Below-prime financing surpassed pre-recession levels in the second quarter. But is this trend dangerous for the future health of auto finance?

by Melinda Zabritski

October 10, 2012

4 min to read

It’s been almost four years since subprime mortgage sent the economy into a tailspin and soiled the reputation of all things not designated as "prime." Based on second-quarter auto finance data, below-prime auto finance is back — at least for now.

Experian Automotive’s second-quarter data showed that below-prime lending surpassed pre-recession levels, with the share of loans made to credit-challenged customers hitting 25.41 percent. That’s up 14 percent from the second quarter 2011 and nearly 2 percent above the frenzied peak reached in the second quarter 2007.

Ad Loading...

In that 2007 time period leading up to the crash, auto financing in the high-risk tiers was heating up. For the second quarters of 2007 and 2008, below-prime loan share was 24.96 percent and 24.49 percent, respectively. But by the second quarter 2009, as the credit markets tightened up, the segment’s share dropped to 17.57 percent.

The key factor is the car buyers themselves. They continue to make payments on time, driving second-quarter delinquency rates to historic lows and dropping the total dollar volume of at-risk loans as well. The repossession rate also enjoyed a year-over-year decrease.

Lessons Learned

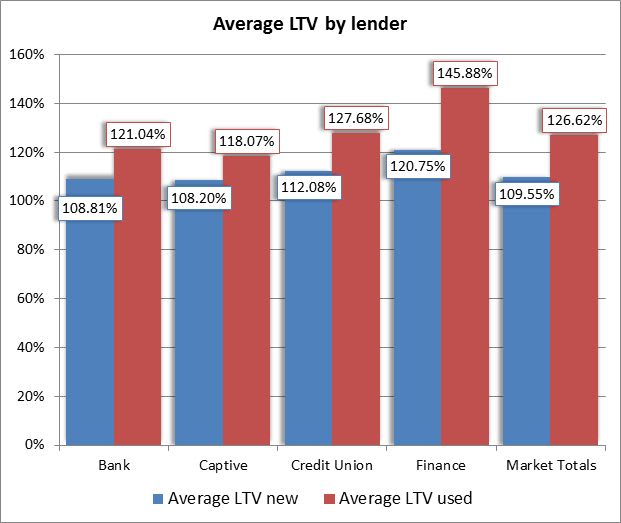

The return of subprime auto finance is great news for dealers and automakers, but finance sources aren’t necessarily throwing caution to the wind. In fact, lenders balanced the sharp rise in subprime lending during the quarter with lower loan-to-value (LTV) ratios. For new vehicles, the average LTV ratio was 109.55 percent, down from 115.65 percent in second quarter 2011.

This aggressive yet balanced approach means more customers are getting approved for car loans. For dealers, that means a larger pool of potential buyers. For the finance companies, keeping LTVs down should help mitigate any future losses.

Ad Loading...

[PAGEBREAK]

Credit Scores Fall Again

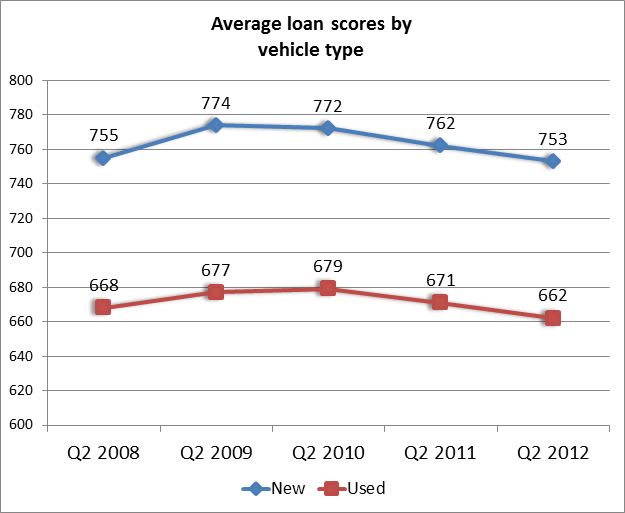

Consumer credit scores for new- and used-vehicle loans also fell in the second quarter, another sign that the appetite for risk is increasing among finance sources. The average credit score for new-vehicle loans originated during the quarter dropped nine points from the year-ago period to 753. In that same span, the average customer credit score for used-vehicle loans dropped nine points.

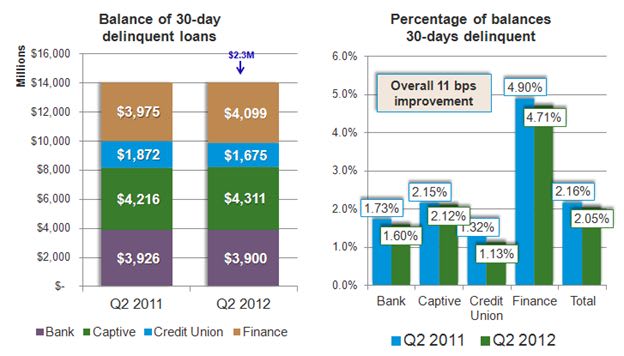

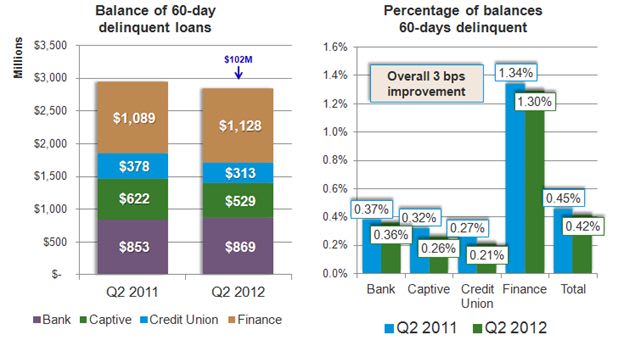

Once again, it’s responsible consumers who are driving this strategy. The 30-day delinquency rate fell from 2.59 percent in the second quarter 2011 to 2.52 percent. The 60-day delinquency rate also fell during the quarter, inching down from 0.6 percent from a year ago to 0.58 percent.

Further, there wasn’t a lending segment that didn’t realize a decrease in delinquency rates, with banks, captives, finance companies and credit unions all experiencing improved repayment patterns. The drop pushed down the total dollars of at-risk loans to $104.3 million.

Ad Loading...

The drop in vehicle repossessions was another sign of the industry’s improving health. That rate fell from 0.59 percent in the second quarter 2011 to 0.43 percent of all vehicle loans during the quarter, representing a 27.1 year-over-year drop.

Amount Financed Rises, Monthly Payments Flat

The second quarter also saw a rise in the average amount financed. For new vehicles, the average rose $474 from the second quarter 2011 to $25,714, while the average for used units jumped $370 from the year-ago period to $17,433.

Looking at monthly payments, the average remained relatively flat, rising just $4 from a year ago to $351 for used-vehicle loans. For new, the average monthly payment inched up by $2 from a year ago to $452.

While flat monthly payments can be caused by lower interest rates and longer loan terms, they also can be a sign that consumers are putting more money toward down payments. Higher down payments also help ensure lower LTVs, which, ultimately, is an important hedge against bad loans for lenders.

Ad Loading...

Total balances of loan portfolios also rose for all types of lending organizations in the second quarter, rising from $646 billion in the second quarter 2011 to $682 billion. Despite the growth, overall loan balances still lag behind pre-recession levels. In the second quarter 2007, outstanding loan balances reached $701 billion.

What to Expect

The automotive industry continues to claw its way back to health. Because auto lending and auto sales have such a symbiotic relationship, these are clearly better times for lenders. With delinquencies down, lenders are finding more breathing room to take calculated risks. They continue to exhibit restraint with lower LTVs, which is a positive sign that they are not giving into the euphoria of an improved market.

As we move forward in the coming months, it will be important to watch delinquencies and LTVs closely. If both of these key indicators remain relatively low, the automotive lending industry will continue to find improved portfolios and overall health. As always, this is good for both retailers and their customers.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

A TransUnion study found that relationship-driven sales models proved to be important, as consumers who used an agent had a lower shopping intensity than those going it alone.