Trouble Ahead

Auto financial advisor returns to offer his take on what the recent weakness in stock market indices means to the economy, the industry, and dealer profitability.

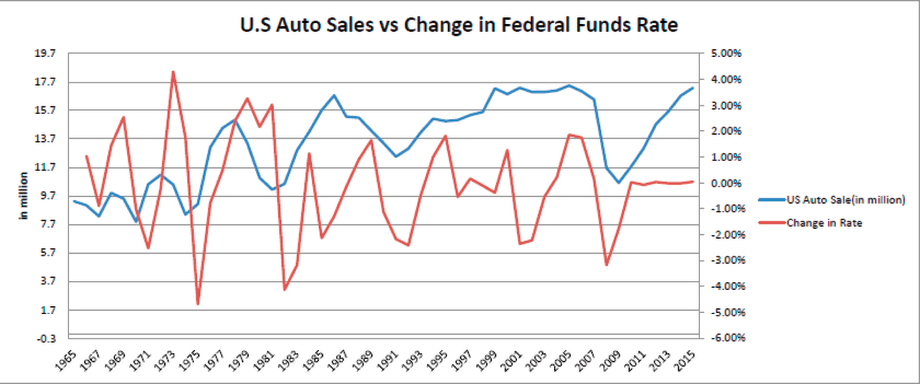

The current yield curve is pointing to interest rates rising over the next three to five years. For each 1% rise in interest rates, one would expect around a 4% drop in new-car sales.

Photo courtesy of iStock.

How long will the good times roll for the automotive industry and how severe will the next downturn be? That was the question I posed in a December 2014 article (“Predicting the Next Recession”) I penned for F&I and Showroom. That article detailed the profound effect economic cycles have on the industry and franchised dealerships. Well, a little more than a year later, the issues I raised in that article are starting to come to a head.

It is universally accepted that the stock market is a leading economic indicator, as it usually indicates where the economy is likely headed in advance of any actual change. Well, the recent weakness in stock market indices should raise some alarms, because when the economy gets a cold, the auto industry gets pneumonia.

Keep in mind we are six years and seven months into the current economic expansion, which officially began in July 2009. And according to the U.S. Bureau of Economic Analysis, only one expansion in the last 50 years lasted longer than eight years and one month. Hey, trees don’t grow to the sky and business cycles inevitably end.

History Check

In the last 50 years, each 1% decline in gross domestic product has resulted in an average decline of 9% in U.S. new-vehicle sales. The last recession’s decline in GDP was 3.4%, but the peak-to-trough decline in U.S. new-vehicle sales was nearly 40% from the more than 17 million units sold in 2007 to just 10 million units in 2010.

Now we’re looking at another year of at least 17.5 million in new-vehicle sales — a level we may exceed this year for the first time in the industry’s history. Keep in mind that during the prior six recessions, the peak-to-trough decline in new-vehicle sales ranged from 2.03% to 39.2%, and that the average decline over these six downturns was 18.8%.

Now, if new-car sales declined by 20% — a likely magnitude of decline during a normal economic downturn — one would expect dealer profits to decline by more than 20% due to the high level of fixed costs in the business. If earnings declined by 50% — which is also likely based on considerable historical precedent — and valuation multiples declined by perhaps 30%, the value of a dealership could decline precipitously [1 – (50% x 70%) = 65% decline] because of the compounding effect of a simultaneous decline in earnings and valuation multiples.

International Concerns

It is also important to understand that U.S. market indices reflect concerns about weakness in international markets. In a global economy, recessions in other markets inevitably impact our own. And right now, the entire world is justifiably concerned about China, the world’s second-largest economy.

China’s GDP growth ranged from 9% to 14% during the 2002–’11 timeframe — rates that were clearly not sustainable in the long run. At best, China’s growth will decline to a more sustainable level of perhaps 6% to 7%, which will impact its imports and international trading partners.

Another concern regarding China is the lack of transparency with respect to its financial disclosures. China’s leadership has very little experience managing an increasingly capitalistic economy, stock markets and the banking system, and there is scant evidence it is very good at it yet.

And the notion that amateurs manage the world’s second-largest economy, which is also the second-largest importer of autos, should be of concern to us all. Note that 14% of U.S. GDP is attributable to exports to our international trading partners — China being the largest importer of new, U.S.-built vehicles. The reason this matters to dealerships is it’s questionable whether Buick would have survived the Great Recession as a General Motors brand if not for China’s affinity for Buick products. In fact, out of the 1.2 million Buicks sold worldwide in 2015, the brand delivered one million units to China.

Our largest trading partner is Canada, which, according to the U.S. Census Bureau, accounts for nearly $260 billion in U.S. exports — of which 5.7% are automotive-related. Canada is a very energy-centric economy. When the energy business declines, Canada is hit especially hard. And the impact is likely to cut into U.S. auto sales there.

Our fourth largest trading partner is Japan, where policymakers just instituted negative interest rates because of a stagnant economy. And that’s after the country attempted to spur the economy by massively inflating the money supply over the last two years.

Gas Turmoil and Rising Rates

Then there are the oil and gas markets, which are in turmoil for one simple reason: The supply curve shifted up dramatically in the last 10 years. The United States, for instance, nearly doubled its production between 2010 and 2014. Although prices will eventually drift up for reasons beyond the scope of this article, it will not happen soon.

China’s economic issues could spell trouble for brands like General Motors’ Buick. Last year, the country accounted for one million of the 1.2 million Buicks sold worldwide.

This situation is causing serious economic problems for oil-producing states, with widespread layoffs and the impending demise of companies in that space. Keep in mind that several of the largest oil- and gas-producing states are also among the largest buyers of new cars — Texas being the largest.

Texas also has three of the 10 largest U.S. cities and has the second largest GDP of any state. The state is responsible for 1.58 million new cars sold annually, accounting for more than 9% of total U.S. new-vehicle sales. The third largest oil-producing state is California, which also has the largest state GDP. It’s also the No. 1 state for new-vehicle sales, with two million units sold annually.

Interest rates are another key driver of new-vehicle sales, as being able to offer below-market rates on finance and lease contracts is one of the most effective marketing tactics automakers have in their arsenal. And it goes without saying that the current yield curve is pointing to interest rates rising over the next three to five years, with short-term rates expected to trend up by at least 4%. For each 1% rise in interest rates, one would expect a negative impact on new-car sales of approximately 4%.

Not If, But When

As previously stated, trees don’t grow to the sky and never will. All economic cycles end, and the current one we’re in is clearly on its last legs. As a pundit for The Wall Street Journal recently stated, “Expansions don’t die of old age.” But it is puzzling why there has never been an expansion that lasted longer than 10 years and one month.

Problem is, seemingly small declines in GDP often lead to large declines in U.S. new-vehicle sales. In fact, it is normal for U.S. new-vehicle sales to decline by 19% during a downturn, with four of the last six recessions having led to sales declines in excess of 25%.

Faced with an imminent drop in U.S. new-car registrations, dealers should fortify their balance sheets and prepare for the downturn. They may even want to consider selling in tax-efficient transactions while earnings and valuation multiples are still robust.

J. Michael Issa, winner of two Middle Market Deal of the Year awards for M&A transactions, is a principal at GlassRatner Advisory & Capital Group LLC, where he serves as the automotive practice group leader. Email him at michael.issa@bobit.com.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →