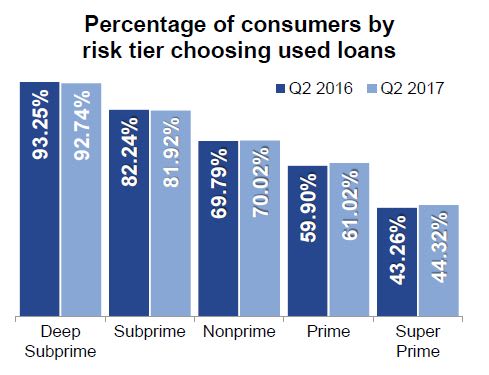

SCHAUMBURG, Ill. — Car buyers with prime and superprime credit shifted toward used in greater numbers, with used-vehicle loans for both low-risk tiers reaching record highs in the second quarter, according to Experian Automotive.

According to the firm, a record 61.02% of prime consumers chose used vehicle loans, up 1.12 percentage points from a year ago. In the superprime category, a record 44.32% of superprime customers took out used-vehicle loans, 1.06 percentage points higher than a year ago. The shift comes as new-vehicle loan payment reached a record $504, about a $139 difference from the average used-vehicle loan payment.

"One of the trends that we've consistently seen is all-time highs and record-highs of prime-plus consumers who are choosing a used vehicle," said Melinda Zabritski, senior director of financial solutions at Experian Automotive, adding that the gulf between payment amounts has played a major role in the new-to-used shift.

The used-vehicle market, however, wasn’t the only solution for car buyers seeking payment relief. Loan terms, which continued to stretch during the period, were also a go-to option in the second quarter.

According to Experian, the 61- to 72-month term band did lead the way in the second quarter, accounting for 40.4% of all new-vehicle loans. However, the 73- to 84-month and 85- to 96-month bands showed the largest growth.

The share of loans in the 73- to 84-month range increased 1.22 percentage points from a year ago to 32.5%, while the 85- to 96-month band increased 0.3 percentage points to 32.5%. Zabritski noted that a majority of loans in the latter range were primarily clustered around 85 months.

Also reaching a new record was the balance of outstanding loans, which increased from $1.027 trillion in the year-ago quarter to a new high of $1.1 trillion. The new high was achieved as delinquencies, which have caused a slight tightening in underwriting standards in recent quarters, showed some improvement.

According to Experian Automotive, the 30-day delinquency rate inched down 0.02 percentage points to 2.2%, while the 60-day rate increased slightly by 0.05 percentage points to 0.67%.

The improvement in delinquencies didn’t translate into a loosening of credit standards, however, with the share of subprime lending in the second quarter dropping from 21.46% in the year-ago quarter to a near-record low of 20.57%. Deep subprime also showed no improvement, falling 0.08 of a percentage point to a near low of 3.98%.

"The last time deep subprime was below 4% for a Q2 period was way back in 2012, and it was 3.77%," Zabritski noted. "The all-time Q2 low was seen back in 2011. It was about 3.64%, but, again, we're still near historic lows for deep subprime in the total loan market."