J.D. Power, LMC: Replacement Demand Driving Up New-Vehicle Selling Rate in April

Based on the new-vehicle selling rate, J.D. Power and Associates says the industry is on pace to retail 15.4 million units this year. LMC’s forecast remains at 15.9 million units for 2013.

WESTLAKE VILLAGE, Calif. — The new-vehicle retail sales pace in April remains in a healthy holding pattern as buyers continue to replace aging vehicles, according to a monthly sales forecast developed by J.D. Power and Associates’ Power Information Network (PIN) and LMC Automotive.

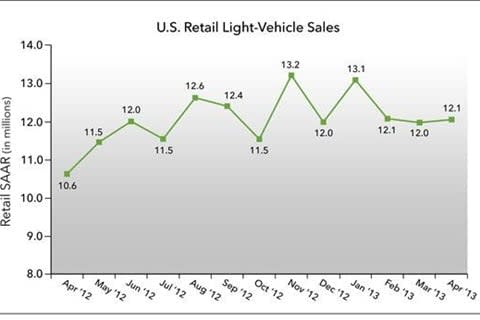

New-vehicle retail sales in April are projected to come in at 1.029 million vehicles, which represent a seasonally adjusted annualized rate (SAAR) of 12.1 million units and keeps the rate stable at or above 12 million units for a third consecutive month.

U.S. Retail SAAR—April 2012 to April 2013

(in millions of units)

According to J.D. Power and Associates’ PIN data, strong sales are being complemented by increasing prices. When comparing year-to-date data for 2013 with the same period last year, consumer-facing transaction prices are up 3.1 percent, which equates to an extra $13.2 billion spent on new vehicles through the first four months of the year ($113 billion in total). The average price of used vehicles sold at franchised dealerships has also risen 3.8 percent in 2013 (YTD) from 2012 (YTD).

“The strong used-vehicle prices we’re seeing are supporting new-vehicle demand and are reflective of the general pricing discipline being exhibited by new-vehicle manufacturers,” said John Humphrey, senior vice president of the global automotive practice at J.D. Power and Associates. “Industry sales are also benefiting from an increase in the number of maturing vehicle leases, a trend that will continue throughout 2013.”

PIN forecasts that overall lease maturities will rise by 447,000 leases (+35 percent) to a total of 1.73 million maturities for the full year of 2013, compared with 2012.

Total light-vehicle sales in April 2013 are projected to reach 1.312 million units, a 7 percent increase from April 2012. The selling rate is expected to remain above 15 million units for the sixth consecutive month. The forecast for fleet sales is 282,000 units, which is slightly stronger than in April 2012, representing a 22 percent share of total sales.

J.D. Power and LMC Automotive U.S. Sales and SAAR Comparisons

April 20131 | March 2013 | April 2012 | |

New-Vehicle Retail Sales | 1,029,000 units2 (9% higher than April 2012) | 1,148,338 units | 908,685 units |

Total Vehicle Sales | 1,312,100 units (7% higher than April 2012) | 1,452,325 units | 1,182,874 units |

Retail SAAR | 12.1 million units | 12.0 million units | 10.6 million units |

Total SAAR | 15.2 million units | 15.2 million units | 14.1 million units |

1Figures cited for April 2013 are forecasted based on the first 11 selling days of the month.

2The percentage change is adjusted based on the number of selling days in the month (25 days in April 2013 vs. 24 days in April 2012).

The outlook for vehicle sales in 2013 continues to improve. LMC Automotive is raising its 2013 U.S. forecast for total light-vehicle sales to 15.4 million units from 15.3 million units. The retail light-vehicle forecast continues to round to 12.5 million units, although the majority of the increase in the forecast is on the retail side of the market.

“The irrepressible buying behavior of consumers is driving auto sales growth in 2013, as consumer spending remains remarkably stronger than the economy suggests it should be,” said Jeff Schuster, senior vice president of forecasting at LMC Automotive. “If the current favorable trend in the stock markets and housing continues throughout the year, the automotive market may be poised for a breakthrough performance.”

North American light-vehicle production in the first quarter of 2013 is up just 1 percent compared with the same period in 2012. Year-over-year production in the United States leads the region, with a 3 percent increase on strong gains from Ford, Nissan and Volkswagen. Production volume in Mexico is up 2 percent, while Canadian vehicle production in the first quarter is down by 9 percent, as all manufacturers, with the exception of Ford, had lower production volume in the first quarter of 2013 than in the same period of 2012.

Vehicle inventory levels in early April fall back to a 60-day supply, compared with 64 days in March 2013. Overall, there are nearly 3.2 million units currently in inventory, as the market heads into the peak spring/summer selling months. Car inventory began the month with a 56-day supply (previously 61 days) and trucks with a 64-day supply (previously 68 days).

LMC Automotive's forecast for North American production is unchanged at 15.9 million units for 2013, an increase of 3 percent from 2012.

More F&I

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

What Market Timing Mistakes Mean for Your Reinsurance Program

When volatility hits, dealer-owned reinsurance programs face a familiar temptation: pull back and wait for calmer waters. New data from BOK Financial shows why that instinct can quietly cost you years of surplus growth.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →