Things don’t always go smoothly in the daily grind of dealership life. That’s why a good paper trail is critical to keeping your store out of the crosshairs of hungry plaintiffs’ attorneys.

I once reviewed the deposition of a salesperson who was involved in a transaction that ended in a court case against a dealership. The plaintiff’s attorney was one of the sharper ones, and it was obvious by all of the other depositions in the case that he was targeting the credibility of the dealership’s employees.

Now, the salesperson who gave the deposition I looked at admitted he was no longer employed by the dealership. In fact, in a two-year span, he had held seven different jobs since leaving the store.

Ad Loading...

His one-month tenure as a salesperson didn’t help the dealership’s defense, either, nor did the fact that he had no previous automotive or sales experience prior to joining the dealership. Worse yet, it turned out he left the store to work at a taco stand.

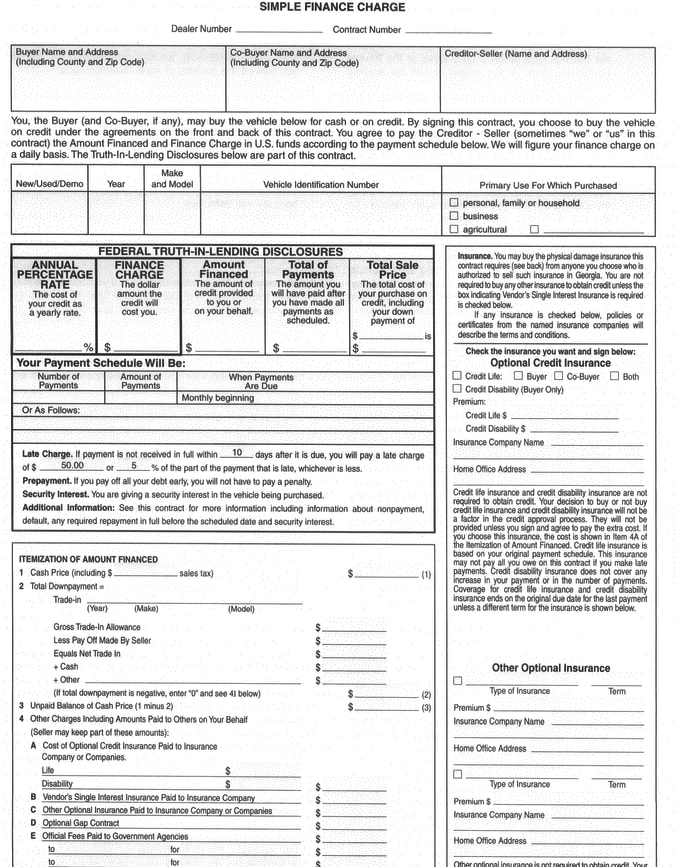

The really damaging part of his testimony, though, was the fact that the dealership did not have an F&I manager. It was up to the sales managers to close deals, but he was too busy to close the deal in question. The sales manager delegated the close to the inexperienced salesperson, who reviewed the Truth in Lending Act disclosures, the menu, and explained to the customer why he was signing 80 times.

To quote the movie Pretty Woman, "Big mistake. Big. Huge."

A Fighting Chance

Thankfully, this case never made it to trial. The dealer may have had a fighting chance if the deal file had a documented paper trail to demonstrate that the customer made informed choices at each step of the process. Of course, the dealer didn’t, and the Dark Side won.

Ad Loading...

A good paper trail takes care of the majority of potential compliance concerns arising out of a dealer’s variable processes. It documents the agreed-upon sales terms, demonstrates a consumer knew the payment walk, captures agreements to arbitrate differences, commits the customer to reps and warrants, and finalizes the financing or lease arrangements. That’s a mouthful, but it is intended to take the wind out of the Dark Side’s blowhard arguments.

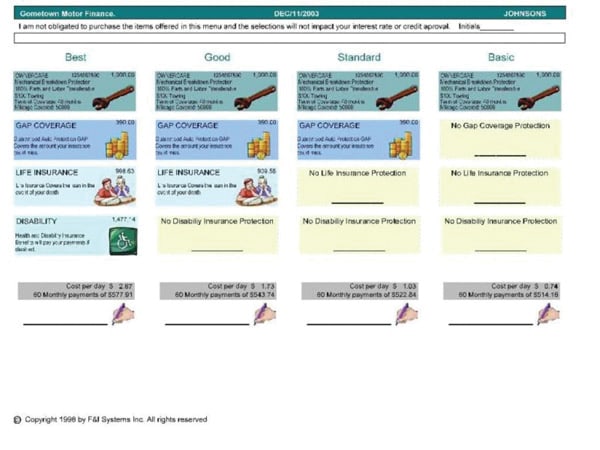

A paper trail consists of five documents in most states (California excluded), and starts with a final sales agreement — whether on a clear and concise web-based desking worksheet or a preliminary buyer’s order. That document should be followed by the final buyer’s order, the retail or lease agreement and, finally, the enrollment forms for all F&I products.

But remember, it is not just about having the forms; it is having the forms executed properly to support a transparent transaction. With that said, let’s review some general best practices for ensuring that the paper trail your process creates can defend challenges to the transaction.

1. The Numbers Have to Match:

Many of us in the industry lament the fact that a contract is not a contract. It would be so easy if we could just rely on the retail or lease agreement to support the transaction. Unfortunately, we don’t necessarily live in a logical world. If we did, men would be riding side saddle, not women.

Ad Loading...

Through a combination of greed, hungry plaintiffs’ attorneys, politicians disguised as attorneys general and pining for votes, and the Federales protecting the unaccountables, we’re well past the simpler days when a contract was a contract. We have to support it with ancillary documents and get a consumer to sign three or four times to prove they agreed to buy a certain product at a certain price. And in our paper trail, the agreement to purchase products and the price they paid must be the same on every document collected.

2. It’s About Time:

Not only do the documents have to match, it must be demonstrated that they were executed in the proper sequence. In other words, it does no good to have a menu timestamped three days after the date of the contract, because you leave yourself open to questions like, "If your process is to sell using a menu, why is the computer-generated timestamp three days after the contract?"

3. It’s Her Signature:

Unfortunately, consumers need to sign around 80 times on a standard deal to complete the transaction. That means our paper trail needs to have signatures in all 80 spots. If a document is not signed, or, heaven forbid, not signed by the customer, the paper trail starts to crumble.

Ad Loading...

4. It’s a Mulligan:

Dealers who spot-deliver vehicles will invariably have transactions that they guessed wrong on and cannot get a finance source to purchase as structured. In instances like that, the customer is called back in to sign again. This is currently a high-risk area for litigation and regulatory oversight, and the paper trail on these transactions must be perfect.

A recontract has to be viewed as a new transaction. As an expert witness, I want to be able to say the previous transaction is void so that any mistakes made in the prior transaction were corrected in the recontracted deal.

In those states where it’s permitted, a recontract should start with a rescission agreement or acknowledgement of rewrite. Collect the old docs from the customer and mark them "void." You also need to obtain the customer’s signatures by the void notation. It continues with a new menu, whether the base terms have changed or not. That should be followed by a new buyer’s or lease order, a new retail or lease agreement and, finally, new product enrollment forms.

Follow the paper trail to the Promised Land, and hopefully you can avoid the Dark Side’s inquiries. It can be a pain in the rear, but it’s well worth it in the end.

Ad Loading...

Gil Van Over is the president and founder of gvo3 & Associates, a national consulting firm that specializes in F&I and sales compliance. E-mail him at gvo@bobit.com.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

A TransUnion study found that relationship-driven sales models proved to be important, as consumers who used an agent had a lower shopping intensity than those going it alone.