Black Book Market Insights

Inventory levels continue to be tight, both in the new and used retail markets, as well as the wholesale market, further fueling the price required to source used inventory.

Inventory levels continue to be tight, both in the new and used retail markets, as well as the wholesale market, further fueling the price required to source used inventory.

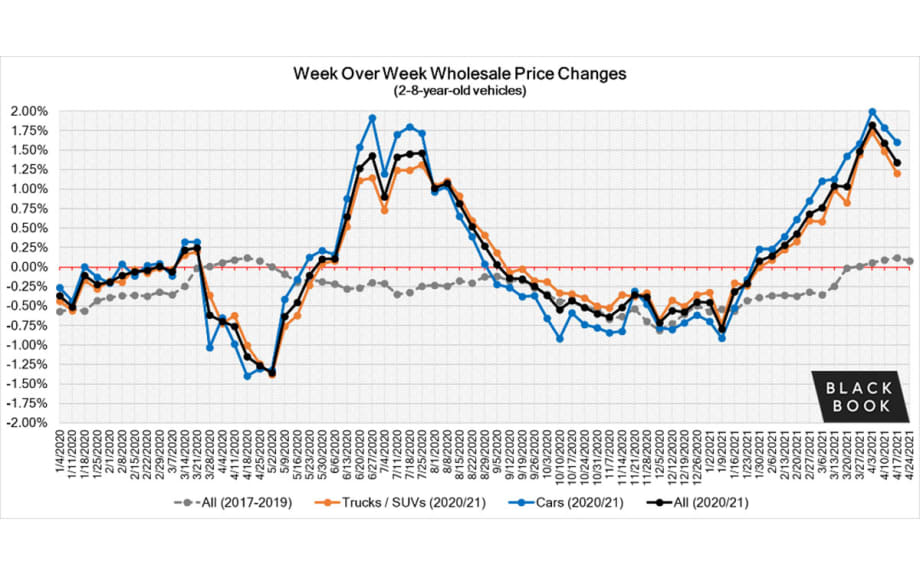

Wholesale Prices, Week Ending April 24th

Wholesale values continued their upward trend for a thirteenth week in a row. The level of weekly increases has slowed from the record set three weeks ago, but the level of increases is nonetheless impressive. Inventory levels continue to be tight, both in the new and used retail markets, as well as the wholesale market, further fueling the price required to source used inventory.

This Week Last Week 2017-2019 Average(Same Week)

Car segments +1.71% +1.60% +0.17%

Truck & SUV segments +1.07% +1.20% +0.02%

Market +1.28% +1.34% +0.08%

Car Segments

Car segments continued to have large gains this past week

(+1.71%), but the rate of increase grew compared to the week prior (+1.60%).

All nine Car segments had another week of gains exceeding +1%, with Compact (+2.33%) Cars exceeding 2% for the fourth week in a row.

Sub-Compact Cars (+1.88%) did not break the 2% mark this past week, but for the last 4 weeks has averaged a weekly increase rate of +1.98%.

Truck Segments

Truck segment gains continued this past week (+1.07%), but it

was at a lower level compared to the previous week (+1.20%).

All thirteen truck segments reported gains last week, with nine exceeding 1%.

Sub-Compact Crossovers led the Truck segment gains again this past week with an increase of +2.13%, compared with +2.14% from the previous week.

Full-Size Trucks (+1.25%) have slowed their rate of weekly gains but are still exceeding 1% each week.

Minivans are a niche segment, but have had strong growth each week, with the last four weeks averaging an increase of +1.96

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the price trends of newer used vehicles were experiencing larger weekly gains compared to the older units. Within the last three weeks, newer used units reached levels that, in some cases, exceed new car pricing while the rate of growth has slowed for older units. For example, in addition to F150 Raptor, 2020-21 Chevrolet Corvette, and 2021 Jeep Gladiator and Wrangler, dealers are paying above MSRP for 2021 Kia Telluride and Hyundai Palisade, as well as other mainstream models.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

This Week Last Week 2017-2019 Average(Same Week)

Car segments +1.54% +1.28% +0.17%

Truck & SUV segments +0.93% +0.98% +0.04%

Market +1.09% +1.07% +0.07%

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. 2021 will not have typical seasonality patterns as the market is going through a rapid increase in wholesale values. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Last week, we exceeded the increases that we saw last summer – wholesale prices are more than 20% higher compared to the beginning of the year (adjusted for the mix).

Retail (Used and New) Insights

Supply chain struggles continue to wreak havoc on new car production. Ford had another week with announcements of more production disruptions. However, they weren’t the only ones, Mitsubishi also said they will cut roughly 16,000 global units in May due to the shortage. Stellantis is laying off employees at their Jeep factory in Detroit as the chip shortage has production at a halt throughout the rest of April and lasting until the end of May.

Electrification is top of the list for most OEMs recently. Honda is now the latest manufacturer to release their timeline for electrification, with the goal being 40% of all sales to be EVs (and fuel cell vehicles) by 2030. Toyota also announced their plans for an EV subbrand with the all-electric crossover concept called the bZ4X being their first EV model. The crossover is just the beginning of their plans that will contain 15 electric models, one of which will be a pickup truck.

In more EV news, Cadillac announced that pricing for the 2023 LYRIQ, an all-electric crossover, will have a starting price under $60,000, including the destination charge.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded in January, retail prices seemed to lag wholesale prices – retail asking prices continued to decline throughout January and remained stable in February. March had an accelerated growth in retail prices, but the rate of growth is still lower compared to the increases of wholesale prices. In April, retail prices picked up speed as demand accelerated fueled by stimulus payments, tax season, and shortages of new inventory. Currently, the prices are more than 9% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles (similar to our wholesale price index).

Volume

Used Retail

Used retail listing volume stayed essentially flat since the beginning of the year but remains at levels above where the industry was in January, during the pre-COVID time of 2019.

Days-to-turn have been decreasing since the middle of March, as retail demand picks up across the country due to tax returns and the additional round of $1,400 stimulus checks deposited into consumers’ bank accounts.

Wholesale

The volume offered for sale each week has remained tight, but this past week there was a small improvement in the available volume, especially on the dealer lanes. However, conversion rates did drop slightly as sellers held firm to floors and buyers exhibited restraint on condition challenged units.

Condition of units is rising to the top of complaints for buyers as much of the available wholesale inventory in the market right now has some type of issue that needs to be addressed before it can be retailed.

With the ongoing new inventory shortage, the availability of used units is expected to remain tight throughout the summer, especially with rental and fleet companies holding their units in service longer until replacements are available.

More Showroom

Used Sales Hit Summer Drag

The vacation season, combined with high prices, has dented deliveries and added to inventories, though supply is still slim enough to keep listings elevated.

Read More →

California Launches EV Rebate Program

Participating automakers are matching the state's $13.5 million investment in new electric-vehicle rebates scheduled to take effect later this summer.

Read More →

OEM Poll Sees Industry Evolution

Kerrigan Advisors’ survey of automakers finds that tariffs, technology, network tightening and other factors are poised to reshape auto retail.

Read More →

The Trade-In Paradox

Retailing older cars with confidence in today’s market is a matter of establishing and following a clear process that can turn greater profit for auto dealers as they aim to meet used-unit hunger.

Read More →

Focus on Vehicle Cabins

The market for interior materials will grow in coming years as automakers look to meet consumer demand while staying competitive with changeups to sourcing and included features.

Read More →

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →

Used EVs Outpace New

While North American electric-vehicle sales remain down year-over-year, May sales saw a 3% increase from April’s numbers as used EVs led the market.

Read More →

New Vehicles Down for Most Brands

Healthy May sales cut into inventory as automakers kept a tight reign on supply, though some brands ended the month with excess units on the ground.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →