Pressure Cooker

The industry might be hitting lows not seen for decades, but dealers and providers say they aren’t changing their goals when it comes to acceptance rates for F&I products.

Results from F&I magazine's January survey of products performance.

In Youngstown, Ohio, where the unemployment rate stood at 9.7 percent in April, dealing with an economic downturn is nothing new to Davey Jones. In fact, it’s one of the reasons why his acceptance rate for service contracts at his Ford dealership is up three points from last year.

“We say we’ve been in a recession for 30 years, and everybody is just catching up,” said the 15-year F&I veteran, whose former steel town is still feeling the effects from the plant closures of the 1970s. “We’re used to selling under these circumstances.”

The biggest challenge for Mark Fedenis, a 20-year F&I veteran, isn’t securing back-end advances; it’s the front-end advances that are giving his Roseville, Mich.-based Jeffrey Automotive Group problems. “It’s been a struggle,” he said, adding that his lenders are requiring down payments of $1,000 down more for each used-car deal, even on customers with 740 credit scores.

Even the white-collar town of Boulder, Colo., isn’t

immune to the economic downturn. “Volume continues to drop, but finance gross

continues to increase, so we’re doing more with less,” said F&I Director

Justin Gasman, whose Chevrolet and Honda dealerships have lost approximately

100 sales per month since the recession struck his town.

For Jim Melson, business manager at a Grand Haven,

Mich.-based used-car dealership, the current credit crisis is a big bank

problem, not a lending-wide problem. “Everything from GAP to life is

significantly off,” he said. “The primary reason is the change with what the

banks are allowing us to do.”

With penetration levels of vehicle service contracts falling

to levels not seen since the 2002 NADA DATA report — dropping from 31 percent

in 2007 to 28.4 percent for the first two months of the year — it’s clear the

economic climate is challenging even the most seasoned F&I veteran. And

while lender guidelines are in constant flux these days, much like consumer

confidence, there is one commonality: The job of the F&I manager is more

crucial than ever before.

“There’s actually more pressure on the F&I office to

maximize profits on each deal because of the fact that front-end profits are

falling due to competition, how slow the economy is, and how slow demand is,”

said Jesse Toprak, executive director of industry analysis for Edmunds.com.

Survey Says

F&I magazine took its own peek into the current challenges by surveying F&I managers across the country in January, the same month vehicle sales hit a 26-year low. Four of the business managers surveyed were Jones, Fedenis, Gasman and Melson. And with the exception of Gasman, the three other F&I managers work in states touting some of the highest unemployment rates in the country.

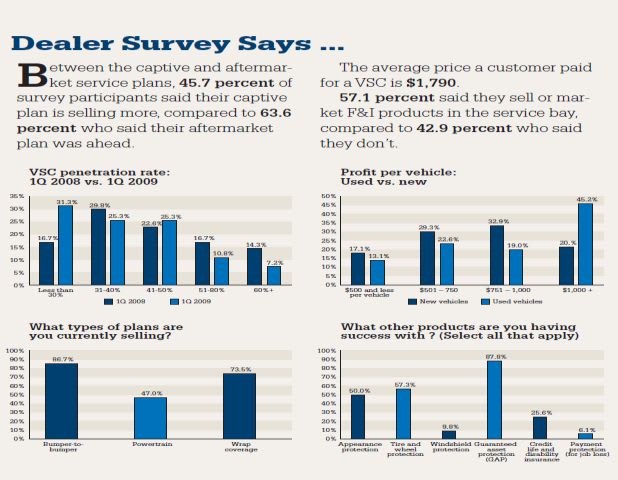

Looking at acceptance rates for service contracts, the percentage range with the highest growth from the first quarter 2008 to the same period in 2009 was the less-than 30 percent range, which jumped from 16.7 percent of respondents to 31.3 percent. The only other range to grow during that measurement period was the 41 to 50 percent range, which increased from 22.6 percent of respondents to 25.3 percent.

As for what plans are selling, 86.7 percent of respondents said bumper-to-bumper, followed by wrap coverage at 73.5 percent and powertrain at 47 percent. As for terms, five-year, 100,000-mile plans were the most popular at 34.1 percent, followed by plans greater than six years and 72,000 miles at 31.7 percent. The average price paid by customers for a service contract was $1,790.

[PAGEBREAK]

“It’s reassuring that service contracts are still holding strong despite the automobile crisis,” Bill Speaks, CEO of NAC, said of the survey results. “Although it’s proved to be difficult times, it’s brought the focus back to the basics that many companies were founded on.”

At his Chevrolet and Honda stores in Colorado, Gasman’s penetration rate on service contracts stood at nearly 30 percent, but he’s also making $850 per contract sold. And while that amount is on par with last year, he said he won’t hesitate to discount the price.

“I’d rather make $200 or $300 than a goose egg,” Gasman said. “When things slow down, you kind of have to adjust your selling a bit. People are just a little bit more leery about spending money, and they are a little bit more conscious about what they’re doing with the few dollars they have left.”

At his Ford dealership, Jones is running at a 41 percent clip on service contracts. However, he said he’s averaging about $195 less per contract than his $795 target, a problem he attributes to the unwillingness of the larger banks to finance customers with blemished credit histories.

“It’s the major players that are giving us trouble with that,” he said. “You’ll get a typical cap on the back-end — only $500 allowed or none at all.”

Market Dynamics Keep Dealers Guessing

One of the most closely watched reports among economists is the Federal Reserve Board’s Senior Loan Officer Opinion Survey on Banking Practices, which has served as a barometer for lending since the credit crisis hit critical levels in the third quarter 2008.

In its October report, the Federal Reserve Board (FRB) pointed out that more than half of domestic banks indicated they had become either somewhat or much less willing to make consumer installment loans. That percentage dropped to 15 percent in January and 5 percent in April. However, the FRB made clear the credit crisis was a big-bank crisis, not a bank-wide crisis, a sentiment echoed by those on the frontlines.

“We seem to be back-end capped way more frequently than we

were six months ago,” said Melson, the used-car finance manager from Grand

Haven, Mich. “For the most part, the big banks aren’t buying well anymore.”

Melson, like many dealers these days, turned to his local credit unions for help, a lending segment often viewed as an adversary to F&I managers. In fact, two of his most active finance sources are credit unions he cultivated relationships with in the last six or seven months.

As for performance, Melson said his acceptance rates for warranties and GAP stood around 45 percent and 60 percent, respectively, an achievement he attributes to the addition of Service Payment Plan to his arsenal. The only problem is he’s averaging $350 less per warranty.

[PAGEBREAK]

Tony Dupaquier, F&I trainer for American Financial and Automotive Services Inc. (AFAS), doesn’t disagree that lenders are capping advances, but he’s not so sure the caps are directed at the back-end. It’s something he talked about at the 2009 NADA Convention and Expo during his “The Lost Art of the Business Manager … A Credit Score Is Not F&I” workshop. And it’s something he’s been preaching ever since.

“When lenders reduce funding on the front-end sale, they’re not necessarily limiting the back-end. If the deal is structured right, financing is available,” he said. “It all comes down to the skills and training of the F&I manager. And what pains me on a daily basis is how dealers are reducing training expenses in an effort to save money.”

Goals Unchanged, Just Less Customers

Most F&I product providers said target penetration rates haven’t changed despite the economic downturn, but admit fewer touches means less products moved. However, any success a dealer is having these days, many said, is due to the burgeoning used-vehicle market.

“It’s tough for all of us. We feel it like everyone else,” noted Steve Amos, president of F&I product provider GSFSGroup, who said penetration rates are up 10 percent this year. “But what’s helped are used-car sales. What we’ve lost in new cars right now, we’re coming close to making up for with the used-car business.”

That’s been the case for Jeffrey Automotive Group’s Fedenis, who’s seen his penetration rate on GAP rise 10 points to 50 percent this year. Even credit life and disability has seen an uptick, he said. “We have a higher percentage of service contracts and GAP on off-lease vehicles … Our back-end average is $400 higher than retail vehicles,” he said.

Providers warn, however, that the one product that could suffer under the current lending market is GAP, especially as vehicle values continue to decline and lenders continue to increase requirements for down payment. “That’s one of the products affected by down payment,” said GSFS’ Amos.

According to the magazine’s dealer survey, the top three products aside from service contracts were GAP (87.8 percent), tire-and-wheel protection (57.3 percent), and appearance protection (50 percent). As for what lenders are advancing on, the top three products among respondents were GAP (96.3 percent), credit life and disability (64.2 percent) and tire-and-wheel protection (42 percent).

Despite the crisis, AFAS’s Dupaquier believes dealers should maintain acceptance rates of 50 percent on service contracts and 60 percent on GAP. As for high-line dealers such as Lexus stores, he said those dealers should be running at a 70 percent clip on ancillary products such as key replacement and appearance protection. Dealers with high truck sales, he added, should be around 20 percent penetration for tire-and-wheel and key replacement.

[PAGEBREAK]

Alan Miller, a senior executive with CNA National Warranty Corporation, said acceptance rates among the company’s dealers are off from last year, but said the company’s ability to add to its dealer base has kept his company performing above the overall drop in the market. Another key has been the company’s service-contract pay plans, which he said has increased in usage by 10 to 15 percent among the company’s dealers.

Resource Automotive’s Mark Mishler said the company is also holding its own, as penetration levels for all of its products stood in the mid to high 30s. Regionally, he said the West Coast is down only slightly. However, even in places like Florida, where retail sales have been hit hardest, penetration levels are holding firm. But like his competitors and even dealers, the hope now is for the credit markets to turn the corner.

“The last quarter of last year was the real downfall of our business from the standpoint of retail sales and F&I products, but on a year-over-year basis, we’re running at about the same penetration levels,” said Mishler, who pointed to expansion of the Troubled Asset Relief Program and further securitization of loans with lenders as the keys for the rest of the year. “If that happens, it’ll change what’s going on out there.”

Whether that happens or not, veteran F&I managers like Jones said they’ll just keep plugging away. “Hey, we think it’s going to be a good year,” he said.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →