Integrating Dealertrack into Cox Automotive wasn’t Mark O’Neil’s only focus when he was named COO in March 2016. He was also charged with bringing together the company’s four business verticals — Retail Solutions, Inventory Solutions, Media Solution and Financial Solutions — to create what he called ‘One Cox Automotive.’

15 min to read

The topic stirs emotions in showrooms and F&I offices everywhere. Some have labeled it the battle between modernists and traditionalists, with the latter determined to maintain control of how cars are sold and financed. But to Mark O’Neil, nothing can stop the onset of automotive retail’s Digital Age.

His opinion stands out. He’s not some Silicon Valley technogeek. In fact, he began his career in the business in the late ’80s, serving as president of Pennsylvania-based Ertley MotorWorld. He also cofounded and led the development and rollout of CarMax Inc. There was also that year-long stint early last decade when he served as president and COO of online auto sales site Greenlight.com.

Ad Loading...

But most people know O’Neil for his decade-long role as CEO of Dealertrack, a position he held until Cox Automotive purchased the tech firm in October 2015. And since he was named executive vice president and COO of Cox Automotive in March 2016, he has become the company’s digital evangelist.

O’Neil spoke by phone with F&I and Showroom just after delivering his address, “Connected Retail: Deals in the Digital Age,” at the 2017 Automotive Forum. It was a conversation in which the executive shared his vision of the future of automotive retailing and offered a glimpse at the sales and F&I tools Cox Automotive is developing to pave the way to that reality.

F&I: It seems you’ve become the digital evangelist for the company. Why don’t we start there: What’s different about your new role at Cox Automotive?

O’Neil: So, yes, my role has changed. When Cox acquired Dealertrack or shortly thereafter, they created the COO role. The purpose of that role was really to focus on not only integrating Dealertrack but creating a more unified Cox. I’ll call it the “One Cox Automotive,” which entails the four verticals of the business, the software business, which was most impacted by the addition of Dealertrack. That is where vAuto, VinSolutions and Xtime sat.

So, step one was integrating within the Retail Solutions Group. That’s what we call our software group. Second was figuring out how to create a competitive advantage by integrating the four verticals: Retail Solutions, Inventory Solutions, which is anchored by the Manheim Auctions, Media Solutions, which is anchored by Autotrader, Kelley Blue Book, and Dealer.com, and the Financial Solutions, which is anchored by NextGear.

Ad Loading...

F&I: Give me an example of how all that’s going to work together.

O’Neil: Take vAuto plus Stockwave. vAuto makes recommendations to dealers on what vehicles they need, while Stockwave tells you where you can find those cars. For this example, let’s assume your Stockwave software is linked to the Manheim Auction. And let’s say it points you to Manheim New Jersey, where that three-year-old Jeep Grand Cherokee Limited with less than 20,000 miles you’re looking for is sitting at that auction. Boom, you can click to put in a buy now or a proxy bid.

Let’s assume you’re the winning buyer. With one click, we can then link you to our transportation company to have that vehicle shipped. With one more click, we can put it on our floorplan source, which is NextGear. With one more click, we can push the condition reports and the photos to your Dealer.com website. One more click and you can put this right into your DMS, all the cost data and everything that we need to stock it in. Boom, you’re done.

So not only was that only a few clicks to do an enormous amount of linkages, you’re doing marketing, you’re doing accounting work, you’re doing transportation. That’s because we own all these assets. We create the technology backbone that ties everything together.

O’Neil said the next step in Cox Automotive’s digital retailing process is ‘click to execute the legally binding documents,’ a feature he said will go into pilot with ‘some of our lenders’ in the fourth quarter. The tool will then be slowly rolled out next year and the following years as more lenders and state DMVs come onboard.

F&I: So this digital evolution isn’t just taking place on the consumer side. It’s happening on the dealer side as well. Which is further along?

Ad Loading...

O’Neil: Well, the consumer piece is often talked about as the most complex transaction in the consumer’s life — and it is. But if you think of the dealer piece, you’ve gotta source the car, you’ve gotta recon the car, you’ve gotta move the car, you’ve gotta merchandise the car both physically on your lot and digitally, and you still have to execute the sale. So I would say the dealer side is probably more complex, and probably more work is going into that.

But let’s talk about digital retailing for a second, because, again, it’s an example of two groups working together — the Retail Solutions Group and the Media Group, where Kelley Blue Book sits. So think of the five pieces of digital retailing: Step One is giving the customer a real payment, whether it’s a bank offer, a particular lease program or a retail program.

Step Two is getting preapproved for financing. All the paperwork is complete, subject to executing the buyer’s order and the retail installment contract. Those two pieces kind of existed with Dealertrack. Then you do the menu presentation. That’s only just rolled out substantially in Q2 here. It existed, but it really is kind of standalone software. It’ll be a little bit more integrated into the digital retailing suite in Q2.

The third step, which requires our media team, is we want to be able to make a guaranteed offer to a consumer on a trade. Now a trade can either be bringing over negative equity being rolled into the deal, or you’re bringing positive equity. What you want is down payment money. Either way, it’s a critical component of putting the deal together.

So, through Kelley Blue Book, we now have a product called Kelley Blue Book Instant Cash Offer.

Ad Loading...

"So instead of thinking of it as pure digital, it’s kind of an interesting twist. I didn’t say this at the forum, but it’s probably a more accurate statement: Think about it as connected retail. You’re leveraging the optimal components that are done digitally." — Mark O'Neil

F&I: You just rolled out a TV ad campaign touting that, correct?

O’Neil: We did, and that product basically allows consumers to describe their cars on the Kelley site, or dealers can host this widget on their sites. You describe the car and we’ll make you a guaranteed offer on that car, whether the dealer buys it or not. If the dealer doesn’t buy it, then, when the consumer trades the car, we’ll take it and we’ll run it right through one of our auctions. So now we’ve enabled the deal to do that transaction.

F&I: What’s the last step?

O’Neil: So the next step is, obviously, click to execute the legally binding documents. And we’ll go into pilot in the fourth quarter with some of our first lenders, and then that will slowly roll out next year and the following years, adding more and more lenders and more and more DMVs.

Ad Loading...

But our view is that most consumers are really comfortable coming into the dealership, and, in fact, might even have a preference to do that to check the car before they sign that last document. And so the need to do that immediately, we see, is less critical, as long as you can still serve up all the documents when they walk in and it’s a very quick delivery and signing process. So we think there will still be a lot of wet-ink signatures for years to come, but the majority of the process will have been executed digitally.

F&I: During your address at the J.D. Power Automotive Forum in April, you said we should see a 100% digital deal by next year. But you still see the physical dealership playing a role in completing that deal?

O’Neil: Obviously, not all lenders that you need are hooked up to a network to be able to execute digitally, nor most of the DMVs. So I think that’s one side of the equation that’s not yet robustly executed. But the second part is a lot of consumers would say, “Do all the setups,” whether that’s just pairing your phone, understanding the infotainment system or understanding more about maintenance of the car. Whatever it is, most consumers want to engage with the dealer at that level, and they actually enjoy that engagement.

So instead of thinking of it as pure digital, it’s kind of an interesting twist. I didn’t say this at the forum, but it’s probably a more accurate statement: Think about it as connected retail. You’re leveraging the optimal components that are done digitally. I mean, filling out a credit app, whether you want to get up at seven in the morning, do it at 11 at night, or do it on your lunch break, being able to do it at your convenience makes a lot sense. And you ought to be able to do that electronically. In fact, a lot of stores will hand you an iPad and you’ll fill it out yourself, or they maybe allow you to do it on a desktop kiosk. So there’s really no reason to do some of these types of activities in the store.

It’s almost like what Best Buy and Home Depot are doing, where you do all the ordering and comparing and paying for the product online, but you actually go to the store to physically pick it up because you want it sooner or it doesn’t lend itself to shipping. When it comes to auto retailing, I think that’s probably the right way to think of it.

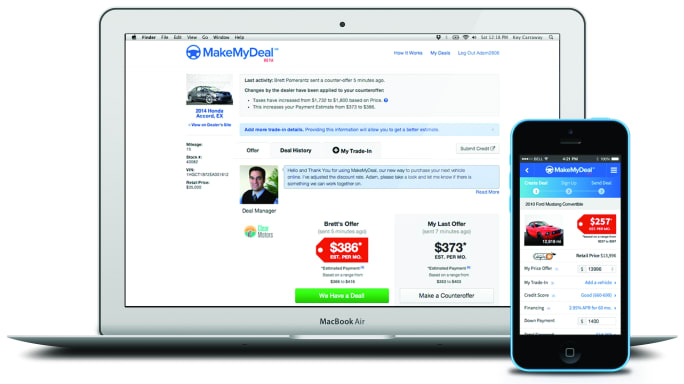

O’Neil said MakeMyDeal was integrated into Dealertrack’s network earlier this year. He revealed, however, that Cox Automotive is preparing to unveil its next version of digital retailing, which will connect the payment, the F&I experience, menu experience, and link trade-ins to Kelley Blue Book Instant Cash Offer.

F&I: You’ve talked a lot about digital retailing, but not once have your mentioned MakeMyDeal. What’s going on with that?

Ad Loading...

O’Neil: So earlier this year we integrated MakeMyDeal into Dealertrack’s network for accurate finance and incentive offers, leasing programs, and credit applications. That integration foreshadows what we are working on for our next version of digital retailing: connecting the payment, the F&I experience, menu experience, and linking the trade-in to Kelley Blue Book Instant Cash Offer. And let me link that with this talk out there that dealers aren’t comfortable with this digital retailing push.

I would say dealerships that still heavily negotiate a deal and that are less transparent are going to have more challenges with digital retailing. No question. And I think a traditional salesperson who only operates on being paid on the gross is gonna be frightened of giving up control in this digitally connected retailing experience.

One of the first things the dealership community needs to get comfortable with is how quickly and seamlessly can I deliver an experience where we get to a firm price. Because the more elongated it is, the higher fallout rate you will have in the digital retailing process.

F&I: So will we see a new MakeMyDeal?

O’Neil: Good question. So the branding of the full seamless integrated suite, we haven’t yet landed on what that will be. I call it “connected retail.” The dealer name and consumer name probably need to change, as we need the dealer’s endorsement of the concept. We also need it to be a comfortable concept for the customer so they feel like they’re in control.

Ad Loading...

And I will tell you it probably will not be something like click-to-buy, because the consumer gets nervous about going from looking at a car to just clicking a button to buy. That’s a huge leap. So stayed tuned, as we’re probably 60 days away or so from probably locking that down.

F&I: MakeMyDeal rolled out the F&I Connect tool back in November 2015. From what you’ve learned, can F&I products be sold online? Because that’s a big leap for F&I offices.

"We found a number of things from that study. One, we found that, on average, people bought more than they were sold. And why do we think that happened? Because we think the consumer, when sitting across from the F&I manager, is thinking, “What is he trying to sell me?” — Mark O'Neil

O’Neil: I’d like to share with you one perspective, one that will exist in our menu shortly. Before I do, I want to share with you two data points. So we have done research with customers on the F&I process. We have asked them, “Would you be willing to spend time to learn more about finance products online? And would you be more likely to buy if you were going through a self-directed process versus a dealership process?”

Sixty-three percent of customers have a preference to learn on their own time and at their own pace about F&I products, meaning you’ve got to deliver that online. Let them watch videos, and read reviews and content. And they’re 58% more likely to buy if they can learn about it on a dealer’s website, versus 51% saying they’re likely to buy if I’m learning from my finance manager.

Ad Loading...

So, again, I think it’s this behavior of consumers getting more used to engaging online. And what I would suggest is happening is this: We have run a number of tests where we gave a consumer an iPad. So this was an in-store experience, where we let them walk themselves through the menu presentation process. They answered five questions, which the dealer could configure. Based on how they answer those questions, we serve up video content, generally no more than a minute-and-a-half video — some of them as short as 40 seconds — on the advantages of buying a service contract, or a prepaid maintenance program, or a key insurance program, etc.

We found a number of things from that study. One, we found that, on average, people bought more than they were sold. And why do we think that happened? Because we think the consumer, when sitting across from the F&I manager, is thinking, “What is he trying to sell me?” So you’re not listening 100%. You’re half-thinking about how you want to respond and what the hidden message is. The other half is actually thinking about the product, versus when you’re watching a video and self-serving — 100% of your attention is listening to the value add of that product.

