Black Book: Market Insights Report

Black Book recently published an update to their weekly Market Insights report.

Black Book recently published an update to their weekly Market Insights report.

Wholesale Prices

Wholesale prices continued their decline last week for the nineteenth week in a row. Volume-weighted, overall Car and Truck segments both experienced continued softening in values last week, with the rate of decline decreasing compared to recent weeks.

This Week Last Week Historical Average

Car segments -0.52% -0.91% -0.62%

Truck & SUV segments -0.20% -0.74% -0.52%

Market -0.31% -0.80% -0.62%

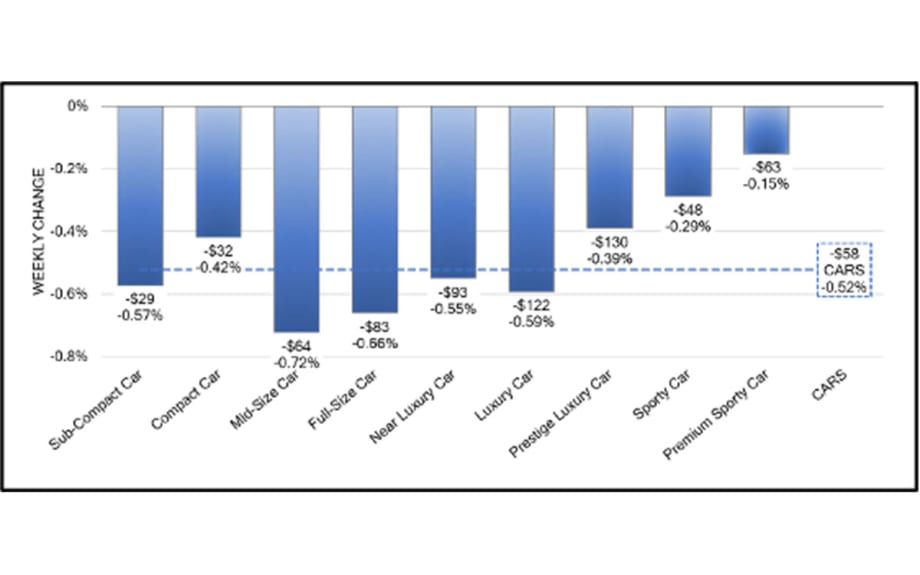

Car Segments

The Near Luxury and Luxury Car segments saw steeper declines in prices this past week as available supply increased on the lanes and remarketers lowered their floors. However, volume remains low in the Premium Sporty and Prestige Luxury Car segments which is continuing to see lower than normal weekly changes.

The smaller Car segments, Sub-Compact and Compact, have been on a race to the bottom over the last several weeks, but this past week the Compact Car segment experienced the lowest weekly change for this segment since the week of Thanksgiving.

Truck Segments

The Compact Crossover segment saw a drastic decline in the rate of depreciation at only –0.34%, compared to –1.45% the week prior.

Full-Size Crossover supply remains tight, and with low fuel prices the demand has remained strong. This was the second week in a row of an increase in values.

Full-Size Trucks continue to see softening in values in the 1500 level trucks, but the 2500 and 3500 level trucks remain strong and the overall segment only saw a -0.20% change this past week.

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. The question still remains whether we will go back to normal seasonality in 2021.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down leading up to the December holidays, and thus resulted in declining retail asking prices over the last several weeks. Retail prices are typically slower to react to changes in the market, and are not reflecting the recent uptick in consumer demand seen in the last two weeks.

Days-to-turn have been increasing since November but remain at levels below average. Recent increases in retail demand are expected to keep the days-to-turn below average in Q1.

Volume

Used Retail

Used retail listing volume stayed essentially flat since the beginning of 2020 but remained at levels above where the industry was in January, during the pre-COVID time of 2019.

Wholesale

Over the last several weeks of 2020 we saw wholesale sold volume decrease as dealers need for inventory declined as a result of weaker used retail demand. As has been the case, the drops in volume were not uniform across all auctions and platforms.

In the first full week of 2021, the average conversion rate at auctions improved. This is mainly due to stronger retail demand to finish out 2020, which resulted in dealers needing to return to the lanes to secure inventory. The improvement trend continued last week, with another increase in the success rate, particularly driven by the increase in activity at auctions in the southern states.

Black Book’s Market Insights

Retail (Used and New)

The majority of dealers are reporting a stronger than usual start to their January sales, both new and used. They are also optimistic about the potential for another round of stimulus and the increased demand they expect it will bring to their business.

The global microchip shortage is continuing to ripple through the automotive industry with more OEMs in the news recently for the impacts it is having on them. For example, Volkswagen had already pulled back on production of the Golf, but now other models being produced at their Wolfsburg plant in Germany are reducing production. Honda, Subaru, and more are taking similar actions because of the shortage.

Carmax announced this week changes to their policies. They have increased their money back guarantee from 7-days to 30-days and now offer a 24-hour test drive period.

Wholesale

Sales rates increased this week, as parts of the country are seeing an uptick in retail demand and as dealers prepare for a potential additional round of stimulus money.

Inventory levels have been climbing for the past two weeks with some auctions seeing levels nearing pre-COVID.

Uncertainty remains around the future of a traditional spring/tax season market this year. Early sentiments by dealers are optimistic and auction performance of the traditional spring market vehicles, those under $12,000, have seen an uptick in demand in the last two weeks.

KAR Global, parent company of ADESA, announced this week that they will remain 100% digital. This was already part of their plan for the future, but COVID has sped up their conversion to all digital after seeing how well buyers and sellers have adapted.

More Showroom

California Hybrids Reach State Record

The Golden State still leads the country in electric-vehicle registrations, but much like the rest of the U.S. its hybrid market share is up while full electrics stabilize after a dramatic first-quarter dip.

Read More →

My Mercedes in the U.S.

The German brand debuted its studio dealership concept for the first time in the states in Los Angeles, tapping Americans’ penchant for creative distinctions.

Read More →

Used Sales Hit Summer Drag

The vacation season, combined with high prices, has dented deliveries and added to inventories, though supply is still slim enough to keep listings elevated.

Read More →

California Launches EV Rebate Program

Participating automakers are matching the state's $13.5 million investment in new electric-vehicle rebates scheduled to take effect later this summer.

Read More →

OEM Poll Sees Industry Evolution

Kerrigan Advisors’ survey of automakers finds that tariffs, technology, network tightening and other factors are poised to reshape auto retail.

Read More →

The Trade-In Paradox

Retailing older cars with confidence in today’s market is a matter of establishing and following a clear process that can turn greater profit for auto dealers as they aim to meet used-unit hunger.

Read More →

Focus on Vehicle Cabins

The market for interior materials will grow in coming years as automakers look to meet consumer demand while staying competitive with changeups to sourcing and included features.

Read More →

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →

Used EVs Outpace New

While North American electric-vehicle sales remain down year-over-year, May sales saw a 3% increase from April’s numbers as used EVs led the market.

Read More →