record jump of 9.1 points. Black Book July’s Index value jumped above 2019 to 126.0 points as wholesale prices continue their climb. Our current “nowcast” for August stands at 124.7, a slight decline from July, but 7% above 2019 levels.

During the last recession (2007-2009), the Index declined by about 15 points in a span of 12 months before recovery started. We project that the Index will decline over the next five months after the summer’s strength.

Segment Highlight: Sub-Compact Crossover

Segment Overview

The Sub-Compact Crossover segment is a relative newcomer to the market, but now accounts for roughly 3% of the overall market share. This segment provides consumers a budget friendly and fuel-efficient crossover option. This is a good entry point into crossovers and is especially popular with younger drivers. Top players in the segment include the Nissan Rogue Sport, Hyundai Kona, Jeep Renegade, Nissan Kicks, and Kia Niro.

Recent Depreciation Rates

Sub-Compact Crossovers have historically been sensitive to any changes in the market and the stay-at-home orders due to COVID-19 were no different. At the onset of the pandemic, the Sub-Compact Crossover segment experienced large negative adjustments, larger than the overall market during most weeks. The same has been true for the rebound in values that started in early June, with many weeks the rate of increase being one of the largest across all segments. Last week was the first time the segment has depreciated since the first week of June as consumer demand is softening with continued high unemployment and multiple weeks without a second stimulus.

Model Spotlight – 2021 Kia Seltos

Kia has been busy keeping their portfolio fresh and exciting with the introduction of the wildly popular Telluride for the 2020 model year and now for the 2021 model year we have the newly launched K5 (the Optima replacement) and the Seltos. The Seltos is in the Sub-Compact Crossover segment so it delivers consumers the utility of a crossover, but the fuel economy of a car. It is available in either a 2.0L 4-cylinder or a turbocharged 1.6L 4-cylinder and consumers can choose between either front or all-wheel drive. As for driver assistance technologies, it has optional adaptive cruise control with lane-centering, blind spot monitoring with rear cross-traffic alert, lane departure warning with lane-keep, and automatic emergency braking with pedestrian detection. MSRP including destination starts at $23,110 for the S FWD or the LX AWD.

Used Wholesale Price Projections

Wholesale Price Impact Under the Most-Likely Economic Scenario

Wholesale prices dropped significantly in April as uncertainty over COVID-19’s impact and response dampened vehicle demand, resulting in an overall wholesale price decline of 5.9%. We saw a substantial improvement in prices during the last two weeks of May, and the monthly decrease was limited to only -1.5%. In June, wholesale prices continued to increase, and the overall market appreciated by a record 5.7%. As a comparison, last year’s prices declined by 0.9% over the same period. Wholesale prices increased by a record 7.0% in July. As of last week, prices increased by 2.7% in August.

Short-Term Outlook (Fall of 2020)

Black Book’s preliminary September Published Residual Values (dashed lines) reflect a new economic reality. Once the temporary strengthening during the summer months passes, we project values to stay below our pre-COVID-19 forecast over the next two years, with the deepest declines expected over the next five months. The green line represents our most-likely economic scenario, which does not include a possible second wave of COVID-19, as well as a still undefined second stimulus package. A more severe and prolonged recessionary scenario is shown in red. Projections are indexed to the pre-COVID-19 projections (black line). All values are weighted by the used vehicle sales volume (actual, where available, or projected).

We project a drop in wholesale prices compared to a pre-COVID-19 baseline this fall, as the US economy suffers through the effects of COVID-19. We anticipate that later this fall, wholesale prices will be approximately 5% lower than originally projected before the pandemic, due to a glut in supply and much weaker demand. Prices will start to recover in 2021 as the economy becomes stronger. We also anticipate that older (>6-year-old), cheaper vehicles in average condition will not decline as much due to increased demand for these units. Additionally, we project that newer (zero- to one-year old) models in good condition will retain their strength in the near future due to the continuous shortage of new inventory.

Long-Term Projections (36-Month Residual Values, Fall of 2023)

The effects of the pandemic will continue to be felt out to 36 months from now. We project that values will return to the pre-COVID-19 baseline as used supply will decline due to cuts in retail and fleet sales throughout the remainder of 2020 and into 2021.

Wholesale Price Impact Under a Severe Recession Scenario

In this scenario, we project a decrease in wholesale prices of up to 15% in early 2021, compared to a pre-COVID-19 baseline, with a slow recovery in the second half of the year. The effects of the pandemic and recession will still be impactful in 36 months, and we project a 10% market level decline of wholesale prices as compared to pre-COVID-19 projections for the second half of 2023.

Used Retail Vertical

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. From the peak in early April until the end of June, retail listing prices decreased by about 4%. Since the second week of June, we saw an increase in used retail prices fueled by higher consumer demand due to stimulus payments, the federal Paycheck Protection Program (PPP), and limited used and new inventory. In the last three weeks, used retail prices rebounded to above pre-COVID-19 levels. We expect used retail prices to decline later in the fall as demand will decline in the absence of stimulus payments during a weak economy.

Used Retail Inventory

Many dealers continue to report a shortage of used inventory in the wholesale marketplace. As a result, from the peak in February, we have seen a decline in the number of used retail listings by between 20% and 25%. The true shortage of vehicles is probably not as severe as this decline would lead you to believe, as many dealers sell some of their best inventory in the first several days before listing them online. Nevertheless, the shortage of used inventory helps keep retail prices elevated even in the weak economic conditions.

The graph above shows the weekly average of the number of retail listings collected by Black Book, indexed to the first week of the year. We see a continuous decline in the numbers starting at the beginning of May as the economy started to open in the states outside of the Northeast.

We started 2020 with active retail listings above the previous year’s levels. By July, the listing volume dropped to about 7% below 2019 numbers. Currently, the number of listings is about 9% lower compared to last year. Scarcity of used inventory is the main reason for this shortage of retail vehicles for sale. Another important factor that may cause the numbers of listings to decrease is that some of the inventory is sold before it has a chance to be listed online.

New and Used Retail Insights

This past week, dealers backed off in their purchasing with the reason being that they want to wait to see how consumer demand shapes up over the Labor Day weekend.

New inventory deliveries are starting to increase so dealers are finding themselves being more selective in the used units they are sourcing at auction and the trade-ins they are keeping.

Auto loan payment deferrals are starting to end for many consumers that took advantage of the lender assistance at the onset of the pandemic.

Auto transport has been a challenge throughout the pandemic; with increased demand and limited trucks on the road, auto buyers have had to increase the price they have to pay to get their auction purchases delivered and they are having to wait longer to receive delivery.

COVID-19 related employee absenteeism at auto manufacturing plants continues to cause slowdowns in production. Supply chain delays also continue to dampen the ability for manufactures to keep plants operating at full capacity. Parts coming from Mexico and plants located in the United States are facing the worst obstacles as it relates to COVID-19. For the most part, overseas parts suppliers and production are running at normal capacity.

Used Retail vs. Wholesale Prices Trends

Each week, members of the Black Book automotive analyst team, data science team and executive leadership team speak with no less than 30 dealers, along with buyer and seller representatives, wholesalers and others, who represent hundreds of franchise and independent dealers nationwide. These industry experts, along with experts we speak with from leading fleet management and rental car companies, auction leadership, and other industry experts, help to clarify and connect the dots between the wholesale and retail markets, adding to the insights that our data reveals.

Since the start of the pandemic, we have been observing different trends in both wholesale and retail prices (see graph below). In April and May, wholesale prices declined at a higher rate compared to retail prices. As margins grew, dealers reported healthy profits on a per vehicle basis. Retail prices displayed stickiness on the way down. Similarly, as wholesale prices came roaring back to pre-COVID-19 levels, retail prices are slow to recover, exhibiting the same stickiness on the way up. As wholesale to retail margins shrink, it is even more important for dealers to stay up to date on market movements. We are seeing this trend play out on dealership lots, where retail asking prices are not increasing at the same level as wholesale transaction prices. This means dealers are paying more at auctions and through wholesale channels, but those increased wholesale acquisition prices, as a percentage, are not flowing through to the retail lots and online listings, and ultimately to the consumer. The main driver of the slow increase in retail prices, based on our conversations with dealers, is simply the fear of sitting on inventory for too long, coupled with the added risk that the market makes a quick reversal, which leaves them stuck with a vehicle they paid too much for. Dealer sentiment is quite clear—if they are going to pay up for a vehicle in this environment, they are choosing to turn them quickly, even with less margin than normal, to ensure they are not caught with high priced inventory when the market does shift. There is no long game here. There is simply a need to fulfill demand in a risk filled environment.

The graph below shows this retail / wholesale dynamic since the start of the year. Prices are indexed to the first week. The black line is Black Book’s Retention Index (not adjusted for seasonality). It is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically-equipped MSRP. It is weighted based on registration volume and adjusted for vehicle age, mileage, and condition. The blue line is a retail index – average listing price of available retail inventory adjusted for mileage.

CPO Retail Sales

Certified Pre-Owned has grown in popularity as it provides consumers with an affordable used purchase option with low mileage (a typical 3-year-old CPO vehicle will have around 5,000 less miles than a similar non-CPO vehicle), but with the peace of mind that comes with a new purchase with the additional warranty. Some OEMs also offer special financing rates and terms for their CPO vehicles. For dealers, the cost to certify a vehicle is typically minimal and the return on the retail is typically greater. CPO vehicles are typically viewed as nicer condition units as there are minimum criteria a vehicle must meet to be able to be certified, and these typically involve age and mileage restrictions.

There are additional benefits to consumers that purchase through certain OEMs, including GM, who offers an exchange program on their Chevrolet and GMC CPO units. If the customer changes their mind within three days or 150 miles, the purchaser can exchange it for any Buick, Chevrolet, or GMC CPO vehicle. Nissan is improving their CPO program by adding additional benefits such as $750 Captive Cash on all CPO Rogue and Rogue Sports and adding one-year complimentary pre-paid maintenance when a CPO vehicle is financed through NMAC.

For some dealers, there is additional incentive to CPO a certain percentage of their used inventory as it bumps up their status with the manufacturer. For example, BMW takes into consideration a dealer’s CPO sales volume when deciding on the dealership’s new car allocation.

Cost of certifying a vehicle ranges by manufacturer. Typically, for mainstream OEMs, the cost to the dealer is $500 or less per vehicle, but luxury vehicles can reach into the thousands of dollars and vary by model. In most cases, the full cost to CPO a vehicle is the responsibility of the dealer, including any reconditioning that is necessary for it to receive certification.

Retail prices of CPO vehicles are generally about 3.5% higher than a similar non-CPO vehicle (adjusted for mileage). Similar to the cost to CPO a vehicle, the difference varies among the segments and, for example, can climb to about 7% for near luxury sedans.

New Vehicles Sales Outlook

Our New Vehicle Sales Outlook remains unchanged from last week. We anticipate a significant reduction in US new vehicle sales in 2020 (both retail and fleet sales) due to continued reduction in consumer demand. This is the result of several ongoing factors, including less miles driven due to remote work and shelter-in-place initiatives, high unemployment, and an overall feeling of uncertainty by consumers. Overall, new sales were down 22% during the first seven months of the year compared to last year (with a 12% YOY decline in July). Even as OEMs are restarting assembly lines, there are significant challenges ahead in order to return to a normalized production schedule as we reported in previous updates. The graph below shows our current projections for new vehicles sales for the remainder of 2020.

Due to continuous production disruptions and much weaker demand due to economic slow-down, we project a 25% drop (compared to pre-COVID-19 projections) in new sales in 2020 to 12.7mm units in our base economic scenario. In a deep economic recession scenario that is still possible this year, we project a 40% drop in new sales in 2020 to 10.2mm units as economy dips into a prolonged recession.

In the longer-term, we expect new sales volume to return to pre-COVID-19 levels within five years.

BEV Sales Outlook

As fast charging infrastructure continues to expand, we expect a slow growth in the battery electric vehicles (BEV) market in the next 2-4 years. Stronger growth is projected after 2025, but we do not expect a large shift to BEVs in the US market in the next 10 years, with market share only exceeding 5% by the decade end. Our current view is that growth in BEV demand will be evolutionary and not revolutionary.

Without substantial change in government policies (state and federal levels), we do not project a wide adoption of BEVs outside several states like California. As federal incentives decline, several states (especially CA) will increase rebates for lower priced BEVs to accelerate adoption. BEV prices are still projected to be substantially higher than comparable internal combustion engines (ICE) for the next 3-4 years.

Projections below include only light duty on-road vehicles as defined by Federal Highway Administration.

All the recent growth in the BEV market has come from Tesla: more than ¾ of all recent sales are Tesla models. There will be many new non-luxury (e.g. Ford, Nissan, and Volkswagen) and luxury (e.g. Mercedes-Benz and Infiniti) entrants into the market for 2021/22 model years.

Used Vehicle Supply Projections

Black Book projects a higher than expected used vehicle supply in the wholesale marketplace for the rest of 2020 due to several factors:

Delayed lease returns resulting from lease extensions offered by OEMs – more than 560,000 additional three-year-old units in the second half of 2020

Extensive de-fleeting by rental car companies due to lack of consumer and business traveler demand and financial pressure to raise cash – at least 250,000 one- to two-year-old vehicles will be added to the market in the second part of 2020

Dramatic reduction in auction activities due to COVID-19 in March, April, and May

Increased repossessions due to deteriorating economic conditions in addition to delayed repossessions during spring and summer months – we expect the volume of repossessed vehicles to at least double in the next six months compared to last year. This additional volume can exceed 1.0 million additional units in the next 6 months.

Short Term Lease Return Projections

When we started the year, lease returns were projected to hit a record volume of above 4.1 million units. Once the pandemic was underway and most manufacturing stopped, OEMs started to encourage lease extensions in order to push returns further into 2020, when they would be able to provide replacement vehicles. As a result, we project at least 560,000 additional units in the second part of 2020 (compared to the pre-COVID-19 estimates) due to a slowdown in sales in April / May, along with expected turn-ins of the lease extensions.

Repossessions

About 1.9 million vehicles were repossessed by lenders and sold (mostly) through wholesale channels in 2019. During the beginning of the pandemic, most of the states put a moratorium on auto repossessions and most of the lenders had deferral programs to help owners through the first several months of the recession. As of last week, only Maryland and Washington DC still have a moratorium in place. Illinois started repossessions just a few weeks ago. Most of the lenders have ended their deferral programs. Our survey of lenders and automotive recovery companies suggest that the volume of repossessed vehicles will at least double in the next six months. We expect that there will be substantial challenges at every step of the process as recovery, transportation, and disposal are not fully recovered.

Rental Unit Returns

Business and leisure travel collapsed at the end of March – air travel is still down by more than 70% according to the TSA. We expect a significant reduction in both categories for the remainder of 2020. In addition, there is no expectation that travel will return to pre-COVID-19 levels over the next several years. According to the IATA (International Air Transport Association), air travel will not return to pre-COVID-19 levels until after 2023. This puts tremendous financial pressure on rental companies that rely on air travel to reduce both their current fleet and scrutinize future vehicle acquisitions.

At the end of May, Hertz filed for bankruptcy in North America as a result of the pandemic. Several weeks ago, Hertz was able to secure a deal with its lenders that allows a gradual reduction of fleet – over 182,000 units between June and December. In addition to Hertz, we expect other rental companies will continue to reduce their fleet during the fall months to match lower demand for rentals. This practice will lead to over 250,000 additional rental units hitting the wholesale market in the second half of 2020.

The graph below shows Black Book’s projections for rental returns. The purple line shows the difference between current (darker rectangles) and pre-COVID-19 projections (lighter rectangles).

In the longer term (later 2021 – 2023), the drop in rental return volume will benefit the price of newer used units, as supply will be limited.

Longer Term Used Returns Projections

With the reduction in retail and fleet sales over the next several years, we project approximately 75k used units per month less in the market in 2023, compared to previously projected returns. This lower level of used inventory will be beneficial to used car prices as supply will be limited, helping to bolster valuations.

More Showroom

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →

California VW Dealers Go After Scout

The franchisees’ state-level actions follow a California auto dealers trade group lawsuit against the VW affiliate last year, both efforts to stop the EV maker’s plan to sell direct to consumers.

Read More →

EVs Gain Traction in Europe

First-quarter auto sales increased as more consumers took advantage of government incentives. Hybrid deliveries are leading the way on the electrifieds boom.

Read More →

California Holds EV Lead Despite Annual Decline

At nearly 14%, California had the lowest zero-emission vehicle market share in the first quarter since the fourth quarter of 2021, according to the California New Car Dealers Association.

Read More →