So we found that consumers spent more than when they were sold. From an F&I manager perspective, the consumer is doing half the work on their own. That means I can handle more customers coming through the F&I office. The other thing we found when customers can engage in digital retailing is inventory turns faster — on average, about five days. So we find a much better experience. And I think it’s the scariest part for the dealer, but it’s the part, in some ways, we have the most confidence in.

O’Neil said the next version of the Dealertrack eMenu will include a feature that operates similar to the ‘Customers Who Bought This Item Also Bought” section of Amazon’s checkout screen. The executive said it will use data designed to reassure F&I product buyers that they’re making the right decision.

F&I: You mentioned a menu feature you’ll be adding shortly.

O’Neil: So, yes, we don’t have it yet, but we hope to have it by the end of the year. We have the data to drive it, but we’ve got to put it all together. It’s very similar to what Amazon does with checkout. Let’s assume you bought a Kindle. You’re going through checkout and they say, “People who bought this Kindle also bought a cover for the Kindle.” Sometimes they give you data on that, sometimes they just tell you that other people bought it. Our view is to take that same general concept and allow a consumer to go through a menu presentation online: Answer five questions, serve them relevant content, and then marry the content to the vehicle they want to buy. And give them comfort and reassurance with data that they’re making a good decision.

Ad Loading...

So let’s assume you’re looking at that three-year-old Jeep Grand Cherokee Limited with 27,000 miles. You have 8,000 miles left of warranty period. We might say, “Look, 62% of customers who bought this car or had only this much warranty period left also bought a service contract.” That would be very familiar, very comfortable for a consumer. And we think there’s a high probability that this will boost the engagement rates and the purchase rates even higher than a dealership selling could, because it’s putting the consumer through a process that they already identify with, are used to, and trust.

F&I: How soon will we see that?

O’Neil: I’m hopeful, as we get into 2018, that we’ll have that incorporated in the next version of the menu.

F&I: Mark, it all sounds great. However, this scenario you just drew up won’t make many F&I pros excited about the future of their profession.

O’Neil: Here’s what I’d say: I think we’re going see a shift in the type of person that’s employed in the dealership. So think back to where I said I think most consumers would still like to actually do Step Five — customers coming in for the setup and delivery after executing some of the documents electronically. So, while I didn’t have a salesperson during the process — maybe I might — that salesperson might be more of someone at the end of the chat, right? It’s a different person, but you will need someone to chat with the customer.

Ad Loading...

"So I think the dealer has to get comfortable, just like every other retailer has when it comes to multichannel retailing — where you’ve gotta be able to start and stop in different ways, because if that’s what the consumer wants, the consumer always wins." — Mark O'Neil

I think part of the sales job will be converted to delivery specialists, who will be a little bit more like the individual in the Apple Store behind the Genius Bar. They’re going to help you pair your phone. They’re going to go through all the setups. Maybe it’s a college kid who’s very tech-savvy. So it may not be the old-school salesperson. But I think there will be people involved in this process. I don’t think it’s going to be a no-touch, no-human-interaction process. You’re still getting a tour of the service and parts area in the dealership and setting up the first service appointment.

And I do think total labor costs for a dealership are going to come down, or labor cost per unit or per car sold is going to come down. It’s no different than in the banking industry. With the introduction of the ATM, you had a lot of self-servicing. You leverage your technology to do the easy exercises, because getting cash or making a deposit doesn’t need a person. Getting a mortgage or opening a checking account does. So the higher value activities will still be engaged with people. That’s good for the dealer, because it saves them labor, and they need to save labor to protect their margins.

F&I: Sounds like dealers will have to operate under two business models until all that happens.

O’Neil: Well, let’s pick any mainstream retailer. I’ll pick Home Depot, because I think they’ve done a good job. Home Depot hasn’t abandoned the physical store whatsoever. But Home Depot has figured out how to create, let’s call it, omnichannel retailing, where they can handle the consumer doing part of the transaction online and in the store. So they’re as equally adept at handling that online part as they are the traditional way. The third way would be 100% digital, where the product is shipped to the house.

Ad Loading...

So I think the dealer has to get comfortable, just like every other retailer has when it comes to multichannel retailing — where you’ve gotta be able to start and stop in different ways, because if that’s what the consumer wants, the consumer always wins.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

It may be human nature to back off when a customer seems to say no to a product or service. But experts say F&I managers should operate as though the answer will be the opposite.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.