Smarter Choices Lead to Smarter Actions

When it comes to the buy-here, pay-here model, payment assurance technology definitely strengthens a dealer’s ability to keep customers current. But these devices are only part of the equation for a successful operation.

The costs associated with delinquencies and repossessions are well known to anyone trying to collect in the “C-” and below credit classes. However, if you don’t mind higher-than-necessary delinquencies and losing money, no need to read further.

The buy-here, pay-here (BHPH) and lease-here, pay-here (LHPH) models are all about collections, not vehicle sales. Over the years and through intense experience, one thing is for certain: We must understand the behaviors and habits of this customer segment in order to collect successfully. Anyone can sell, but collecting is an entirely separate issue.

Many dealers use lien holders or lessors, or use starter interrupts, locator systems or a combination of the two to strengthen their collections efforts. In some cases, these systems are used in place of good underwriting practices, which is not a recommended practice. These systems will perform well, but they are not magic bullets. If you agree, then keep on reading.

Understanding Payment Assurance Systems

Underwriting for ability and willingness is always recommended, just like selling vehicles that have a reasonable life expectancy and keeping payments in line with income. Payment assurance systems do work, but they shouldn’t take the place of good underwriting practices.

A recent trade publication indicated that fewer dealers utilized payment assurance systems in 2008 than in 2007. I find that impossible to accept. I currently sit on the board of the Payment Assurance Technology Association. Among our members, which include all of the major players in the segment, each one is experiencing increases in unit sales and in the number of active and new accounts.

But back to the issue at hand, payment assurance systems are vital tools when used properly. And these devices do empower dealers much like telephone and utilities companies are when it comes to delinquency. But the fact is the GPS-locator functions these devices tout are the least used feature. That’s because the location of the asset does not get the money in house, which is the primary goal when it comes to special finance.

Reducing Losses and Collections Staff

When it comes to special finance, it really does come down to behavior modification. Professionals in this arena say that if you don’t work to change your customer’s behavior, sometimes regularly, habits will not change.

That’s why two things need to happen in order to alter a special finance customer’s behavior. The first step is early detection and communication (reminding). The second step is intervention, which requires additional reminders, as well as consequences. Add these two steps together and you get prevention. And prevention equals profits for you.

In the collections arena, successful collections professionals practice this strategy everyday, because the results of preventing delinquencies and reducing charge-offs is worth the effort.

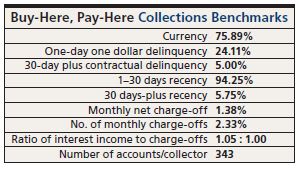

The folks doing benchmarks and static pools tell us that BHPH-level paper should be 72 to 75 percent current (see chart below). However, there are companies out there that are running over 90 percent current on “D” or below paper. Keeping customers current at levels like that means you can reduce collections staff by half or more.

[PAGEBREAK]

Early Warning Systems

So, if you are tired of the same old, same old, or your numbers are equal to the benchmark shown, read on. If not, thanks for your time and good selling. But if you are interested in further reducing losses and selling or financing more vehicles, then stay with me.

There are some pioneers and innovators in the payment assurance industry that have developed systems that not only help to modify behavior, but also increase the likelihood of collecting customer payments.

These proactive and preemptive communication systems employ automated text messages, e-mail, outgoing phone calls, and vehicle buzzers when situations escalate. Basically, these systems provide the early warnings to keep your customers current, and they do all the “heavy lifting” by handling all the communications when they’re not.

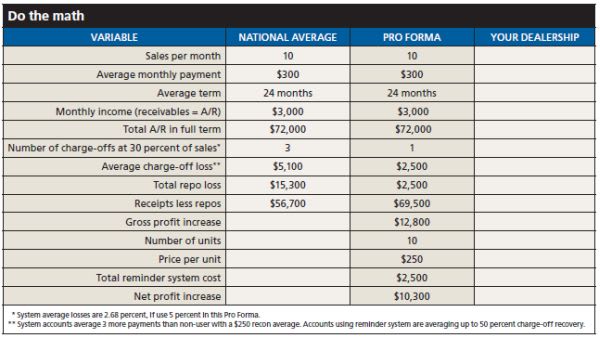

Users of these systems say they have increased their business by 20 percent. Some dealers even say these preemptive technologies have allowed them to go from 80 percent current to 92 to 97 percent current.

Payment assurance technology is definitely a key component to a special finance operation, but it’s only part of the equation. Remember, the key to special financing is making sure your customers are current on their payments, which is why a successful operation requires good underwriting practices and a preemptive communications system.

Ashley Herndon is a founding partner of the Irvine, Calif.-based payment assurance technology provider Crossbow Group Inc. E-mail him at aherndon@special-finance.com.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →