Black Book: Specialty Market Insights

Black Book released a newly published update to their COVID-19 Specialty Markets Insights report.

Black Book released a newly published update to their COVID-19 Specialty Markets Insights report.

IMAGE: Black Book

BLACK BOOK – As 2020 winds down, with most people happy to see it go, Powersports continues to be one of the relative “winners” this year. Prices are still elevated across the entire industry. Manufacturers are building new vehicles as fast as they can. Dealers have more customers than inventory. And finally, the arrival of colder weather has not significantly impacted the upwards trajectory the industry is on. Recent comments by both dealers and manufacturers indicate they are expecting the same trends that drove motorcycle, ATV, and watercraft demand earlier in the year, are going to propel snowmobile sales in the coming months. The biggest current concern is the lack of inventory, both new and used, that has been a problem for much of the past 6 months. Now that vaccines are beginning to roll out (the first ones going to Health Care workers just this week) and an end to the COVID-19 pandemic in sight, even if it is still half a year away, the big question is, what happens to powersports values in the future when life returns to normal? For now, demand continues to be strong, and the winter months, which normally see depressed pricing, are looking to be some of the strongest the industry has ever seen.

Dealers and Inventory Supply

A continuing issue facing the industry is inventory supply. In a conversation the other day with a member of the general public, someone mentioned to us that their local dealer was prospecting them to sell their bike. This is just one anecdotal example of a trend we have been hearing more and more about lately. Dealers are getting creative in looking for new units to fill showroom floors. Coupled with the increase in overall demand since the pandemic began, a much higher proportion of sales are going to first time buyers. This creates a dilemma for many dealers as trade-ins are a primary source of units for them to sell. Even many current customers are buying additional units, rather than replacing their existing vehicles. These trends have hit dealers hard, leaving many showrooms with a fraction of the inventory they would normally be carrying at this time of year.

Auctions have also been hit hard by the sheer number of first-time buyers as well. As the remarketing and wholesale industry has grown and expanded over the past decade, many more dealers today use the auctions as a significant resource for inventory management. The proportion of dealer consignments is much higher now than a decade ago. With the lack of trade-ins, dealers are sending fewer units to the auctions, and simultaneously unable to acquire them there as well. We have seen numerous examples of auctions offering free shipping and other incentives to motivate dealers to send more vehicles their way. The remarketing channels have also been slowed by the coronavirus, with federal and state restrictions affecting normal business activities, all sources of units for the auctions are still running below normal. The situation is improving every day, but the increased demand still far outstrips supply.

At the same time used vehicles are hard to come by, the new vehicle manufacturers are also having difficulty keeping up with supply. The OEMs have generally returned production to normal levels, but they are still unable to keep up with demand. As fast as units are shipped to dealers, many are pre-sold, and the rest are flying off the lots nearly as fast as they can be unloaded. The main issues facing the manufacturers are supply chain and capacity issues. Some are also still having occasional coronavirus flare-ups in various geographic areas that are impacting production volumes. Based on recent financial reports, most OEMs are on pace to match or exceed production levels from last year. Considering that many of their plants, and their suppliers’ plants, were shutdown for a month or more earlier in the year, this is quite a feat. The global nature of both current manufacturing supply chains, as well as the pandemic, means that virus outbreaks or disruptions anywhere on the planet have the potential to negatively impact production volumes half a world away.

Price Trends

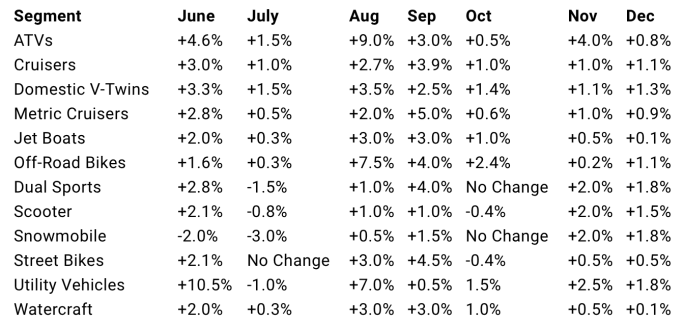

2020 Powersports Segment Changes

This is now the second month in a row where ALL segments we cover have increased in value. We are running out of ways to say this, but this is exceptional and unprecedented. At no time in the past can we recall not only the road going segments, but the watercraft and jet boats as well, increasing in value heading into December. In another month or two, we will be in the time period where these segments would normally begin to increase in value again. What happens when we get there will certainly be interesting. At some point these trends will not be sustainable. From January to today, our average Powersports vehicle has increased in price by a little over 21%.

Segment Comparisons: 2019 vs 2020

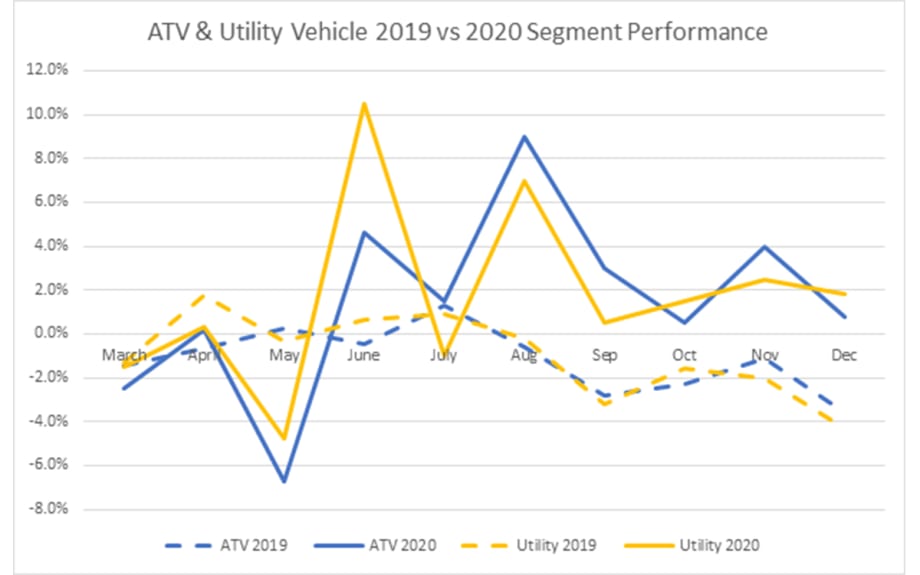

ATVs and Utility Vehicles

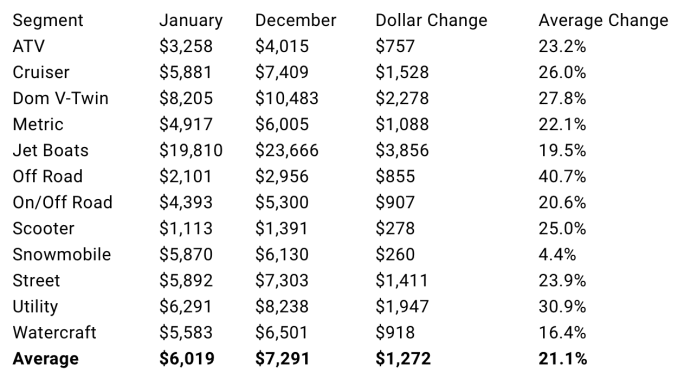

The ATVs and Utility Vehicles are up again this month, but by smaller amounts than for November. This is especially true for the ATVS, which are up less than 1% compared to last month’s 4.0% increase. The Utility Vehicles are up 1.8%, about 1/3 less than for November. For the full year, ATVs have increased in value by 23.2%, while the Utility Vehicles are up by 30.9%. These numbers clearly show the historic nature of this year. In January our Segment Index Average Value (based on the most recent 10 model years) for ATVs was $3,258. It has risen to $4,015 as we close out the year. Even more impressively the Utility Vehicles have gone from $6,291 to $8,238. The Utility Vehicles have been one of the strongest performing segments in Powersports over the past decade making it all the more impressive that they outperformed the smaller, less expensive ATVs this year.

Dirt Bikes

Once again, the most extraordinary segment this year. Off-Road bikes are up another percent this month. Since the pandemic began these units have been highly sought after by the general public. The combination of (mostly) low prices and their status as great beginner bikes continues to drive demand for this segment with average prices rising by 40.7% since the beginning of the year. A large number of these bikes have been bought by first time buyers looking for “socially distant” fun as many other forms of recreation have been severely restricted this year.

Cruisers

This segment continues to be one of the most surprising. Now that we are well into December, in many parts of the country bikes like these would typically be in garages already or headed there momentarily. To still be in demand at this point is something we have never seen before. It is only another month or two before we enter the period in time when this segment, as well as the other road-going bikes, normally starts to increase in value. Our Cruiser Segment Index Average Value started the year at $5,881 and has risen to $7,409 this month. That is a 26.0% increase for the year. Within the segment the domestic V-Twins performed better than the metric models. Domestics were up 27.8% vs the metrics 22.1% rise in value.

Street Bikes

Looking at the chart above, it appears that this segment has leveled off a bit in value, but it is important to remember that we are still looking at increases in value. Over time even these small monthly upwards trends in value add up. That is what we are still seeing. Much like the Cruisers, street bikes should be depreciating right now and for the next few months. From January to now, these bikes have seen their Segment Index Average Value go from $5,892 to $7,303, an increase of 23.9%. Like all the other segments, the increases in value this year are truly historic in nature.

Industry Insights and News

The US Government has approved the first vaccine for the virus that causes COVID-19 and initial shots are being administered as you read this. This marks the beginning of the end of this health crisis and with it a gradual return to normalcy.

Polaris CEO Scott Wine is leaving to become CEO at CNH, an agricultural and construction equipment manufacturer. Wine will continue to act as CEO through the end of the year while the Board works through succession and transition plans. A new CEO has not been named at this point.

Yamaha is hiring 300 new employees at its Newnan, Georgia location. Bob Brown, VP of Finance & Operations, stated the company was “gearing up now for an incredible 2021.” This is in addition to 100 new employees added a few months ago. This plant assembles side-by-sides, ATVs, watercraft, and golf carts. – From recent Powersports Business Article

According to the Motorcycle Industry Council (MIC), new off-road motorcycle sales are up 48.1% for the first 9 months of 2020 versus the same period last year.

The MIC is encouraging all members to take note of the constantly changing mask mandates and other safety measures related to COVID-19. As the pandemic continues to spike, many states are tightening restrictions. Follow the MIC @followMIC on Twitter for updates.

Auto defaults are rising as contract extensions and other accommodations from finance companies are expiring. S&P Dow Jones Indices and Experian data show auto defaults rising for 4 consecutive months. Levels are still way below (less than a third) levels seen after the Great Recession though. – From SubPrime Auto Finance News

Honda of South Carolina Manufacturing produced its 300,000 side-by-side on Nov 12, 2020. It was a Pioneer 1000 Deluxe five-seater. Congratulations!

MIC reports year to date sales of new motorcycles and scooters through September are up 10.2% compared to last year.

Kawasaki is spinning off their Motorcycle and Engine business into a separate company. This is to allow Kawasaki Motor Company to be more agile and responsive to the powersports market. US operations should see no change from this. – From Powersports Business

Ducati posted record sales in the third quarter of 2020, with a total of 14,694 units shipped worldwide. – From Powersports Business

RumbleOn reported gross profit of $2,271 for the third quarter for powersports vehicles. Total gross profit per vehicle grew over 260% year-over-year, though this includes automotive as well as powersports vehicles. – From Powersports Business

DelaerNews reported Triumph Motorcycles is offering a Certified Pre-Owned program. Triumph is bringing their existing program from Europe to the US in late November. They are doing this to help ensure that customers buying a used vehicle receive a similar experience to someone purchasing a new motorcycle. Triumph hopes this will also help preserve the residual value of new bikes. Dealers participating in the program will gain national exposure on Triumph’s new triumphcertified.com website. Benefits include a 1-Year Unlimited Mileage Warranty, 1-Year Roadside Assistance, Full Triumph Service History, Quality Check & Technical Inspection, and Complete History and Mileage Check.

A Washington Post article says jobless claims jumped last week with 853,000 people applying for new benefits. This is an increase of 137,000 from the prior week. An additional 427,600 claims were made through the Pandemic Unemployment Assistance program. The total number of people claiming benefits in all programs was a little over 19 million, though officials stated the tally may be inflated.

Auto Finance News – US hiring slows as coronavirus cases surge. The unemployment rate dropped .2% to 6.7%. This news was tempered by the fact that large numbers of people have stopped looking for work. The weak jobs report will likely increase calls for more stimulus from Congress and the incoming Biden administration.

Harley-Davidson recently announced their 2021 Dealer Meetings will be held virtually and the general public is invited to attend. The event will take place on January 19, 2021 and Harley will be unveiling their 2021 models and roadmap to the future as they continue to work on their “Rewire” and “Hardwire” plans.

Year in Review and What Happens Next

2020 started like many other years in the recent past, Powersports was coming off a solid, but not spectacular year, and looked likely to do about the same or maybe a bit better this year. Prices were running about the same level as the past few years, some segments were growing a bit, and others were in a slow decline. The major concerns at the last trade shows in 2019 were what could the industry do to grow the future rider base and how to expand the market for Powersports. The Great Recession that started in 2008 had left a lasting mark on the industry. Sales volumes have never recovered to pre-recession levels. There was, and still is, some excitement around electric vehicles bringing in new customers, but at the moment they still represent only a tiny fraction of new unit sales. The coming election season was generating its usual amount of anxiety, but otherwise it looked to be another solid year. Then the coronavirus showed up and everything changed.

Since none of us have lived through a global pandemic before, no one had any idea what the impact would be on our lives, or the truly global scale of such a crisis. For the industry, when the first health orders shutting down or restricting business activities went out, thoughts immediately turned to the last big economic shock, the aforementioned Great Recession, and what that did to Powersports sales and business, namely ruin them. For the first few weeks, and even months of the crisis, it appeared that might occur again this time. However, after the initial shock of our new reality, reports, sporadic at first, started to trickle in about dealers running out of inventory and having record sales months. This directly contrasted with the daily barrage of bad economic news and disruptions to our personal lives. What few saw at the time, but is obvious in retrospect, is that when you can’t go anywhere, can’t spend money on normal sports, leisure, and recreational activities, is that all that time and money will flow somewhere else. That somewhere else turned out to be Powersports. The Powersports industry was not the only beneficiary, home improvement sales went up, online retailing shot through the roof, laptops and webcams are still in short supply, and RV sales reached record heights as well. Each of these industries offered products or services tailor made for our new socially distant reality. Shortly thereafter, government stimulus checks, tax refunds, and enhanced unemployment benefits left many people with both the time, and the money, to spend in new and different ways.

This boom in Powersports activity showed up first in more rural areas in sales of off-road bikes, ATVs, Utility Vehicles, and Watercraft. It spread within a few months to metropolitan areas and added the Street Bikes, Scooters, and Cruisers. At the same time this spike in sales was occurring, dealers were learning to navigate sales in a “socially distanced” world. Mask wearing, extra cleaning and sanitation, capacity restrictions on showrooms, and reliance on digital communication, suddenly replaced traditional ways of doing business. The industry from top to bottom met this challenge, moving much of the sales process online, even going so far as to offer remote deliveries and touchless paperwork where possible (and legally allowed.) Since that time there has been a so far insatiable appetite for Powersports vehicles of all types. A side benefit of all this demand is that a huge proportion of 2020 sales have gone to first time buyers.

The industry has been struggling for years to regain the sales and interest levels last seen over a decade ago before the Great Recession. COVID-19 gave it a most unexpected opportunity to grow its audience, with this large influx of new customers. This large number of first-time buyers has impacted current business operations in many ways and offers significant opportunities for future growth. The immediate impact has been felt in a lack of trades that would normally help keep showroom floors fully stocked. Dealers and manufacturers have also begun devoting more resources to education and training for new riders to help them acclimate to their new vehicles. Many manufacturers have enhanced their after-sale communications and follow-up processes with an eye towards long-term retention of these new customers. The long-term impacts are a bit more unknowable, though the industry is hoping these new riders will keep their vehicles long after the current crisis ends and will be part of a larger base of users moving forward. Only time will tell if this occurs, but one thing Powersports has always had going for it is fun. Virtually every powersports vehicle offers excitement and fun as part of its core DNA. Once people are exposed to this, most in the industry are confident that they will become lifelong enthusiasts.

The incredible increase in demand for Powersports vehicles this year produced a tremendous increase in pricing across the industry. Among all ten major segments we cover in the Powersports market, the average increase in values (as measured by our 10-year Segment Index Average Values) was 21.1% for calendar year 2020. This ranged from a low of 4.4% for the Snowmobiles, to a high of 40.7% for the Off-Road bikes. Below is the full chart showing how each segment fared.

As 2020 draws to a close and most people wish it “good riddance,” the main questions facing the Powersports community are how long can the current strong demand and elevated pricing levels remain and what happens next spring and summer when the COVID-19 crisis begins to ease as a majority of the population gets vaccinated? As you are reading this, health workers in the country are receiving the first vaccinations for the COVID-19 virus. Assuming things go well, this will start the country on the path back to “normal.” When people are able to gather again without worrying about getting sick, travel, sports, and other entertainment activities should see a massive rebound. The big question is what happens to the outlets for that time and money over the past year, such as Powersports and RVing? Will the new customers gained by the industry remain, or will they sell their ATVs and motorcycles to finance travel and other activities? Ultimately, ending the pandemic will set in motion a chain of events that will return us to a new “normal,” but what will that look like? Once health concerns are removed, how fast does the economy bounce back? And, after the economy establishes a new baseline, individual industries like Powersports will need to find their natural place in this new world. For Powersports does that look, like 2019, or does it look more like 2007? Either way we will continue to track and report the results as 2021 unfolds.

Black Book COVID-19 RV Market Update

One of the top stories of the year has been the surge in popularity of recreational vehicles, commonly referred to as RVs. There are several different categories of RVs, based on their size and if they can move under their own power or have to be towed by another vehicle. As COVID-19 began to rampage across the country, much of the travel, hotel, and hospitality industries were dramatically affected: flights were canceled, hotels were closed, and restaurants and bars limited to carry out only. People were afraid to be around other people and tried their best to limit contact whenever possible. All of this isolation began to take an emotional toll on many people, who began to look around for a way to get themselves and their families out of the house and hopefully find something fun to do. RVing, which has been popular for decades, but has really seen explosive growth in recent years, was viewed as the perfect solution: drive (or tow) your RV to a vacation spot, park it reasonably far away from other people, cook your own meals, and do fun activities with your friends or family. No flying, no hotel lobbies, and no crowded restaurants. RVing is essentially tailor made for enjoying a vacation in the great outdoors while remaining socially distant from other groups of people. Millions of people already own RVs, so for them planning a trip was as simple as picking a destination and hitting the road. But what about the people without RVs? They’d have to either purchase or rent one if they wanted to plan a vacation. To say that quite a few of them did so might be an understatement. RV dealers have been reporting record sales since late spring, and many are still seeing traffic on their lots late into the colder months that far exceeds what is typical for this time of year. In fact, most dealers’ biggest complaint is still lack of enough inventory, even though the manufacturers are continuing to pump out units at historic levels. The RV rental business, both traditional agencies and peer-to-peer, is also rocketing along, with many of the large national booking services reporting explosive growth and record rentals, including the cold weather months that generally see activity taper off. Although everything seems great now, there are those in the industry who are beginning to feel a little nervous about the rate of growth and are starting to question if it is sustainable. There are also concerns about whether the existing industry infrastructure can handle the increased volume and manage the expectations of the flood of new customers, many of whom are new to RVing and have their own ideas about customer service based on what they are used to from other industries. Another point of concern is the ongoing surge of COVID-19 cases that is sweeping across the country, and for whatever reason, seems to be hitting Elkhart, Indiana, the epicenter of US RV production, especially hard. Even with the mid-December rollout of the COVID-19 vaccine, many continue to ask: will governments be forced to announce new health related social restrictions and business closures, will consumers continue to buy big ticket items as infection rates and hospitalizations surge, and will RV manufacturing plants have to shut down again?

AUCTION ACTIVITY

RVs have been red hot on both the wholesale and retail levels since hitting their lows in April, when most of the economy was effectively shutdown. In addition to dealers selling every new unit the manufacturers can produce, the used side has been thriving as well. Pre-owned units have always been an important part of their inventory mix, but with the inability of many dealers to get all of the new units they need, sometimes waiting months for ordered inventory, they have turned to scouring the auctions for used models to help fill out their lots, even if the balance of new to used units they typically maintain is leaning much more heavily towards used than usual. Dealers never want to turn a customer away because they don’t have a suitable unit in stock, and also don’t want their lots to look so depleted that potential customers drive by without looking, so they have been stepping up and paying higher than typical prices for used units at auction for the past several months. In fact, the sales averages for both motorhomes and towables hit record highs this month, which is especially noteworthy given how far into the economic and manufacturing recovery we are.

In October, the average motorhome’s selling price at auction dropped $4,040 (7.1%) to $53,601 from September’s all time high of $57,641, but is still the third highest amount ever recorded. One year ago, in October 2019, the average selling price at auction was $46,293, so even with this recent drop, we’re still quite a bit higher. Auction volume was up 4.4% from September, and the average age of all units sold declined to seven years (MY 2013) from last month’s eight.

Towables, which include conventional bumper pull travel trailers and the larger fifth wheels, continued their record setting pace, coming in at $19,196, which was $558 higher (2.9%) than September and the highest amount ever recorded. One year ago, the average towable selling price was $15,188, so the market is still substantially above that benchmark. The volume of towables sold at auction was down 3.6% from the previous month due to supply issues, and the average age of all units sold remained seven years (2013 model year).

Industry Overview

Since hitting a low point in April due to COVID-19 induced shutdowns, the RV market has rebounded dramatically. Production resumed in many locations in May, and RV manufacturers have been running at capacity since June, with each successive month seeing increases over 2019’s totals. According to the latest RV Industry Association data, this winning streak continued in October, with total production coming in at 47,326, an increase of 21.4% over the 38,972 shipped in October 2019, and 5,817 more than September 2020. Looking at the specifics, towable units came in at 42,854, which is up 22.9% over last October’s 34,866. Motorhomes also saw an increase, rising 8.9% year over year with 4,472 units shipped compared to 4,106 last October. Year to date, total shipments are sitting at 347,517, which is only off 0.4% from 2019, especially impressive given the nearly two-month long manufacturing shutdown earlier in the year.

The RVIA reports that, as usual, conventional bumper-pull travel trailers led the way once again in October, with 32,593 units shipped. The larger and more expensive fifth wheel style came in at 9,431, folding camping trailers reached 525, and truck campers rounded things off with 305. Travel trailers and fifth wheels saw big increases over 2019, up 25.1% and 20.8% respectively, but folding campers dropped 14.2% and truck campers slid 22.4%. On the motorized side, Class A totals were 1,136, Class Bs hit 927, and Class Cs reached 2,409. Class Bs (Van campers) saw the largest increase over 2019 at 115.1%, with Class Cs rising 12.0%, but Class As dropped 25.5%. Park model RVs were down 5.7% from last year, with 333 wholesale shipments.

The RVIA is forecasting that total sales will come in at just under 424,000 units for 2020, which would be a modest improvement over 2019’s 406,070, and if that projection is correct, it would account for the fourth highest total of all time, even with the shutdown. Sales are expected to be even better for 2021, with totals reaching 502,500, an increase of roughly 20%, and only the second time ever to break through 500,000 sales.

Retail registrations are closely related to wholesale RV shipments, especially in the current environment when dealers are selling units as fast as they can get them in. Statistical Surveys recently announced that October set a record for retail RV registrations, which is the fifth month in a row that new records have been set. Retail RV registrations totaled 40,467 in October, up 21% from the same period in 2019.

The United States Census Bureau recently announced that as of 2017 (the last year information was available) there were 2,667 RV dealers in the United States, and they generated $25.9 billion in total sales, up 81.5% over 2012, with an average of $9.7 million per dealership.

The Bureau of Economic Analysis announced that the outdoor recreation industry generates $788 billion annually, supports 5.2 million jobs, and compromises 2.1% of US GDP. RV’s individual portion of that is $18.6 billion, which surprisingly is higher than both agriculture and mining.

RVIA’s “Go RVing” ad campaign reached the milestone of serving more than one billion impressions across all media platforms between August 24th and December 31st.

John Spader, of Spader Business Management, commented that a large portion of RV dealers’ growth and net profit was due to the surge brought on by the pandemic, and cautioned that they should not count on business remaining at these elevated levels forever.

The boating industry is closely related to RV, and in a similar fashion to the explosive growth in RV sales since late spring, powerboat sales are up nearly 10% year over year, with September coming in 22% above August. Overall volume is expected to exceed 300,000 units, a level not seen since before the Great Recession.

Thor’s most recent fiscal quarter showed a 17.5% increase in net sales to $2.54 billion, with profits increasing 112.8% to $113.8 million. Their market share for the quarter was 43.4% for motorhomes and 43.6% for towables. Their wholesale order backlog has increased 195% from this time last year.

Winnebago reported fiscal fourth quarter revenue of $738 million, which is up 38% from 2019. Towable revenue was up 35% and motorhome was up 50%. Net income rose to $42.5 million, up 33% from 2019. Full year revenue came in at $2.4 billion, up 18.6% from last year.

Patrick Industries, a major supplier of components used in RVs, reported net income of $37 million on sales of $701 million, up 75% year over year. Their earnings per share was $1.62, which is up 76%. They also announced a dividend increase of 3 cents per share to 28 cents from 25. They are forecasting that the supply chain will return to normal in 2021, barring any unforeseen circumstances.

Lippert Components, another major RV supplier, reported net third quarter sales of $827 million, 41% higher than 2019. Net income increased $32.5 million to $68.3 million. They also announced an upcoming expansion in Elkhart County that will add several hundred jobs.

With the explosive growth the industry has been seeing, a few areas of concern have arisen. The manufacturers have been making and shipping RVs as fast as possible, all the while contending with supply chain issues, labor shortages, and public health challenges. Many consumers have been complaining that their RVs are arriving with multiple defects and that dealers are taking a long time to repair them. Repair Event Cycle Time has been a problem that dealers have struggled with for years, mainly due to a shortage of qualified technicians, but the sheer number of new customers who are more accustomed to the reliability and fit and finish of new cars has really exacerbated the problem. One industry observer we spoke to said that some of this consumer frustration has led to a steep increase in negative reviews on RV dealers’ websites.

Another area of concern is the resurgence of COVID-19, especially in RV manufacturing hub Elkhart, Indiana. Elkhart General Hospital reached capacity in mid-October and reported that deaths were up 40% since Labor Day. Elkhart County has raised their COVID threat level to Red, the highest level, which will evoke certain public health protocols to limit the transmission of the disease.

The RVIA has written letters to all state governments asking that all aspects of the industry, including manufacturing, transport, sales, and service, be considered “essential” and be allowed to remain open in the event of public health related closures.

Dealership Updates

For the past several months, we have been reporting that dealers from all over the country were posting record sales, and the only thing holding them back was a lack of inventory. This is true this month as well. Although the RV sales boom has been going on for several months, many dealers from all over the country have reported that their sales are still very strong, and that interest has not really tapered off with the onset of cooler weather. Many of their customers are first time buyers, which they acknowledge is great for growing their customer base, but since they are new to RVing, they do not have a trade-in, which is a key component of how dealers typically acquire pre-owned inventory.

One RV dealer in the Northeast we spoke to a few weeks ago said that their sales were up 20-30% year over year, with their biggest months being July and August. They are still selling units as fast as they can get them, even though this would normally be the time of year they were slow. Customers are telling them that they are buying now so that they will have an RV to use next year. In fact, many customers whose RVs have arrived at the dealerships are not even picking them up until spring. The dealer commented that they’re OK with this because it makes their lot look like they have more inventory and may encourage customers to drop in. They typically try to maintain a 90-day supply, but this year have been less than 30 most of the time. They are light on used inventory because less than 10% of their buyers have a trade, whereas usually that number is closer to 20%. They also noted that manufacturers have increased prices by 10% or more and they are passing this along to the customers, who are paying it without too many complaints. He concluded by saying that travel trailers in the $20,000 – $30,000 range fly off their lot, but it takes a little longer to sell fifth wheels that start in the $40,000 – $50,000 range.

Another RV dealer in the Southeast we spoke to agreed with many of the comments the first dealer made. Their inventory is about a third of what it usually is, they were not getting many units on trade, and every new model that arrives at their dealership is essentially “pre-sold”. They remarked that many of the new units they receive need much more dealer prep than usual, particularly with regard to fit and finish, and it is not unusual for them to come back for service after the new owner has used it once or twice and noticed additional items that needed attention. They noted that they are doing much more service work than usual, and they were scheduling appointments out three to four months, partly due to the amount of time they are having to spend on new units. They concluded by saying that they were having problems getting all of the parts they needed, and that the manufacturers were charging them more in transportation costs, sometimes in the hundreds of dollars per vehicle.

The RV industry is starting to see growing consolidation within the dealer body, similar to what we’re seeing in the automotive world. Camping World has made several acquisitions recently: Noble RV in Minnesota (four locations), bringing their total in the state to eight; All RV Needs in Oregon, bringing their total in the state to five; Paul Sherry RV in Ohio, bringing their total in the state to four; and Outlet Recreation in Fargo, North Dakota, their first in the state. They are also opening a new location in Lincoln, Nebraska in 2021. Their goal is to have a physical presence in all 48 contiguous states by the end of 2021 (they are currently in 36). RV Retailer recently purchased Sierra RV, a 90,000 square foot facility with 32 service bays, in the Salt Lake City area, their first in Utah and 36th overall. RV Retailer also purchased two dealerships in North Carolina: Golden Gate Trailers and RV in Raleigh and Camptown RV in Charlotte. Lazydays announced that they completed the acquisition of Camp-Land in northern Indiana, which serves the Chicagoland metro area.

Rollick, which connects in-market consumers with dealers, reported that RV dealers using their Sales Driver product saw an increase in traffic of 58%.

The state of New Mexico announced a temporary closure of dealership sales departments in mid-November, the first such order in the US since earlier in the spring. They noted that service and online sales were permitted.

Many in-person RV shows have been canceled over COVID-19 concerns, but many dealers are hosting “virtual” online shows to connect with their customers. The 2020 Hershey, Pennsylvania RV show, billed as the largest in the country, was canceled in September, and the Ohio RV Supershow scheduled for January 2021 has also been canceled. This is a significant blow to dealers who exhibit there; one who was interviewed said that he usually sold upwards of 300 units, which accounted for a good portion of their yearly sales. The RVIA has announced that they will no longer host their annual California RV Show. On the brighter side, organizers of the massive 2021 Florida RV Supershow, scheduled for January 13-17, are still planning on holding the event live at the Florida State Fairgrounds.

The RVDA and Baird Consultants reported that a lack of inventory was the number one problem facing RV dealers. They reported that the average inventory supply for motorhome dealers was recently 24 days, down 75% from last year’s 100. 81% of dealers surveyed said their inventory was too low. Towable dealers reported having a 30-day supply versus just over 100 at this time last year. 97% of dealers surveyed said this was too low. The RVDA predicts it will be March 2021 before inventories hit an equilibrium.

The Federal Reserve recently announced that they intend to keep interest rates low through 2023 to help stimulate the economy. This will have a positive impact on dealers who plan on borrowing money to enlarge their facilities or acquire additional inventory. Low rates will also encourage consumers to make big-ticket purchases, such as RVs.

Consumer Updates

RVs are still very popular with consumers. Their number one attraction is the ability to travel while remaining socially distant. In several industry surveys, many have responded that they are afraid to fly on an airplane, stay in a big hotel, and be around large crowds. The RV industry has been promoting RVing as a great way to vacation while avoiding all of the pain points for consumers, and they have been very successful in getting their message out.

In addition to the increasing sales we have already mentioned, RV rentals are up dramatically as well. This applies to the burgeoning peer-to-peer market as well as dealer rental units and dedicated rental agencies. RVShare recently announced that 80% of their users were new in 2020. They revealed that the average RV owner could receive $16,000 a year in rental income, with Class As having the most potential at $60,000, Class Bs with $40,000, and Class Cs at $45,000.

The National Park Service announced that Yellowstone had their most ever October visitors this year with 360,000, which is 110% higher than last year. The previous record was set in 2015 with 252,000. Grand Teton also reported record visits for the month, with 351,000, up 88% from last year. The previous record was 207,000 in 2018.

The state of California announced new COVID restrictions in regions with less than 15% capacity in their hospitals’ ICUs. Although dealerships and campgrounds can stay open, overnight campground stays are not allowed.

Glamping, which is essentially luxury camping, has grown dramatically during the past several years, and is projected to reach $4.8 billion by 2025. Glamping can range from high end motorhome resorts with top notch clubhouses and facilities to luxury tents or yurts that are already set up in scenic locations and include maid service and other resort amenities.

Recent industry surveys have found that many consumers are considering working out of their RVs. As many jobs can be done remotely needing little more than an Internet connection, many workers are taking their RV to a vacation type spot and working from there as opposed to their home. Another survey found that many parents whose children are attending class remotely are considering taking their family on vacation during the school year, since their children can watch the class from a vacation spot as easily as from home. This has been nicknamed “roadschooling”.

Black Book COVID-19 Collectible Vehicles Market Update

Last month we covered a variety of recent collectible car auctions, several of which were live, in-person events. We noted that although they were generally smaller than pre-pandemic levels and included social distancing and other safety and public health accommodations, they seemed to be successful, with strong bidding and reasonable sell through rates. It appeared that they had a handle on the pandemic, and they had figured out ways to safely hold live events. Fast forward about six weeks: the Coronavirus has been raging seemingly out of control, with hospitals nearing their maximum capacities and the daily death toll hovering around three thousand. With the January Arizona auctions only about a month away, many industry watchers began checking their inboxes and news feeds several times a day to see if there was any news of changes or cancellations. That news finally arrived a couple of days ago, and I don’t think that anyone was really surprised. Scottsdale, which accounted for total auction sales of nearly $250 million in 2020, was not going to happen in its usual form this coming January, and most people that I’ve talked to thought that it was for the best. We’ll take a look at each of the major auctions and see what their plans are for January.

If you’re talking about Scottsdale, you have to start with Barrett-Jackson (2020 total $137 million). They have been putting on their flagship auction since 1971, and had big plans for their January 2021 sale, which would be their 50th Anniversary. They even held a smaller “practice” auction a few months ago at the same venue to make sure that they could successfully incorporate all of the recommended health and safety guidelines while still hosting an enjoyable and successful event. Their auction is the sun around which all of the other Arizona events orbit, so any changes to it would produce significant ripple effects. Although it came as no surprise, it was still somewhat shocking when they announced a few days ago that they had postponed their January auction until the end of March. If you have ever been to a Barrett-Jackson auction in-person, or even watched one on television, you know just how big of an event it is. There is just no way that they could have held it in January, even if they followed every possible public health protocol and limited attendance. A big part of what makes Barrett-Jackson special are the crowds and the “Super Bowl” like atmosphere. Hopefully the vaccine, distribution of which started earlier this week, will go smoothly and get the Coronavirus under control by March to the point where events like this are possible. If not, it may have to be postponed a while longer.

Russo and Steele (2020 total $8 million), which bills itself as a smaller, more intimate version of Barrett-Jackson, is currently planning on holding their auction as scheduled on January 23rd, although they are limiting auction entries to eighty vehicles and restricting in-person attendance to bidders and sellers and their guests, and have implemented the usual health and safety enhancements. Given the current surge in infections, please check their website for any up to the minute changes to their schedule.

RM Sotheby’s (2020 total $30.3 million) will also be offering eighty vehicles, and is calling their January 22nd event a “livestream auction with limited attendance”. It will be held at a new venue this year, the private OTTO Car Club. RM specializes in well documented, high-end collectible vehicles, so even if bidders choose not to attend in-person, they would be able to follow along online and bid remotely with confidence.

Gooding and Company (2020 total $35.8 million) had previously announced that they would be replacing their usual in-person event with one of their Geared Online auctions, of which they have successfully staged several earlier this year. As opposed to a live auction, this will be a timed sale with bidding starting at 9:00 am on January 18th and closing on a staggered basis starting at 10:00 am on January 22nd.

Worldwide Auctioneers (2020 total $5.5 million) has moved their scheduled Scottsdale auction on January 21st to their headquarters in Auburn, Indiana on January 23rd. It is still billed as a live auction, but with the ability to bid remotely. Please check their website for more information and additional updates.

Bonhams (2020 total $8.4 million) is scheduled to hold their Scottsdale auction January 21st at the Westin Kierland, describing it as “live and online”. As of press time, they have not made any scheduling announcements, but please check their website for updates.

MAG Auctions (2020 total $1.7 million) has postponed their Scottsdale auction. Please see their website for more information.

Leake Auctions (2020 total $16.6 million) is still deciding how to handle their Scottsdale auction. Please see their website for more information.

Although it’s not in Arizona, you can’t talk about the January auction scene without including Mecum’s Kissimmee, Florida sale (2020 total $95 million), currently scheduled for January 7th – 16th. It is still listed online as a live event with in-person attendance welcomed, although the usual safety protocols (masks, hand sanitizer, social distancing, entry temperature checks, etc.) will be enforced. Mecum has successfully run several in-person auctions in the past few months, and Florida has been keeping the state as open as possible, so there is a strong possibility that this auction will be able to go on as planned, but please check their website for the most recent updates.

AUCTION ACTIVITY

Mecum’s Kansas City auction was held November 20 -21 as a live event. Total sales came in at roughly $7 million with a sell through rate of 70%. One of the featured draws of the auction was the Etzel Family Collection, which was sold in its entirety, including the top three selling 1957 Cadillac Eldorado Biarritz.

The Top Ten Sales from Mecum Kansas City:

2005 Ford GT Coupe $264,000

1970 Ford Mustang Boss 429 Fastback $209,000

1957 Cadillac Eldorado Biarritz Convertible $110,000

1970 Shelby GT500 Fastback $110,000

1957 Ford Fairlane 500 Skyliner Retractable Hardtop $99,000

1970 Chevrolet Chevelle SS454 LS5 Coupe $96,800

1936 Diamond T REO Flatbed Car Hauler $95,700

1970 Ford Mustang Mach 1 Twister Special $90,200

1955 Cadillac Series 62 Convertible $88,000

1971 Dodge Charger R/T Coupe $86,900

RM Sotheby’s Online Only: Open Roads Fall 2020 included 77 vehicles and a wide array of memorabilia. Of those 77 vehicles, 39 were declared sold, for a sell through percentage of 51%, with the total dollar amount coming in at just over $4.4 million.

The Top Ten sales from RM Sotheby’s Online Only Open Roads:

1969 Ferrari 365 GTC Coupe $660,000

2005 Ford GT Coupe (Chassis #2) $522,500

1951 Porsche 356 Coupe by Reutter $330,000

2005 Ford GT Coupe $291,500

1931 Mercedes-Benz 370 S Mannheim Sport Cabriolet $286,000

2019 Porsche 911 Turbo S Exclusive Cabriolet $247,500

1956 Austin-Healey 100 M Le Mans $236,500

1990 Ferrari Testarossa $170,500

1994 Porsche 911 Speedster $132,000

1935 Packard Super Eight Convertible $121,000

Mecum wrapped up their year in Houston, Texas, their sixth large scale live auction in the past eight weeks. This sale finished with an impressive 84% sell through rate (442 of 526) and a total of $14.7 million, which brought their last two months up to a total of $75.5 million and 2,700 vehicles sold.

The Top Ten Sales from Mecum Houston:

1941 Ford Custom Pickup $206,250

1990 Land Rover Defender 110 Custom $176,000

2013 Ford E350 4×4 Based Custom Camper $176,000

1934 1934 Lincoln KA Custom Convertible $137,500

1987 Porsche 930 Turbo Coupe $132,000

2004 Ferrari 360 Spider $126,000

1962 Mercedes-Benz 190SL Roadster $121,000

2020 Chevrolet Corvette Convertible $115,500

2010 Dodge Viper ACR Coupe $110,000

1963 Lincoln Continental Convertible $106,700

PRICING TRENDS

The Vintage Muscle Car segment represents high performance cars from American Motors, Ford, General Motors, Dodge, and Plymouth produced from the mid-1960s through the early 1970s. A few representative examples would be American Motors AMX 390, Buick GS400/GS455, Chevrolet Chevelle SS396, Dodge Charger R/T, Ford Torino Cobra 428CJ, and Pontiac GTO. After dipping in the latter part of 2017, they have been on a general upwards trend as similar new cars being sold currently have rekindled interest in the segment.

The Vintage Pony Car segment represents sporty vehicles from American Motors, Ford, General Motors, Dodge, and Plymouth produced from the mid-1960s through the early 1970s. A few representative examples would include its namesake Ford Mustang, Chevrolet Camaro, Pontiac Firebird, Plymouth Barracuda, Dodge Challenger, and AMC Javelin. These vehicles also dipped in late 2017 but have been on the rebound ever since. These vehicles are typically less expensive than those in the Muscle Car segment, and their generally high production numbers (over 1,000,000 Mustangs in 1965-66 alone) make them a popular choice for collectors, especially those new to the hobby.

The Vintage American Post War Classic segment represents “big American iron” produced from the mid-1940s up through the mid-1970s. This encompasses a wide range of vehicles, and the prices can correspondingly range from the mid-teens up to the low six figures. A few representative examples would include 1953-54 Buick Skylark, late 1950s Cadillac Eldorado (Seville and Biarritz), Tri-Five Chevrolet Bel Air, Ford Crown Victoria, Lincoln Mark III, Chrysler 300 Letter Series, and Pontiac Bonneville. These vehicles have been squarely at the heart of the hobby for decades, but shifting tastes have led to a gradual decline in their values as older collectors age out of the hobby and are replaced with younger ones who grew up with different cars.

The Vintage European Sports Car segment represents classic “sports cars” in the purest sense of the word. Most of Europe was busy rebuilding their infrastructure after the devastation of WWII, so it took until the mid-1950s for the European automotive industry to get back on track. Although most immediate post war European vehicles were strictly utilitarian, a few lighter hearted vehicles were part of the mix. It is commonly believed that many American GIs experienced these vehicles first hand while serving in post WWII Europe, both in Great Britain and on the Continent, and many either brought vehicles home with them on the strength of the US dollar, or sought them out from the fledgling importers or “foreign car” dealerships when they returned home. This genre would include MGs, Alfa-Romeos, Triumphs, Porsches, Jaguar, BMW, and some Mercedes-Benz models. These vehicles are really considered to be “timeless”, as their appeal spans multiple generations. The market has its peaks and valleys, but for the most part is very stable.

The Vintage Exotic segment focuses on high dollar European exotic sports cars produced from the late 1950s up through the mid-1970s. This is without a doubt the top of the market. This segment includes Ferrari 250s, 275s, and 365s, Lamborghini Miuras, Maserati Ghiblis, Mercedes-Benz Gullwings, Porsche Speedsters, and coach-built Bentleys and Rolls-Royces. Although most owners of these vehicles are very wealthy individuals, the market is very volatile and fluctuates quite a bit as it falls in and out of favor, sometimes being seen as a safe haven in which to park money and other times as an unreasonable extravagance. Values have been stable for several years, with some individual models generating more interest than others.

The Vintage Pickup Truck segment has recently expanded to include collectible SUVs, many of which were constructed on modified truck chasses. A few examples are Ford, Chevy/GMC, and Dodge pickups built from the mid-1940s up through the early 1970s, early Jeep CJs, Toyota FJ40s, International Scouts, early Range Rovers, and first generation Chevy Blazers and Ford Broncos. Pickups have been on a run for the better part of a decade, and SUVs have been on fire for the past two or three years, with values doubling or sometimes tripling during that time frame.

Black Book COVID-19 MD/HD Trucks and Commercials Trailers Market Update

Industry News

According to the Center of Disease Control and Prevention, truck drivers and other workers in critical and essential jobs may be among the first to receive COVID-19 vaccinations.

On December 13th the first shipments of Pfizer’s COVID-19 vaccine left Michigan to be delivered to distribution centers all across the country. UPS Inc., FedEx Corp, and Boyle Transportation are the reported carriers of around 3 million doses.

The overall market continues a slow depreciation trend as we close out the year. This is following months of increased pricing due to supply issues in most segments.

Recent reports continue to show increased production from all OEMs and classes; however, many experts believe production will not meet current demand until Q3 of 2021.

Auction Activity

Overall, the wholesale market has cooled down as we close out 2020.

Dealer and end user participation remains strong at auction; however, we are seeing significantly fewer units showing up at physical auction.

Used prices remain relatively stable with very little week-over-week price changes.

Medium and Heavy-Duty auctions remain active despite the drop in volume. From July through October of this year, we have seen steady increases in the number of units being remarketed. However, in November we saw a 36% reduction in auction volume in the number of 2014-2018 model year units being remarketed.

On the retail side, we saw a -0.08% reduction in the number of units being remarketed from October to November.

As supply continues to fall, we expect prices to remain relatively stable through Q1 of 2021.

Live in-person biding is available at some Manheim Specialty Auction locations. Digital bidding and online buying are available at all locations. For info on locations and dates, visit https://www.manheim.com/.

Taylor and Martin remain online-only with onsite inspections available before the sale. For info on locations and dates, visit https://www.taylorandmartin.com/auctions/.

ADESA Specialty Auction remains digital with in-person bidding and online buying opportunities. For info on locations and dates, visit https://adesarigs.com/adesarigs/#!/loc/home/lang/en/.

Ritchie Brothers’ continues bidding in online-only format with no buyer fees and limited onsite inspections. For info on locations and dates, visit https://www.rbauction.com/covid-19.

JM Wood continues to have live in-person and online auctions. For info on locations and dates, visit https://www.jmwoodlive.com/.

Insurance Auto Auction branch locations are currently open. Digital auctions are accessible via IAA AuctionNow™ https://www.iaai.com/

Effective June 19, 2020, IAA is requiring that all visitors wear face coverings while in branches and offices. Also, if a visitor is previewing vehicles, a Safety Vest or Bright Colored Clothing is required.

Retail Sales Trends

The chart below shows new retail sales numbers for the past three years as reported by the U.S. Bureau of Economic Analysis.

Recent figures show New Retail Sales for classes 4 through 8 continue to improve after the lows experienced in May of this year due to the pandemic.

In March, retail sales were at 33,441 units, which is 10,494 less than those retailed in March of 2019.

After months of factory closures and shutdowns, retail sales jumped 22% from May to June as the country began to rebuild.

In October of this year, retail sales grew to 40,390 units, which is 4% higher than the 38,584 units reported in September of this year.

Retail numbers are expected to continue to grow. As new supply returns to a normal level later in 2021, we expect used prices to begin to slowly decline.

Supply for most segments is not expected to meet demand until the third quarter of 2021. This will help used trucks retain their value as the transportation and construction industries demand product.

The chart below from Ward’s Automotive shows new retail sales by class for September and October. Overall, retail sales and OEM production continue to slowly increase; however, we are well behind last years figures.

According to Wards Auto’s chart above, retail sales figures grew 0.68% from September to October of this year. This is following a 3.2% increase from August to September.

Class 3 Retail Sales increased 7.9% from September to October.

Class 4 Retail Sales dropped 41.5% from September to October.

Class 5 Retail Sales increased 10% from September to October.

Class 6 Retail Sales increased 15.1% from September to October.

Class 7 Retail Sales increased 5.6% from September to October.

Class 8 Retail Sales increased 1.9% from September to October.

Dealership Updates

Reports and conversations from dealers indicate that retail transactions remain strong; however, recent reports indicate that used retail sales are down 0.08% from last month.

It’s going to be interesting to watch each segment as OEMs continue to increase new truck production as safely as possible.

As supply continues to be an issue, retail and wholesale pricing remains stable.

Service departments remain extremely busy; however, supply chain issues are increasing turn time as mechanics and technicians have to wait longer for the parts they need.

Over-the-Road (OTR) units with excessive miles continue to show price softening, while lower mileage units increase in value due to their scarcity.

GDP and the housing market continue to show positive signs, which is helping keep demand and values strong on dump and straight trucks.

Clean up along the East Coast due to recent severe weather continues to help strengthen new and used demand for Construction/Vocational Units.

Fewer trucks and tractors are showing up at physical auction as many dealers are retailing trade-ins due to limited supply. This will help improve values even further for some segments as we head into 2021.

Wholesale Value Trends

The chart below shows average wholesale pricing changes by class over the past fourteen months.

Since the beginning of the year used supply has moved from saturation to scarcity in all model classes.

Shifts in demand, freight, and overall used supply have created volatility in wholesale values.

Since August, used values for most classes have continued a positive trend; however, recent reports indicate values are leveling off and beginning to deteriorate.

For the next few of years, used Over-the-Road (OTR) and Regional Tractors (Day Cabs) will likely have increased mileage as transportation companies were forced to keep units in service longer than originally anticipated.

Over the past couple of weeks, values began to level off and depreciate on some Over-the-Road units due to their availability compared to Regional Tractors.

This past month, all classes reported drops in wholesale pricing.

The chart below shows average wholesale price changes for 2018 and 2019 model year class 7 and 8 units by segment over the past 3 years.

Model Years 2018 – 2019 HD Construction/Vocational segment dropped an overall weighted average of $445 (-0.5%) in December, compared to the $460 (0.5%) average increase seen in November.

Model Years 2018 – 2019 HD Over the Road Tractor segment dropped an overall weighted average of $34 (-0.1%) in December, compared to the $1,085 (1.6%) average increase seen in November.

Model Years 2018 – 2019 HD Regional Tractor segment dropped an overall weighted average of $841 (-1.3%) in December, compared to the $1,731 (2.8%) average increase seen in November.

Page BreakThe chart below shows average wholesale price changes for 2010 – 2017 model year class 7 and 8 units by segment over the past 3 years.

2010-2017 HD Construction/Vocational segment dropped an overall weighted average of $129 (-0.2%) in December, compared to the $753 (1.3%) average increase seen in November.

2010-2017 HD Over the Road Tractor segment dropped an overall weighted average of $14 (-0.0%) in December, compared to the $785 (2.6%) average increase seen in November.

2010-2017 HD Regional Tractor segment dropped an overall weighted average of $217 (-0.8%) in December, compared to the $992 (3.8%) average increase in November.

The chart below shows average wholesale price changes for 2018 – 2019 Medium Duty trucks over the past 3 years.

Overall, medium duty units remain stable as we close out the year. In December we saw prices drop an overall weighted average of $221 (-0.5%), compared to the $1,319 (3.0%) increase seen in November.

Used Construction and Medium Duty truck demand remains strong due to production concerns, increased demand in last mile delivery, and improving housing and construction markets.

The chart below shows average wholesale price changes for 2010 – 2017 Medium Duty trucks over the past 3 years.

Much like the late models, older Medium Duty trucks reported a drop of $206 (-0.9%) in December, compared to the $699 (3.0%) increase seen in November.

Values have begun to level off; however, increasing demand due to a number of recent storms and natural disasters paired with limited supply has helped to improve overall values for the units in this segment over the past couple of months.

Fuel Trends

The chart below illustrates average fuel prices over the past 12 months

Fuel prices have remained relatively stable over the past couple of months and are projected to remain flat through the remainder of the year.

The current national average for regular diesel is $2.38, which is down $0.67 from this time last year, when the average was $3.07.

The current national average for regular gasoline is $2.14, which is down $0.45 from this time last year, when the average was $2.59.

Freight Trends

The chart below shows freight demand as reported by the ATA Truck Tonnage Index.

After months of freight improvement following the outbreak in March, freight demand dropped slightly from July to August, which helps shed a little light on recent price softening in some segments.

The chart below shows that even with the recent drop, freight demand remains relatively high.

It’s important to point out that freight is extremely healthy despite the recent reduction in demand. Reports have indicated that both truck and commercial trailer orders are increasing, which is a positive sign for both the trucking industry as well as the US economy.

Commercial Trailer Value Trends

Heading into 2020 a surplus of commercial trailers in the market caused an increase in depreciation for all trailer segments.

COVID-19 has affected commercial trailer values in much the same way as it impacted Medium and Heavy-Duty truck and tractor values.

As a result of mandated shutdown periods, excess inventory was sold off while only a limited number of new units were placed in the market, which helped improve demand, allowing prices to stabilize or increase in some cases.

Recent week-over-week trends indicate that pricing has leveled off and may begin to slowly depreciate as production slowly increases.

The charts below show average wholesale price changes over the past two years for the commercial trailer segments Black Book analyzes.

Wholesale prices for Curtain Side, Drop Style, and Dry Vans all improved heading into the final quarter of 2020. Manufacturer production slowdowns have significantly reduced vehicle supply, which has increased values for most segments.

Live Floor and Lowbed trailer values stabilized heading into Q4, while an increase in the supply of Livestock and Dump trailers has caused values in those segments to depreciate.

Refrigerated and Chip-Ag. Open Top Vans also stabilized heading into the final quarter of 2020. Steel and Steel Drop Deck Flatbeds are in high demand because of their practicality and versatility; from transportation to construction, these units are used in a wide variety of markets.

Originally posted on Auto Dealer Today

More Showroom

New Vehicles Down for Most Brands

Healthy May sales cut into inventory as automakers kept a tight reign on supply, though some brands ended the month with excess units on the ground.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →

Mitsubishi Sets Growth Strategy, Structural Transformation

The Japanese automaker aims to 'strengthen products and technologies that embody its brand identity,' focus on its strongest markets and expand value-chain businesses 'that leverage its unique strengths.'

Read More →

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →

Mid-Atlantic Ford Store Has New Owner

A growing Maryland automotive group is only the 93-year-old dealership’s third owner after its longtime proprietors retired.

Read More →

Porsche Dealership Breaks Ground in Illinois

Barrington Porsche will be the new location for Murgado Automotive Group’s existing Porsche dealership currently in the Motor Werks of Barrington auto mall.

Read More →

Michigan Auto Group Acquires Ohio Rooftops

Feldman Automotive Group added two new brands, Honda and Toyota, to its portfolio with its latest acquisition of four Fireside dealerships in Ohio.

Read More →