Consumers Prioritize Affordability as Loan Amounts Increase

Wary of unmanageable monthly payments, the American car buyer’s attention is increasingly shifting toward used vehicles, leases, and longer terms as the cost to buy a new car or truck continues to climb.

Concerns over soaring MSRPs and monthly payments continue to drive buyers of every credit tier out of the new vehicle market.

Photo ©GettyImages.com/Ridofranz

With increasing average vehicle loan amounts in the automotive finance market, consumers are looking for manageable options that will save them money.

The automotive loan market continued to grow at a steady pace, according to Experian’s Q2 2019 State of the Automotive Finance Market report. Loan balances reached $1.197 billion in Q2 2019, an increase of 4.2% year-over-year. At the same time, delinquency rates remained relatively flat.

Loan amounts for both used and new vehicles increased in the second quarter. Used loan amounts reached a record high of $20,156, a $448 year-over-year increase. For new vehicles, the average loan reached $32,119, a $1,161 increase.

Read: Average New Vehicle Prices Up Nearly 3% in October

These trends are driving consumers to look for more manageable options for their monthly payments. Data from Q2 lends critical insights behind the popularity of used cars, leasing vehicles, and financing with longer term loans as a method to lower monthly payments for consumers.

Used Car Market Contracts Upward Trend

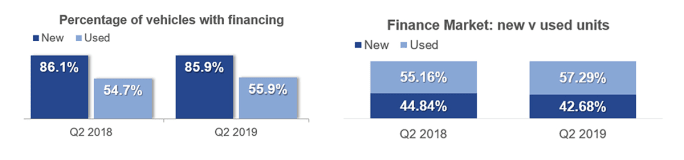

Used cars are the “new” hot item. Q2 saw increases in the percentage of used vehicles with financing — up 1.2 percentage points year-over-year. Those opening new loans also shifted further in favor of used cars, growing from 55.16% of the finance market in 2018 to 57.29% in 2019.

Another sign that consumers are prioritizing more affordable monthly payments is the record high number of prime and superprime consumers financing used vehicles.

Traditionally, consumers with higher credit scores lean toward new vehicles. However, superprime borrowers with vehicle loans chose used vehicles 45.95% of the time in Q2 2019, up from 43.65% in Q2 2018; prime consumers with vehicle loans chose used vehicles 62.47% of the time.

Overall, prime and superprime consumers financed used vehicles 57.2% of the time, a new record high.

There are numerous factors impacting the shift to used, one of them being the higher availability of pre-owned late-model vehicles. New vehicle leasing has hovered around 30% for the last three or so years, and as these vehicles come off-lease, they are often shifted to the used side of the dealership.

With low mileage and similar features — and often extended warranties available — opting for these vehicles can be a great way to get the vehicle desired at a more affordable price.

Consumers Investigate Leasing as a More Manageable Option

Leasing is another option some consumers are pursuing to achieve lower monthly payments. Compared to loans, average monthly lease payments are lower on many of the top leased models.

The largest payment difference can be found in the full-size pickup category ($189 less per month to lease versus a loan). CUVs comprise the majority of the top lease models and are also on average $92 less expensive per month to lease instead of taking out a loan.

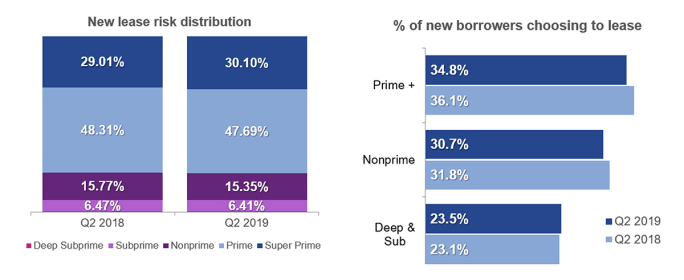

Cumulatively, leasing still comprised more than 30% of the market. In Q2, prime and superprime consumers continued to dominate the lease market; the two credit segments combined represent 77.79% of the market.

However, the overall number of prime and superprime consumers choosing to lease vehicles dropped from 36.1% in Q2 2018 to 34.8% in Q2 2019.

