Understanding why the performance of auto loan-based portfolios is improving even as the economy is contracting is the key to knowing when to package and sell your retail installment contracts.

by Nick Levenstein

July 1, 2009

4 min to read

I read with great interest Aaron Dalton’s “Singing the Big Apple Blues” (Dec. 2008, page 18), which discussed apprehensions common to the fund managers who ensure the flow of capital into the auto finance market. Like Mr. Dalton’s Tie Guy, many of the money people I’ve met with have raised the kind of objections that force me to defend the industry in general and myself in particular.

Such fears should be partially placated by a surprising improvement in auto loan portfolio performance in the past year. In working to form a new auto finance company, my associates and I researched the correlation between unemployment rates, investment inflows and defaults in asset-backed securities (ABS), as well as other consumer debt and portfolios of automotive retail installment contracts (RIC).

Ad Loading...

For data, we looked at the performance of ABS as rated by Standard & Poor’s from the year 2000, static-pool analysis of a portfolio of 5,000 RIC spread over Florida, Texas and the Midwest, unemployment data as published by the U.S. Department of Labor, and statistics on issuance of ABS domestically and globally as published by S&P and the Bank of England.

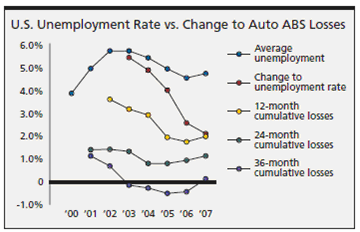

Our first set of data compares U.S. national unemployment rates and changes in the rates with defaults on ABS in the 12th, 24th and 36th months as traced by S&P:

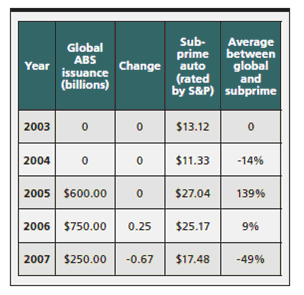

Other data of equal interest compared the same default rates for ABS issued against many categories of consumer loans including student loans, credit cards, home loans and other loans. You see rather wild fluctuations in the investment climate over the past five years:

If you graph out the default rates among different ages of ABS, there are definitely some changes. But take a look at the difference in capital flows over four years. We included the general data on all ABS issuance because subprime auto is a large and fragmented industry. It’s often difficult to determine how much of an effective proxy the rated ABS issued on Wall Street is:

We find that the general unemployment rate is highly correlated with ABS and RIC portfolio defaults in the first, second and third years. However, the rate of change of unemployment is correlated in the first two years and negatively correlated in the third year.

Ad Loading...

[PAGEBREAK]

This research helped us form a hypothesis as to why RIC defaults in the third year and changes in unemployment in the concurrent period were — to our surprise — negatively correlated. In examining the portfolio, we found the following to be true:

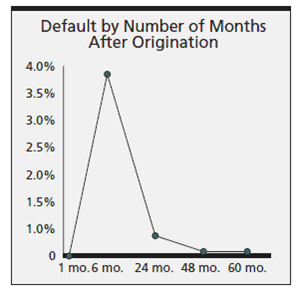

Rates of default in the portfolio peaked in the first six months and subsided afterward. In the third year, the rate of default is markedly less than the first two, and the age of the portfolio appears to be more statistically significant than the change in unemployment rates:

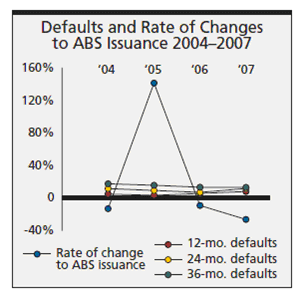

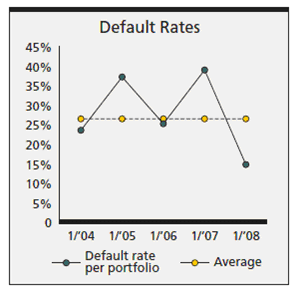

The part of the portfolio and ABS that were issued in years of a healthy investment climate — 2006, for example — were the worst performers:

The portfolio and ABS data confirm a strong negative correlation between healthy issuances of ABS and default in the period after the year or month of strong investor interest in ABS and portfolios of RIC in general:

Ad Loading...

In the third year, there is a positive correlation between ABS issuance, static pool losses and RIC default. There is a negative correlation between changes in unemployment and defaults in the third year, which is surprising. So, when unemployment rises, RIC aged three years default at a lower rate. LVC advances the theory that nonprime obligors understand that their choices to refinance are rather limited and behave more responsibly in an economic recession, even in an environment with declining employment opportunities.

What does all this mean for dealers? Well, to summarize our findings, times of strong capital investment in consumer-debt ABS are bad times to buy portfolios and RIC. The general

unemployment rate is strongly correlated with defaults on RIC in the first, second and third years. Changes in the unemployment rate also are correlated with RIC defaults, but are clearly less significant than other macroeconomic and microeconomic factors in the third year after the issuance of an ABS or origination of an RIC portfolio.

Many auto dealers and all finance company executives will have to meet the quintessential Tie Guy at some point. While nobody can predict the future for him, we can at least assure him that today is a much better time to buy our RIC portfolios than two years ago.

Nick Levenstein is the managing member of Mongoose Income Fund LLC, which is managed by San Francisco-based Levenstein, Vaceva & Co., and the former chief executive of Mongoose Capital Inc. He can be reached at nlevenstein@special-finance.com.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

It may be human nature to back off when a customer seems to say no to a product or service. But experts say F&I managers should operate as though the answer will be the opposite.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.