Loan Terms Are on the Rise

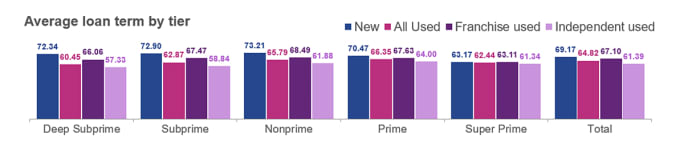

Across all loan and risk types, average loan terms reached new highs in Q2 2019. Average new vehicle loans reached a new high of 69.17 months, while used vehicle loans reached 64.82 months.

The most common loan term is 72 months, though the number of loan terms over 85 months also increased slightly. Consumers are opting for these longer-term loans to distribute the cost over a longer period of time.

30-Day Delinquencies Decrease Slightly While 60-Days Remain Stable

The increase in average loan amounts has left the industry questioning whether consumers will be able to handle the higher costs of a vehicle. Delinquencies can be a telling sign of this, and in Q2, the story is a positive one.

Q2 saw 30-day delinquency rates decrease for most lenders. Banks decreased from 1.88% to 1.84%; captive auto went from 2.15% to 2.07%; and credit unions were down from 1.19% to 1.14%. Overall, Q2 2019 30-day delinquency rates were at 2.11%, down from 2.12% in Q2 2018.

Unlike other sources, finance companies did see an increase in 30-day delinquency rates to 3.85% — a 0.18% increase from Q2 2018.

Finance companies, which tend to take on more subprime and deep subprime borrowers than other sources, saw 30-day delinquency rates climb to 3.85% in the second quarter.

Photo ©GettyImages.com/allanswart

Sixty-day delinquency rates increased from 0.64% in Q2 2018 to 0.65% in Q2 2019. This increase is primarily due to finance companies, which saw a 0.08 percentage point increase on 60-day delinquency rates, up to 1.40%. In fact, captive and credit unions both experienced a 0.01 percentage point decrease in delinquency rates from Q2 2018. Banks remained stable at 0.64%.

Finance companies saw larger increases in both 30-day and 60-day delinquency rates compared to other sources. This is likely because finance companies typically cater to a higher percentage of subprime and deep subprime customers.

New Credit Scores Continue Five-Year Rise

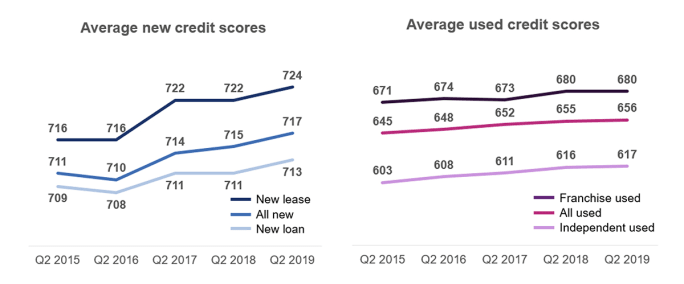

In Q2 2019, the average credit scores (based on VantageScore 3.0 calculations) for new vehicle loans and leases showed steady growth, up two points to 717.

New lease scores were up two points to 724 and new loan scores were up two points to 713. This data shows the upward movement of credit scores for new vehicles, increasing six points from Q2 2015 to Q2 2019.

Meanwhile, average credit scores for used vehicle loans also saw slight increases in Q2 2019. For independent dealers, credit scores for used vehicle loans went up one point to 617, while credit scores for all used vehicle loans rose by one point to 656. Franchise used remained flat YOY staying at a score of 680. With rising credit scores, consumers will be able to pursue additional lending options that may offer more affordable monthly rates.

Q2 Data Highlights Steady Trends in the Auto Finance Market

The overall theme of Q2 2019 automotive finance market was consistency, with steady growth and low delinquencies.

As vehicle prices continue to rise, consumers are focusing on affordability when choosing vehicles. Whether it is through extending loan terms or choosing a used vehicle over new, car buyers are looking for options to offset monthly payments, which continue to rise across multiple finance types.

Credit scores are one of the major factors taken into consideration by lenders when offering loan rates and terms. As such, consumers should make use of all available tools to improve their credit standing, increase their scores, and potentially secure better rates or terms.

As the auto finance market continues to evolve, dealers, manufacturers and finance sources should monitor vehicle affordability and delinquencies. Understanding these trends can help dealers and lenders ensure they have the right options available for consumers and help keep the market moving forward at a steady pace.

Melinda Zabritski serves as senior director of automotive financial solutions for Experian Automotive. Email her at melinda.zabritski@bobit.com.

Read: Rising Loan Amounts Drive Consumers to the Used-Vehicle Market

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →